All 16 entries tagged Keynes

View all 18 entries tagged Keynes on Warwick Blogs | View entries tagged Keynes at Technorati | There are no images tagged Keynes on this blog

November 15, 2013

Which Dead Economist Must I Follow?

Writing about web page http://politicsatwarwick.net/2013/11/13/economics-and-the-crisis-which-dead-economist-must-i-follow/

I contributed recently to the Politics at Warwick blog, which I thank for its hospitality. My post elicited a comment to which I'd like to respond; my response is longer than my original post so I decided to include it here. First I'll put up my original post, dated 13 November 2013. Then I'll quote the comment and respond to it.

How should the economics curriculum respond to the global financial crisis and ensuing recession? Community activists and students have become vocal in this discussion, as recently described by journalist Aditya Chakrabortty and Matthew Watson.

Events have prompted questions about economists’ understanding of financial markets; the same events have generated a deluge of new data. How should economists respond? Economic research has already responded; hundreds of new articles have analysed global imbalances, market efficiency, corporate behaviour, regulation and deregulation, policy rules, the politics and economics of past crises, and the relative fragility of economic and political institutions in history.

The core curriculum has been slower to change. Here are two reasons. The first is that we no longer teach from handwritten notes and a chalkboard; students and teachers demand comprehensive textbooks with instructor manuals, PowerPoint slides, and websites. These take years to develop (and revise). Although slow, change is already visible. Because change is slow, there is more to be done. Change will probably accelerate through initiatives like the CORE (Curriculum Open-access Resources in Economics) project.

A better reason for inertia in the curriculum is our foreknowledge that the full meaning of recent events will take decades to establish – although many people believe that they are already obvious. To illustrate, today we continue to make new findings about the last Great Depression, which began in 1929, although many who lived through the 1930s were so certain of the answers that they were willing to kill and die on that basis.

How should the core curriculum change? A common complaint is that economics is dominated by a single school of “neoliberalism” or “market fundamentalism.” There are calls for more diversity in economics; some students want more access, specifically, to Keynes and Marx.

It is simply untrue that mainstream textbooks reflect principles of market fundamentalism. I can’t think of a principles text that doesn’t follow the initial explanation of market equilibrium with an immediate, detailed discussion of the varied sources of market failure and the regulatory interventions that might follow.

While one may learn from both Keynes and Marx, what is to be gained from taking them outside their historical settings? A Keynesian model focuses on flows (of income and employment) while neglecting stocks (of capital and debt). Yet capital and debt are very important! Keynesian principles are linked to a model of household behaviour (the “marginal propensity to consume”) that half a century of applied research has comprehensively invalidated. A Marxian model simplifies the continuum of capital ownership into a two-class society; additionally it throws out efficiency and substitution, so distribution is all that remains. In the context of today’s mainstream, each of these is now a stagnant, oxygen-starved backwater.

The importance of competing traditions is much overrated. Those that wish to organize the curriculum around them seem to believe that the major decision each economist must make is “Which dead economist must I follow?” and after that her research findings and policy recommendations will follow. This may be a natural reaction to the fact that mainstream economists are often unenthusiastic about policies that gather widespread popular support, for example rigid immigration controls, employment protection, and double taxation of corporate income. It might be easier for the supporters to say “Oh, those economists are all neoliberals who are ignorant of Keynes and Marx” than work patiently back through the evidence that fails to confirm their biases.

“Economics ought to be a magpie discipline,” writes Chakrabortty. But Economics is a magpie discipline. Most non-specialists – and most journalists – think public and private finance are all we do. They are amazed when I describe the sheer diversity of research that is done just in my department (here and here). We suck up topics and data from any time and place; we don’t care what discipline claims to own them. Then they backtrack and say, “Of course, I didn’t mean to criticize you (or Warwick), I meant Friedman (or Chicago).” The fact is there are no clear intellectual boundaries among schools of thought; we should all mingle in the same fluid mainstream, which is broader, deeper, and faster than you think.

Concluding, Chakrabortty reports a lament for the good old days. Tony Lawson recalls the Cambridge economics faculty in the time of Nicky Kaldor and Joan Robinson: “There were big debates and students would study politics, the history of economic thought.” I remember; I was there too, as a student. The big debates were an exercise in identity politics, not economics. Hostile clashes between intolerant armed camps ended in a war of attrition that benefited no one, least of all students. There is a warning here: be careful what you wish for.

On the day that my post appeared, the anonymous blogger Unlearning Economics posted a comment which you can read in full here after scrolling to the bottom. Here's my response, with excerpts from the comment inset.

Unlearning Economics quotes me and comments:

“A Keynesian model focuses on flows (of income and employment) while neglecting stocks (of capital and debt).” First, Keynes didn’t ignore capital or debt at all; that is simply false ... Keynes carried over some silly marginalist concepts like the efficiency of capital (clearly he mentioned capital once or twice).

My response: It is useful to distinguish between “things Keynes wrote about at various times” and “things that are core principles of the Keynesian model.” Of course we could argue about the division, but it seems to me capital and debt belong to the former, not the latter. The point is exemplified by Keynes’s model of consumer behaviour (more below), in which capital and debt play no role, although they were fundamental to other models available at the time. As for the marginal efficiency of capital, Keynes introduced this to rationalize his discussion of investment (a flow), not to understand the behaviour of the capital stock.

Again, Unlearning Economics quotes me and comments:

“Keynesian principles are linked to a model of household behaviour (the “marginal propensity to consume”) that half a century of applied research has comprehensively invalidated.” Which research would this be? “People don’t consume all of their income” is hardly a false statement.

My response: Yes, it's true that “people don’t consume all their income,” but that isn’t the issue. The issue is whether the main thing in consumption is a stable proportion between household consumption and current income at the margin, as Keynes believed. I should add that he not only advanced this idea in theory but also applied it in practice, for example in his writing about how to pay for World War II. Franco Modigliani, Milton Friedman, and others investigated this idea after the war and failed to find it in the data. They did identify a stable relationship between consumption and wealth, or lifetime (or "permanent") income, to which changes in current income make a small or negligible contribution. Because permanent income is uncertain, the future (including expectations of inflation and the real interest rate) are fundamental. Modern new-Keynesian models drop the marginal propensity to consume (and the multiplier) and focus exclusively on intertemporal substitution intended to smooth consumption over time. Which takes me on to our next point.

Unlearning Economics adds:

Second modern post-Keynesian is *all about* stock-flow consistent models ... people like Godley, Keen etc have updated [Keynes’s] work.

My response: Yes, certainly. Here another distinction arises, between Keynes and the post-Keynesians (or Marx and the post-Marxists). Naturally, there is development in the Marxian and Keynesian traditions. I could not dispute that, when a great economist produces an insight that turns out partial or incomplete or defective in some respect, it may be fixable. There is evolution. Evolution has produced neo-Keynesians and post-Keynesians (and Marxists). Evolution is better than stagnation. At some point it generates new species. Every year I help teach a “new-Keynesian” model of the macroeconomy to Warwick undergraduates, and every year I (and I hope they) learn something new. Yet the label “new-Keynesian,” like George Box’s economic models (more below), although useful, is also wrong. Would Keynes recognize it as his? It’s debatable. Does it matter? Only if you want to claim ownership over Keynes’s legacy.

Unlearning Economics quotes me and comments:

“A Marxian model simplifies the continuum of capital ownership into a two-class society; additionally it throws out efficiency and substitution, so distribution is all that remains.” Marx spent a lot of time talking about the difference between financial capital and industrial capital; Lenin updated his work in the context of ‘globalisation’ (imperialism). I also have no idea how you got that Marx “throws out efficiency and substitution”: he continually praised the efficiency of capitalism, and substituting capital for labour is the main driving force behind the tendency of the rate of profit to fall.

My response: I considered proposing that “efficiency of capitalism” belongs to “things Marx wrote about at various times” rather than “things that are core principles of the Marxian model.” On reflection, however, I am not convinced that Marx had a concept of efficiency at all, not in the sense that economists use it today (when you can’t reallocate resources without using more of some input or consuming less of some output). Marx did write a lot about the productiveness of capitalism, but I do not think he was thinking about total factor productivity.

Similarly, I do not think Marx had a concept of substitution in the sense of a choice between alternatives that varies with their relative price. Yes, it’s possible to rewrite Marx’s idea of the organic composition of capital (the constant/variable capital ratio) as capital/labour substitution, but that is not at all how Marx described it. His idea (Capital III, chapter 13) was that over time the ratio of constant and variable capital in value terms will tend to rise, but that seems to be driven by the accumulation of capital, not by relative factor prices. What is described is a process that piles capital up faster than labour; there is no process that allows substitution between them along a frontier. With labour the only source of surplus value, the rate of profit on capital must tend to fall.

Since Unlearning Economics charges me at the outset with “complete ignorance of Keynes and Marx,” I thought I had better come up with a test of Marx’s understanding of substitution. When I teach the subject of economic warfare I put a lot of emphasis on substitution. People who are not mainstream economists (military commanders, for example) often make biased predictions about the effectiveness of blockades and sanctions, and this is because they lack a concept of substitution. They expect a blockade to curtail production and so to cause the rapid downfall of the blockaded economy. In history, the curtailment of trade has generally brought about relative price changes that stimulate substitution and in turn this will make the blockade less effective than expected. So I looked to see how Marx wrote about blockades.

In 1861 the American Civil War led to a blockade of the Southern ports. The Confederacy responded with a cotton embargo; they thought this would trigger such a crisis in Britain’s textile industry that London would have no choice but to intervene on the Confederacy’s behalf. In the autumn of 1861 Marx wrote (in several places including here, for example) predicting that the stratagem would succeed: “England is to be driven to break through the blockade by force, to declare war on the Union, and thus to throw her sword on the scales in favour of the slave-owning states.”

It did not happen. In Britain the price of raw cotton shot up (which Marx could see), and this stimulated a search for alternative supplies, soon found in Egypt and India (which Marx entirely discounted). He had made the characteristic error of someone who does not get substitution.

Back to George Box, who wrote that “all models are wrong, but some are useful.” The models you can find in Keynes and Marx are no different; they are all wrong in the Boxian sense. Are they useful? Sometimes, yes. Marx’s idea of surplus extraction is useful for understanding societies with closed elites and extractive economies, although not modern capitalism. Keynes’s idea of animal spirits gives insight into modern capitalism as a nice corrective to the idea of rational expectations. But, why should I, or you, or anyone confine themselves to the limits of any “wrong” model by declaring that I am a Keynesian or a Marxist? When scholars do that, it surely tells us more about the politics of identity than about their scholarship.

In fact, I fear that the tone of this discussion may exemplify my final point: when social science is polarized into schools of thought, s/he who is not with me is against me and personal rancour is the likely product.

Mark Harrison

15 Nov 2013 09:11

|

Mark Harrison

15 Nov 2013 09:11

| ![]() Tags: Economics History Keynes Marx

|

Tags: Economics History Keynes Marx

|  Comments (2)

|

Comments (2)

|  Report a problem

Report a problem

Please wait - comments are loading

Please wait - comments are loading

April 26, 2011

The History of Britain's Public Debt Does Not Give Grounds for Complacency

Writing about web page http://www.johannhari.com/2011/03/29/the-biggest-lie-in-british-politics

Twice recently, the journalist Johann Hari has suggested that we are going through a manufactured crisis. The history of Britain's public debt, he argues, show that present levels are modest and there is no need for precipitate action to restrain government spending:

Here’s the lie. We are in a debt crisis. Our national debt is dangerously and historically high. We are being threatened by the international bond markets. The way out is to eradicate our deficit rapidly. Only that will restore “confidence”, and therefore economic growth. Every step of this program is false, and endangers you.

Let’s start with a fact that should be on billboards across the land. As a proportion of GDP, Britain’s national debt has been higher than it is now for 200 of the past 250 years.

The quote is from Johann Hari's blog, The biggest lie in British politics(March 29, 2011). Before that, in When will David Cameron's soufflé of spin collapse?(February 11, 2011) Hari wrote:

Beneath Cameron's entire agenda runs the biggest lie of all: that Britain is facing an "unprecedented" level of debt. In reality, Britain's national debt has been higher as a proportion of GDP for 200 of the past 250 years.

The full argument, widely blogged and tweeted, goes like this:

- Current debt levels are historically modest.

- So, there is no need for drastic action to contain the debt through deficit reduction.

- In fact, advocates of public spending reductions are creating a phoney sense of emergency in order to vandalize the welfare state for other reasons.

On a closer look, this line of reasoning raises interesting issues. Here is a chart that shows the evolution of Britain's public debt as a percent of national income since 1692:

(The figures from 1692 to 2010, and a forecast for 2011, compiled by Christopher Chantrill, can be found at http://www.ukpublicspending.co.uk/. I added the Office of Budget Responsibility forecasts for 2012 to 2014.)

First, is it true that Britain’s current debt level is historically modest? Yes, clearly -- although Hari exaggerates. As of 2011, Britain's debt ratio has been higher than it is now for just 169 (not 200) of the last 250 years (or you could say "200 of the last 282 years").

Next, is there anything else of interest in these figures? Well, since the level of debt today is the sum of past changes, we could also look at the rate of change of Britain’s public debt. Interestingly, there have been just 36 years in the last 320 when the debt grew faster as a percent of GDP than in 2009 to 2011. Let me give some twentieth century examples, and you'll get the idea. One run of years when the public debt climbed faster was 1915 to 1919. Another was 1941 to 1946.

In other words, Britain's debt has been growing in the last couple of years at rates generally exceeded only in major wars. It's particularly dangerous because, as I explained here, debt has persistence. Once the conditions have been created for it to grow rapidly, it'll go on rising under its own momentum until you take steps to control it. The longer you leave it, the harder it gets.

In some general sense, however, Hari has a point. It's true that Britain’s debt has been higher than it is now for more than two of the last three centuries. He overstates the case, which I dislike, but I accept that most policy advocates do that most of the time, and they can't all be wrong at once.

Now, some economic history. My point here is that there are important reasons why Britain today cannot handle the 200% plus debt ratios that characterized the 1820s (after the Wars of the Austrian and Spanish Successions, the Seven Years' War, and the Napoleonic Wars) and the 1950s (after World Wars I and II). If much higher debt levels were okay then, why not now? The answer begins with: because times have changed. We no longer live in the 1820s or the 1950s. It’s the twenty-first century.

How did Britain sustain that kind of debt in the past? Well, how do you handle a debt that is twice your income? The important thing is that you have to be able somehow to limit the interest payments. If debt is twice national income, as long as you can borrow at no more than 3%, you have to transfer only 6% of national income each year to bond holders. But, if the interest rate goes up to 12.5% (as it is today for Greece and Ireland) then the transfer eventually goes up to an infeasible 25% of national income. Basically, you’re insolvent.

How do you keep the interest rate down to 3%? In one of two ways. Either you dominate the world capital market – as Britain did in the eighteenth and nineteenth centuries. Or, you close the domestic capital market off from the world, so you can dominate your own little pool of saving – as Britain did in the mid-twentieth century. Either way, you can borrow if there's no one else for people to lend to.

In the eighteenth and nineteenth centuries, Britain could handle a much higher debt ratio than today’s because an integrated global capital market developed in which the British economy was the major borrower and lender. There was little credible competition with British bonds. As a result, British public debt remained universally acceptable despite its relative abundance. (The United States has enjoyed a similar position since World War II, but the uncontrolled U.S. budget deficit may eventually put an end to that.)

Before the twentieth century, moreover, the British government did not have major commitments to social spending at home. The spending of the central government was principally on administration and defence. As a use of government revenue, interest payments did not have to compete with major entitlement claims. This kept government guarantees of repayment credible.

The two world wars broke up the global capital market. Although no longer the world's financier, in the mid-twentieth century Britain could continue to handle a much higher debt ratio than today’s for a reason that was completely different from before. In a closed domestic capital market, British bonds were protected from competition. British lenders could not freely buy the bonds of other countries, even if they wanted to, because of government controls on foreign exchange and capital movements. With alternatives kept out of the market, British public debt continued to be acceptable at home.

Today, these conditions have gone. There is a global capital market again. British bonds have no specific advantage for foreign lenders (as they had in the eighteenth and nineteenth centuries), and domestic lenders can pick and choose among bonds issued by many countries (something they could not do in the middle of the twentieth century).

This is why a level of debt that was sustainable decades or centuries ago is not sustainable today. Today, no one has to lend to the British government for lack of alternatives. In short, whether or not it is true, it is irrelevant that "Britain’s national debt has been higher than it is now for 200 of the past 250 years." The conditions of those 200 years have gone.

Here is the first reason why it is important for the British government to control the level of public debt: the day of reckoning would be upon us if we didn't. A combination of rising debt, declining confidence, and rising interest rates would then force us to close the budget deficit even faster than planned at present. The world doesn't owe us a living; we already owe them. In fact, don't feel sorry for us; feel sorry for Americans that the U.S. Treasury has enough discretion to put off its day of reckoning until the fiscal mess there will be still more dire than it is now.

The world has changed; for Britain, has it changed for better or worse? Some people might think "for worse." There are those that don't like globalization on principle; others might wonder, more pragmatically, whether the conditions of the capital market half a century ago could be restored. Talk of capital controls is in the air again. If capital account liberalization made it more difficult for us to carry on with deficit spending and a rising public debt, then why not restore the protected capital market regime of the 1950s?

The case might be that, by restricting the choices of British lenders again, we could increase the domestic demand for British debt. (By the same token, however, we would also eliminate the foreign demand.) On closer inspection, this course of action hardly recommends itself. When lenders lose the will to lend, as with Greece, Ireland, and Portugal, it is usually for good reason. Taking away their option to buy elsewhere would amount to sticking fingers in our ears so as not to hear bad news.

Besides, if we restored the conditions that enabled the government to borrow more than twice GDP, what reason is there to suppose that the government would make better use of the money than private borrowers? Still one of the richest countries in the world, Britain’s prosperity has come from private enterprise and innovation, industrial and commercial revolution, and trade and finance; it did not come from Whitehall.

To finish up, the second reason for fixing Britain's debt while it is still at today's historically "modest" level is that having a debt twice your income is a sign that something went terribly wrong; a run of major wars, for example. Faced with the worst recession in 80 years, the British government was right to let its budget go into deficit temporarily. At that moment an increase in Britain's debt was inevitable. Now it's right to bring it back under control over a few years.

So, if the British government today cannot dominate its capital market and continue to eat up national resources beyond the willingness of the population to pay taxes -- there is reason to be glad.

Mark Harrison

26 Apr 2011 18:18

| ![]() Tags: Economics Keynes Recession Using-Data

| Comments (0)

| Report a problem

Tags: Economics Keynes Recession Using-Data

| Comments (0)

| Report a problem

April 24, 2011

Surely You're Joking, Mr Keynes?

Writing about web page http://www.debtonation.org/wp-content/uploads/2010/06/Fiscal-Consolidation1.pdf

The British government is seeking to bring the public debt under control by cutting back public spending. A popular story is going around, however, that suggests this is either crazy or a thinly disguised plot to undermine the public sector; see for example Johann Hari's blog, The biggest lie in British politics, March 29, 2011.

How does this story work? It runs like this. Start from the government’s plan for cutting public spending:

- With lower spending, the national income will fall.

- With lower national income, tax revenues will fall.

- With lower tax revenues, public borrowing will remain high.

- With public borrowing still high, the public debt will be hard to shrink.

- The burden of the debt relative to GDP could even rise.

In this story, the public debt is hard to control because it pushes back when the government tries to cut spending. It pushes back so hard that cutting public spending is actually counter-productive. In fact, the story implies that the government should spend its way out of debt! This is because more public spending would generate higher national income, higher tax revenues, less borrowing, and less debt relative to GDP.

How good is this story? It has a logic, purely Keynesian in spirit. But is it true? One issue could be that it leaves such factors as business confidence and the exchange rate out of the calculation. Ultimately, however, it’s an empirical question. That is, it can be answered by looking at how the public debt has actually responded to changes in public spending in the historical record.

It’s clear how both the UK Treasury and the independent Office of Budget Responsibility answer this question. They predict that, with the current fiscal squeeze, Britain’s public debt will rise more slowly, peak in 2014 at around 70 percent of GDP, and then start to fall. In other words, deficit reduction will eventually win. Given enough time, cutting public spending will not be counterproductive.

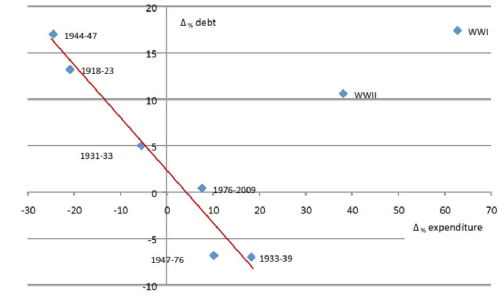

The Economic Consequences of Mr Osborne is a paper that Victoria Chick (of UCL) and Ann Pettifor (of the New Economics Foundation) circulated in June last year. It tells a more pessimistic story. It uses a century of data to suggest that the public debt varies negatively, not positively, with public spending. Fiscal cutbacks, they conclude, have consistently increased, not reduced, the burden of public debt. The key result is illustrated by their figure, below. The figure compares the change in the burden of the debt relative to GDP (the vertical axis) with the percent change in nominal public spending on goods and services (the horizontal axis), measured in annual averages over varying periods of time. The idea, I guess, is that nominal spending is the one thing over which the government has direct control; how does it affect the burden of the debt?

This chart suggests that a change in the public debt is negatively associated with a change in nominal public spending. When public spending falls, debt rises. Chick and Pettifor also report this result as a regression (the Δ symbol means “change in”):

Δ public debt/GDP = 2.2 – 0.6 x Δ public spending

Notes:

- The 2.2 means that the public debt would have risen on average by 2.2 percent of GDP per year in every episode if public spending remained unchanged.

- The 0.6 means that, in addition, debt tended to rise by 0.6 percent of GDP for each one percent cut in nominal public spending.

- Chick and Pettifor state that this relationship explains 98 percent of the total peacetime variation in the debt.

There are two implications. One is that deficit reduction is pointless because it will worsen the burden of the debt. The other is that the government can and should spend, not save its way out of debt.

This finding has been widely blogged and tweeted. It even made its way into a quarterly newsletter of the Royal Economic Society. But I have not seen any serious commentary so far. So, let me try. To begin, there are four odd things about the picture in the chart.

- The compression of 100 years of annual data into eight data points.

- The exclusion of the two data points that don’t fit (the two World Wars).

- The six data points that are used to fit the line are very different in coverage, ranging from two years (1931 to 1933) to 32 years (1976 to 2009).

- Regardless of the length of the period covered by each data point, the effect of public spending on debt is assumed to be exactly contemporaneous.

Is this a sufficient basis for a very important policy prescription? In my view, absolutely not.

Let’s look again at the data, which Chick and Pettifor helpfully provide in an appendix. Like them, I'll use nominal public spending changes to try to predict changes in the public debt burden. Unlike them, I’ll use all the data. I won't leave out any inconvenient observations. I’ll work on the basis that, if the relationship we are looking for exists, it ought to be simple and direct; it should not be instantaneous, but it should be speedy; and it should be there, year on year, in every period, regardless of other circumstances.

One other thing I'll do differently: Remember the 2.2 percentage points a year of upward drift in the debt burden that Chick and Pettifor found. Remember also the official forecasts that expect the Osborne budget cuts at first only to slow the growth of the public debt; not until 2014 will the debt start to fall relative to GDP. This reflects an important problem that Chick and Pettifor left out of account: the burden of debt has a momentum of its own.

What does this mean? Suppose there is a lot of public borrowing, causing the debt to rise rapidly. If the government reduces its deficit but does not eliminate it, the public debt will go on rising, but more slowly. It will not fall until the deficit is closed altogether. Moreover, while it is rising, the additional interest payments will be added to the debt, increasing it further. In other words, whether or not there is pushback in the public debt, there is certainly persistence. This is matched by the data, which suggest that public debt has moved systematically up or down over long periods under its own momentum. You can't ignore this if you want to understand how current fiscal policies affect the evolution of the debt.

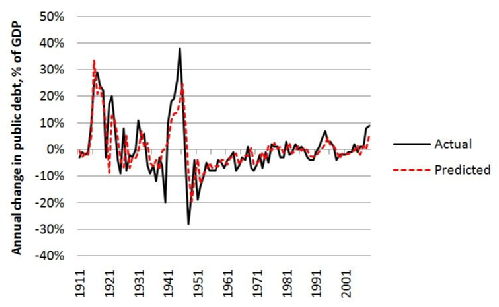

My own calculation uses year-on-year changes in public spending (percent of previous year) and public debt (percent of GDP) from the Chick-Pettifor data. It allows the change in the public debt in a given year to be influenced by not one but two things, both in the previous year: how public spending was changing, and how the debt itself was changing. Including the latter means we can work out the historical persistence factor in the change in the debt from one year to next year. Using Δ to mean “change in” and “(-1) to mean “in the year before,” here are the numbers that come out:

Δ public debt/GDP = -0.01 + 0.74 x Δ public debt/GDP (-1) + 0.14 x Δ public spending (-1)

Notes:

- The 0.74 means there is quite a lot of persistence in the debt: if public spending was unchanging, but the public debt increased by one percent of GDP, it would increase again by 0.74 percent the following year.

- The 0.14 means that the historical relationship between a change in the public debt and the change in public spending one year previously is actually positive. This is the most important result. Allowing for the persistence factor, if the government increased nominal public spending by 1 percent, the public debt tended to rise by 0.14 percent of GDP the following year.

- The explanatory power in this relationship is quite high. For the experts, the t-ratios of the 0.74 and the 0.14 are 11.0 and 5.2 respectively, meaning that the probabilities of finding this pattern by accident are extremely low. Nearly 60 percent of the total historical variation of the change in the public debt is explained. Of course, this is much less than the 98 percent that Chick and Pettifor say their model explains. I set myself a far stiffer test, however, by using 98 (not 6) observations, so that there is much more variation in the data to be explained. I also included all the years that Chick and Pettifor arbitrarily dropped in order to get their result.

The next figure shows how well the regression equation predicts the actual year-on-year changes in the debt ratio over the whole period.

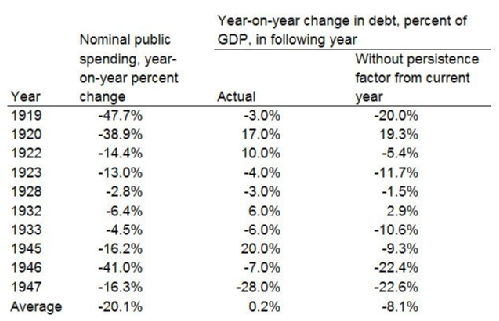

As a final check, I narrowed my focus down to those years in which nominal public spending actually fell. Public spending was unlikely to fall without a deliberate government policy of fiscal consolidation. Never mind what happened on average across the century as a whole; what happened to the public debt when the government took an axe to public spending? There were just ten such years within the sample. This is what happened in them.

The first column shows that in these years nominal public spending was cut on average by 20 percent. The second column shows that in the next year the debt burden did not fall on average, and even rose slightly. Perhaps Chick and Pettifor would see this as validation of their idea. But it ignores the persistence factor in the debt. In most years that public spending was cut, there was already a large deficit that fuelled rapid growth of the debt. Unless the deficit was eliminated immediately, the debt would still grow, but at a slower rate. In the third column, I estimate how the debt would have behaved without the inherited momentum. On that basis, the debt would have fallen in eight of the ten years shown, and it would have fallen on average by 8 percent of GDP.

I'd never claim that this is the best that can be done. I do claim that, if you treat the same data properly, they can tell a very different story from the one that Chick and Pettifor come up with.

To sum up: Deficit reduction works. As for the Chick-Pettifor story, it is not completely wrong. There is a grain of truth in it. Once the public debt is set on a particular course, it is hard to change that course quickly. But it is just persistence that takes time to reverse; it is not a pushback so strong that trying to controll it becomes pointless or counterproductive. Once we allow for the momentum of the debt burden, we can uncover the simple, intuitive, positive relationship between spending and debt that even a non-economist might expect to find.

At the beginning I outlined a Keynesian story that starts with deficit reduction and ends with an increased burden of the debt. It is an intriguing story and it is popular among those that are easily satisfied when a result seems to match their preconceptions. But, like many intriguing stories, it is a fiction. What the figures actually show is that more public spending means more public debt.

Spend our way out of debt? Surely you’re joking, Mr Keynes.

Mark Harrison

24 Apr 2011 23:11

| ![]() Tags: Economics Keynes Recession Using-Data

| Comments (2)

| Report a problem

Tags: Economics Keynes Recession Using-Data

| Comments (2)

| Report a problem

September 08, 2010

Why Bad Economics is Like Bad Art

Writing about web page http://whatpaulgregoryisthinkingabout.blogspot.com/2010/09/do-we-need-new-economics-101.html

It's economics bashing time again.

The latest to have a go is Gideon Rachman in yesterday's Financial Times. "Sweep economists off their throne!" he demands. He compares economists unfavourably to historians, "archive grubbers" who at least have a sense of modesty about their claims to rigour. He goes on to complain about the "brash certainties, peddled by those pseudo-scientists, otherwise known as economists."

As an economic historian -- and I do grub around in archives -- I suppose I have some sympathy for this view. Only a year ago I was writing about the advantages of history in helping us see what's coming round the next corner.

But as a trained economist I think it misses the point.

Good economics isn't brash and doesn't make unjustified claims of predictive power. Specifically, good economics is not the handmaiden of the journalists and politicians who most want economics to support their nostrums and interventions. My Hoover colleague Paul Gregory makes a powerful case that what our first year students have been learning is still pretty much on the button in today's world. It is, above all, an economics that promotes scepticism, critical thinking, and the avoidance of Type I errors.

My point is that there is not just "economics." There is good economics and bad economics. I don't care if it is radical, liberal, conservative, or what. It's interesting that good economics of every school or tradition has more in common with the good economics of other schools than it has with bad economics of any school.

The problem is that there is always a demand for bad economics and there is also a plentiful supply of it. Why? We won't discuss good and bad physics, because that annoys too many people. Instead, think about bad art. On the supply side, untalented artists exceed the number of talented ones by a large margin. So, bad art is abundant. The same is true of economists; there are many more people like me that are writing about economics, for example, than there are Keyneses, Hayeks, and Friedmans. (I hope there's an even larger number of economists that are worse than me, but that's not for me to say.)

On the demand side, many people (myself included) are not really sure of the difference between good and bad art. Also, there are many reasons why we positively desire bad art: because it is comfortable; because it fits with the decor of the room we live in; because it promotes our fantasies without transcending them; and, particularly, because some critic tells us it is good when it's not. I'm sure I personally subscribe to at least some bad art for each and all those reasons.

The demand for bad economics is similar. In fact, just as critics and reviewers mediate the demand for bad art to the public, bad economics has a bunch of people that do the same job of telling the public to buy it. Who are they? Well, many of them are politicians and, er, journalists.

Since this is about economics, we should also think about price. Good economics is relatively scarce, difficult, and uncomfortable; it's designed for truth, not reassurance. In short, the price is high. Bad economics is abundant, soft, and easily absorbed. For all these reasons, it's cheap.

In fact, I'm fairly sure some of the journalists that are now hopping mad at economists are mad just because they themselves previously invested too much of their beliefs in bad, cheap economics. I once had a rather ill-mannered go at Anatole Kaletsky of The Times on this score. Not all of them are to blame, though, and specifically not Gideon Rachman. (I checked out what Rachman was blogging about before the crisis broke in 2007. At least, he wasn't promoting buy-to-let.)

Anyway, let's get back to sweeping the bad economists off their throne. Get rid of them; then what? Who are we going to ask about the economy? Sociologists? Some guy in the pub? Use common sense?

The trouble is, this is a surefire way of replacing bad economics with ... more bad economics. It was Keynes, himself a great economist, who wrote:

Practical men, who believe themselves to be quite exempt from any intellectual influence, are usually the slaves of some defunct economist. Madmen in authority, who hear voices in the air, are distilling their frenzy from some academic scribbler of a few years back.

Mark Harrison

08 Sep 2010 18:14

| ![]() Tags: Economics History Keynes Recession

| Comments (6)

| Report a problem

Tags: Economics History Keynes Recession

| Comments (6)

| Report a problem

July 26, 2010

The Return of Animal Spirits?

A student asked me recently if the economists' consensus is that deficit reduction should be delayed until private demand has picked up -- which might not be any time soon. My first response was to point out that, while this might easily be the impression gained by reading the pages of The Guardian, a number of distinguished economists take the view that global demand would benefit from a more rapid fiscal adjustment. My Hoover colleague John Taylor has listed some of them here.

I also considered how to explain the wide range of disagreement to my student. Model uncertainty is part of the story, reflected in divergent views about the value of the government spending multiplier. According to President Obama's advisers, a government consumption stimulus of 1% of GDP will add 1.55% to U.S. GDP over 16 quarters, i.e. every $1 of federal spending should create another 55 cents of private consumption and investment. A recent IMF paper, in contrast, estimates that the effect goes nearly to zero over the same period, i.e. the same $1 of federal spending eventually reduces private consumption and investment by an equal amount.

Just as importantly, I wondered whether, in addition to differences between models, there is also inconsistency within models -- specifically, within the Keynesian model as some are applying it currently.

Think of Keynesian economics as incorporating two key insights. One is the problem of effective demand, and the spending multiplier that augments the effect of any income shock on aggregate demand. The other is the problem of unpriced uncertainty and the human reaction to this problem, which Keynes called "animal spirits." It seems to me that Keynesians are sometimes unjustifiably selective in applying these two insights.

To simplify, the Keynesian narrative of the crisis should have both main elements. On the way down they work like this. Borrowers and lenders failed to price the uncertainty in asset markets. Animal spirits soared, then collapsed as reality struck home. When animal spirits collapsed, they took down effective demand and there was a sharp multiplier contraction. It's a coherent and interesting diagnosis. Now we have the problem of getting back up. What should the Keynesian narrative of the recovery look like? Here the prescription of leading Keynesians (I'm thinking of Paul Krugman, Brad deLong, and my Warwick colleague Robert Skidelsky) becomes curiously one sided; there's the multiplier -- and just the multiplier. Animal spirits aren't in the picture, so private demand is destined to be flat. In this view, the only thing that can get us back up off the floor is discretionary government spending. That's why, they argue, deficit reduction right now is crazy.

On top of that are the politicians and the journalists. There is a lot of Keynesian-inspired "never again" publicism around at the present time. This might be stretching it a bit, but the spirit of it is pretty much: Animal spirits got us into this mess -- never again! Animal spirits are bad -- let's kill them off, once and for all! We need rules that will put a stop to irrational behaviour! Let's appoint sensible people to take charge and just not let that happen any more!

This is absolutely not the spirit of Keynes. Keynes did not say that animal spirits are a bad thing or that we should get rid of them. He said that animal spirits are a source of instability, and they are hard to manipulate; but they are also the driver of capitalist enteprise and we cannot get away from them or do without them. Here I'm going to quote a few sentences from Keynes's General Theory of 1935 (which is on line here). First, Keynes suggests that enterprise relies on animal spirits as much as business calculation:

Even apart from the instability due to speculation, there is the instability due to the characteristic of human nature that a large proportion of our positive activities depend on spontaneous optimism rather than on a mathematical expectation, whether moral or hedonistic or economic. Most, probably, of our decisions to do something positive, the full consequences of which will be drawn out over many days to come, can only be taken as a result of animal spirits — of a spontaneous urge to action rather than inaction, and not as the outcome of a weighted average of quantitative benefits multiplied by quantitative probabilities. Enterprise only pretends to itself to be mainly actuated by the statements in its own prospectus, however candid and sincere. Only a little more than an expedition to the South Pole, is it based on an exact calculation of benefits to come.

When animal spirits falter, so does enterprise:

Thus if the animal spirits are dimmed and the spontaneous optimism falters, leaving us to depend on nothing but a mathematical expectation, enterprise will fade and die; — though fears of loss may have a basis no more reasonable than hopes of profit had before.

Without animal spirits there is no progress:

It is safe to say that enterprise which depends on hopes stretching into the future benefits the community as a whole. But individual initiative will only be adequate when reasonable calculation is supplemented and supported by animal spirits, so that the thought of ultimate loss which often overtakes pioneers, as experience undoubtedly tells us and them, is put aside as a healthy man puts aside the expectation of death.

Policy makers must legitimately reckon with the effects of politics and policy on animal spirits:

This means, unfortunately, not only that slumps and depressions are exaggerated in degree, but that economic prosperity is excessively dependent on a political and social atmosphere which is congenial to the average business man. If the fear of a Labour Government or a New Deal depresses enterprise, this need not be the result either of a reasonable calculation or of a plot with political intent; — it is the mere consequence of upsetting the delicate balance of spontaneous optimism. In estimating the prospects of investment, we must have regard, therefore, to the nerves and hysteria and even the digestions and reactions to the weather of those upon whose spontaneous activity it largely depends.

It's Keynes's last point that so-called Keynesians should pay more attention to. Reckoning with animal spirits does not mean that we are now somehow ruled by "the markets," as Robert Skidelsky suggested recently. It does mean giving thought to how policy can encourage animal spirits to revive -- and how policy mistakes can do further damage.

At the core of today's policy dilemma is this question: How does the government's budgetary policy influence animal spirits? It's a difficult question because it cuts both ways. Deficit spending by the government is good for animal spirits, other things being equal, because it floods the economy with demand and floats us all upwards. But other things are not equal. The deficit adds to the debt. Public debt must be financed, and a growing debt implies a rising tax burden that, looking to the future, must depress animal spirits.

So, there are two effects: deficits are a positive, but debt is a negative, and you cannot have the deficit without adding to the debt. Of the two effects, which today is the greater? It's hard to be sure, because animal spirits are as incalculable as the uncertainty to which they respond. In fact, we don't really know. On top of that, when policy outcomes are uncertain, and we fail to make a clear choice, we have policy uncertainty. As Robert Higgs has shown looking at the Great Depression, policy uncertainty is more bad news for animal spirits.

In short, there exists a Keynesian argument for decisive fiscal retrenchment now -- and it is more coherent and truer to Keynes than the positions adopted by some latter-day Keynesians. Deficit reduction is likely to take away from demand now via the spending multiplier (which may however be small, or become small or even go to zero over a few years). At the same time deficit should add to demand to the extent that it slows the accumulation of debt and encourages business confidence in the future, and also because a clear choice in favour of enterprise also builds confidence.

Contemplating deficit reduction, can we be sure of the results? No. Past behaviour gives us only rough averages as a guide; for example, Reinhart and Rogoff suggest that the median long term growth penalty for pushing debt above 90% of GDP is 1% a year. There's a lot of variation around that figure, which reduces the predictability of the outcome. So, is there an element of gamble in debt reduction now? Absolutely. But is there a safe or low-risk alternative? No.

The jobs and welfare of hundreds of millions of people are at stake in the fiscal policy game being played out now in the capitals of the West. But it's not a game we can refuse to play.

Mark Harrison

26 Jul 2010 19:36

| ![]() Tags: Economics Keynes Politics Recession

| Comments (0)

| Report a problem

Tags: Economics Keynes Politics Recession

| Comments (0)

| Report a problem

April 30, 2010

Poor Greece — Poor Us?

Greece at the mercy of "the markets." Hundreds of thousands faced with job cuts, lower salaries, and longer to work until retirement. It's hard not to feel sorry.

Equally, it's easy to understand the wrath of many Greeks: why should foreign bond holders have such power over the domestic policies of a sovereign state? Why should they accept the diktats of the IMF?

There is a simple answer. For many years, the Greek government spent far more than it raised in taxes. Why? It was the easiest way to buy votes. The problem was that the Greek government could not do it without the cooperation of others: those willing and able to lend it it.

Some of these were Greek financial institutions such as pension funds. But 80% of the Greek debt is held abroad, much of it with German and French banks. But these have walked away, taking the ball with them.

Now that the markets have called an end to the game, those who want to stand up for the entitlements of the Greek workers have to ask where the money will come from. Here are the options:

- Continue to borrow on the market -- but who will lend? The Greek debt is already at or beyond the margin of sustainability (on which more below). It is not an attractive prospect.

- If not borrow, then take. One option for the Greek government is to take from the lenders that previously enabled the years of pleasure and are now causing the pain. Taking without permision is normally called taxation. In this case it is called default. For Greece, default is all the easier because most of the lenders are abroad; they do not vote and are unlikely to throw rocks. Unilateral default has one problem: you can only do it once. After that, there is the same problem as before: if the voters want the Greek government to spend more than it raises in taxes, they must borrow. But who will lend?

- If neither borrow nor default, then print money. For most sovereign states, printing money would fix several things at once. The new money would cover the budget deficit. Then there would be inflation, but inflation would erode the real value of the debt. After that there would be a disaster, but hey ... But Greece cannot go down this road, even if it wants to. When it joined the euro, Greece gave away the right to print its own money.

- If neither borrow, nor default, nor print money, then ... raise taxes and cut spending, because there is nothing else that can be done.

These are Greece's options. In fact, the conditions that the EU and the IMF are "imposing" on Greece -- to raise taxes and cut spending -- are just what Greece must to do anyway, because there are no other choices that don't end in disaster.

Even that might not be enough. Government revenues are currently around one third Greece's GDP. If the debt heads for 140% of GDP and then stops, and must be refinanced at 10%, it follows that in future taxation must transfer 14% of GDP annually to bondholders in interest payments, and these alone will use up around 40% of Greece's limited tax capacity. Moreover, around 80% of Greek debt is held abroad, so those interest payments must shift more than a tenth of Greek GDP abroad each year -- just to cover the service on the debt, not to reduce it. The currrent EU-IMF bailout assumes that Greece's problem is liquidity. But what if it is solvency?

In that case, the future still holds the possibility of default. Given more time there will perhaps be an organized, agreed default. A rescheduling of repayments agreed with Greece's creditors will not kill Greece's credit ratings for ever, provided Greece adheres to the conditions imposed upon it.

One way of thinking about the Greek government yesterday, if not today, is that it stood at the centre of a web of obligations: legal obligations to bondholders, moral obligations to public sector employees and pensioners, and political obligations to voters. What the world has found, adding these up, is that they total far more than Greece's available resources. Something must give.

Greece holds one card, and it is an important one. If Greece goes down, so do its foreign bondholders. The German government has faced the choice between bailing out Greece and bailing out its own banks. It is interesting, and not inevitable, that the German administration has chosen in favour of Greece rather than to let Greece go and pick up its own pieces afterwards. This illustrates two things: the importance of politics, and the well known saying widely attributed to Keynes: "If I owe you a pound, I have a problem, but if I owe you a million, the problem is yours."

In all modesty, how far from Greece are we? Expectations of the British government, and what it can do for lenders, employees, the young, the old, the sick, and voters at large, have also become overstretched. Like Greece, the UK has a government that overspends, with a budget deficit of similar size relative to GDP. As in Greece, public spending is much more important to the UK economy than it should be. Even before the crisis, its importance was rising steadily; public spending accounted for nearly half of the entire increase in GDP over the period of the Blair-Brown government from 1997 to 2007. Since the start of the crisis, the growth of public spending has accelerated. Right now, public spending amounts to more than half of the UK's GDP.

In some other important ways, we are much better placed than Greece. Our aggregate debt is smaller relative to GDP, with less need for near-term refinancing. More significantly, the UK has a much greater fiscal capacity than Greece, with better coverage of tax raising institutions and less avoidance. We will be able to raise the taxes we need to finance the debt we have. And we will raise them, for another important reason: more of our debt is held at home, so lenders are also voters.

Finally, and crucially, we are not part of the eurozone. That matters, not because it will let us print money, but because it will let us recover from fiscal adjustment. The coming squeeze on spending and tax increases will put a cramp on jobs and demand from the public sector, but further depreciation against the euro and dollar will eventually rebalance the economy, allowing exports and private spending to take its place.

If there is a parallel with Greece it is not in the national picture but the regional one. For the UK as a whole, the ratio of government spending to GDP is currently a little over one half. For Ireland, Wales, and the Northeast it is between 60 and 70 percent. These regions are not only hugely dependent on public subsidies but they have no chance of renewed competitiveness through currency depreciation because, like Greece, they belong to a currency union -- in their case, the United Kingdom. What keeps them going is an unconditional year-on-year bailout from central government revenues.

My vote is not yet decided, but these are some of the reasons why I am taking seriously what the conservatives have to say about the economy today. Darling called the first phase of the crisis far more astutely than Osborne, and labour deserves credit for that. I am not convinced that more of the same will take us into a recovery.

Mark Harrison

30 Apr 2010 00:00

| ![]() Tags: Economics Greece Keynes Politics Recession

| Comments (2)

| Report a problem

Tags: Economics Greece Keynes Politics Recession

| Comments (2)

| Report a problem

April 16, 2010

Privatized Keynesianism: Rebirth After a Life That Never Was?

Writing about web page http://www3.interscience.wiley.com/journal/122498671/abstract?CRETRY=1&SRETRY=0

"Privatised Keynesianism: An Unacknowledged Policy Regime," published in the British Journal of Politics & International Relations11:3 (2009), pp. 382-399 by my Warwick colleague Colin Crouch, has been deservedly recognized and cited by scholars and journalists. The paper starts from the idea that it is a problem to maintain stability and consumer confidence under capitalism. These were secured for thirty years after the war by Keynesian demand management. After that, Crouch writes:

In those countries where capitalism was moving into full partnership with electoral democracy, it was acquiring a new vulnerability. In a fully free market, wages and employment were likely to fluctuate; would workers, who were dependent on their incomes for their level of living and lacked the cushion of wealth of propertied classes, be confident enough to consume at levels adequate to enable capitalists themselves to sustain confidence to invest and maintain profit levels? Would the very characteristics of the market that constituted its strength—flexibility, especially of labour—undermine its own ability to thrive? It should be noted that we are not here talking of the market producing social problems of insecurity in workers’ lives—that might be dealt with by an adequate welfare state—but of its producing problems for itself through its own dependence on workers’ willingness to maintain and increase their consumption. It can be assumed that the level of living at which social policy will sustain purchasing power will be below that needed to sustain an expanding, consumption-driven economy.

And he continues:

In the 1940s it had seemed that only state action could solve this problem for the market. But now, absolutely in tune with neo-liberal ideology and expectations, there was a market solution. And, through the links of these new risk markets to ordinary consumers via extended mortgages and credit card debt, the dependence of the capitalist system on rising wages, a welfare state and government demand management that had seemed essential for mass consumer confidence, had been abolished. The bases of prosperity shifted from the social democratic formula of working classes supported by government intervention to the neo-liberal conservative one of banks, stock exchanges and financial markets.

I have thought about this a lot recently, partly because my students love it -- and reproduce it for me in their essays! I have to say I don't buy it -- at least not in this form. Why am I sceptical? Well, Crouch's argument seems to be that capitalism is vulnerable to underconsumption. From 1945 through the 1970s, the argument goes, the British government ensured demand was sufficient. After the 1970s, Crouch suggests, government retreated and banks stepped in. In his eyes, British capitalism survived on credit.

The big thing here that is clearly true is that as the public debt declined, household debt rose. My problem is with the counterfactual. Implicitly, without government spending in the first phase, and credit expansion in the second, there would have been a problem: not enough demand. In the first phase, that is for most of the period up to the 1970s, it's clear that British capitalism actually suffered from too much demand; that's why there was rising inflation. In the second phase, after the 1970s, the government didn't so much step out of the picture as try to limit demand more fiercely (and hamfistedly at first), eventually delegating the job to the Bank of England. In this phase I don't really see any evidence that British capitalism was going to fall into decline if we hadn't been able to lend lots of money to the workers that they couldn't afford to pay back.

With less household borrowing and less equity realization, what would have happened? Most likely, interest rates and the exchange rate would have been a little lower, and exports would have been a little higher. With more export competitiveness, our manufacturing sector would have declined a little more slowly (and our universities might have expanded a little more). That's about it. Oh, and I guess we would be in slightly better shape today.

Ironically it is only now, in the current recession, after a huge credit crunch and collapse of private demand, that privatized Keynesianism has truly come to life. Hence, in my view, its rebirth, after a life that never was. Here is some evidence, which you'll note is tri-partisan:

-

BBC, July 23, 2009: Chancellor Alistair Darling has urged banks to lend more to small firms, during a meeting with banking bosses ... Alistair Darling has said he is "extremely concerned" that banks may be charging firms too much for loans.

-

Reuters, October 26, 2009: British retail banks should stop paying big cash bonuses and use the money instead to support new lending and contribute to an economic recovery, opposition Conservatives’ finance spokesman George Osborne said on Monday.

- The Guardian, February 23, 2010: A new government should tear up "ineffectual" lending agreements with Britain's taxpayer-owned banks and force them to lend billions of pounds more to small and medium sized businesses, Liberal Democrat Treasury spokesman Vince Cable said today.

Thanks to Colin Crouch, we know what to call it: Privatized Keynesianism. It is Keynesian because it uses debt finance to add to aggregate demand. It is privatized because the debt is private and stays off the government's books.

Now, the question is: Is privatized Keynesianism a good idea for today? Hmm. Why are we in the mess we are in? I think it might have been that we had too much private debt in the first place, so banks lent too much to firms and households that had no chance of repaying their debts unless house and stock markets floated ever upwards; and because banks did not keep enough in reserves. Where are we now? House and stock prices are still too high, and they are rising. And the solution these politicos favour is ... more private debt! The bankers are letting us down! They should be out there trying to persuade us to take out more loans! They should be keeping less in reserves!

You couldn't make it up, could you?

At this point I am going to offer one of those dire aphorisms that runs: "The only thing worse than X is -X." I apologize in advance, but there is no alternative, so here it is:

- The only thing worse than having bankers making lending decisions is to have politicians making lending decisions.

This does not mean I am complacent about the need for better financial regulation. Politicians have a role to play, and it is in setting prudential rules, limiting guarantees to retail depositors, and removing the incentives for banks to grow "too big to fail." That is a lot, but that is all. Politicians should not be making lending decisions! That is the bankers' job; let them do it.

Mark Harrison

16 Apr 2010 20:21

| ![]() Tags: Economics Keynes Politics Recession

| Comments (2)

| Report a problem

Tags: Economics Keynes Politics Recession

| Comments (2)

| Report a problem

September 23, 2009

The Essence of Keynes and the Value of Macroeconomics

Writing about web page http://www.guardian.co.uk/books/2009/aug/30/keynes-return-master-robert-skidelsky

Reviewing Keynes: The Return of the Master, by Robert Skidelsky (Allen Lane), in The Observer on August 30, 2009, Paul Krugman remarked that Keynes himself at one time considered the core of his theory to be the rejection of Say's Law (that income is always spent);

Say's Law [Krugman writes] isn't true, because in a monetary economy people can try to accumulate cash rather than real goods. And when everyone is trying to accumulate cash at the same time, which is what happened worldwide after the collapse of Lehman Brothers, the result is an end to demand, which produces a severe recession.

At another time, however, Keynes suggested that the core lay in

uncertainty that cannot be reduced to statistical probabilities, what the former US defence secretary Donald Rumsfeld called "unknown unknowns". This irreducible uncertainty [Keynes argued and Krugman writes] lies behind panics and bouts of exuberance and primarily accounts for the instability of market economies.

Krugman noted that Skidelsky himself has moved closer to the second view.

Observationally, these two views are excellent markers today for positive and negative judgements of the field of modern macroeconomics. Those that emphasize uncertainty as the fundamental problem are likely to excoriate professional economists for the false precision of their mathematical modelling, and their inability to foresee the crash of 2008.

In contrast, those that emphasize the broken relationship between supply and demand as the core insight of Keynes are likely to commend many of the same economists for their prompt reaction to the same financial crisis; they were as good as their word, speedily putting in place the massive fiscal and monetary interventions that have saved us from a repeat of the Great Depression.

In truth and logic, these insights complement each other. If Say's Law held, uncertainty would not matter. Depressions are possible because Say's Law does not hold, but it is unpredictable animal spirits that trigger them. Thus both insights are essential to Keynesian macroeconomics

That being the case, it appears that macroeconomic policy makers did not completely lose sight of what matters most. Macroeconomic theory -- well, that's another story.

Mark Harrison

23 Sep 2009 20:14

| ![]() Tags: Economics Keynes Recession

| Comments (1)

| Report a problem

Tags: Economics Keynes Recession

| Comments (1)

| Report a problem

July 27, 2009

Rationalising the Macroeconomy

Writing about web page http://www.ft.com/cms/s/0/478de136-762b-11de-9e59-00144feabdc0.html

In The Financial Times on July 21, Paul de Grauwe published the best comment I have read so far about the crisis in macroeconomic policy. If your time is scarce, don't read on; click the link and read him.

De Grauwe makes a fundamental argument, which I will summarize in four steps.

- Today, macroeconomists are distributed along a spectrum from "Keynesian" at one end and "Classical" at the other. They tend to clump at the extremes so there are many passionate Keynesians and passionate Classicals, as well as less passionate scholars in between.

- The Classical macroeconomists expect the macroeconomy to bounce back quickly from a major disturbance (for example, a credit crunch) on its own accord; government intervention is more likely to hinder than help. The Keynesians believe the opposite.

- For practical purposes, both schools model the behaviour of the people in the macroeconomy as follows: their behaviour is based on expectations of the future that are guided by the model, whether Keynesian or Classical. Classical macroeconomists assume that people's behaviour is based on the expectation that the outcome of the Classical model will be fulfilled, and Keynesian macroeconomists similarly.

- In both models, these expectations are self-fulfilling.

De Grauwe's punch line:

So what? Does it matter that economists disagree so much? It does. Take the issue of government deficits. If you want to forecast the long-term interest rate, it matters a great deal which of the two camps you believe. If you believe the first [Classical] one, you will fear future inflation and you will sell long-term government bonds. As a result, bond prices will drop and rates will rise. You will have made a reality of the fears of the first camp. But if you believe the story told by the second [Keynesian] camp, you will happily buy long-term government bonds, allowing the government to spend without a surge in rates, thereby contributing to a recovery that the second camp predicts will follow from high budget deficits.

In short, in a Keynesian model, the agents are assumed to expect that a credit crunch will have lasting adverse consequences. As a result they will rein in consumption (because households expect lower incomes) and investent (because firms expect depressed markets). The economy will stay depressed until government action flips the economy back to normal. But in a Classical model, the agents are assumed to expect that a credit crunch will soon be overcome, provided markets are allowed to work normally. Do nothing, and any damage to confidence will soon be restored. Unnecessary government action, however, by enlarging public spending and debt, will depress long term expectations and so inhibit the restoration of confidence.

This point is not new. I'm not sure who made it originally. It has been around a long time. I checked my notes from 1998/99, the first year I lectured to first year undergraduates at Warwick on this particular topic. I found the following passage:

We’re trying to explain a state of the world in which at least some unemployment is involuntary, money isn’t instantly neutralised by price change, and business cycles last anywhere between 5 and 9 years. The fundamental problem of the RE [rational expectations] approach is that it proves this state of the world can’t exist. Underlying this are some basic conceptual faultlines. Learning from experience may be more difficult than RE theory assumes. Large experiments are rarely if ever repeated under controlled conditions (e.g. joining, then leaving the ERM). Large shocks (e.g. oil shocks, monetary shocks) make it hard to discern the underlying things which remain the same. What is the true model of the macroeconomy? RE theorists tend to assume that most people adhere to a Classical philosophy. But since economists have such difficulty decided how best to model the economy, it’s not clear why rational non-economists should be different. Policy demonstrably does affect the real economy, so why should rational people believe it won’t? This is particularly important since the outcomes of actions based on RE tend to force the world to conform to the model, not the other way round. What is created here is a "guessing the winner" problem: what’s important in forming rational expectations is not "how does the economy work?"; nor even "how does the economy work in my opinion?"; but "how does the economy work in most people’s opinion", bearing in mind that in forming their opinions they are all asking themselves the same question.

I claim absolutely no credit for this; I was not saying anything original. I got the argument from somewhere or someone else. My point is that the basic paradox in rational expectations has been understood for a long time, but the horrendous policy implications are perhaps only now fully apparent.

How bad does that make economists? Ten years ago I told my students that the idea of rational expectations, although not wrong, contained a paradox. I had no idea how to resolve it, however. One route the profession has taken has been to consider that, just as economists learn, so do non-economists. As a result, macroeconomic models have been developed that incorporate heterogeneous expectations -- when different people in the macroeconomy start out with different models of how the economy works and so different forecasts of the future -- and model how they might then learn from experience. A recent review by George W. Evans and Seppo Honkapohja is here.

This takes me well outside my comfort zone. I thought about it, however, when a friend forwarded some lines from an internet discussion including the suggestion:

Until the "science" of economics detaches itself from econometrics and unilateral modelling and realises that humans are "rationalising beings", not "rational beings", then the predictions and opinions stemming from its adherents should be treated with caution.

In the context I took the gap between "rationality" and "rationality" to reflect some falling short of cognition or computation. It wasn't that I disagreed; the suggestion seemed almost trivially true (apart from the reference to econometrics, which seemed silly). What it made me think is this: If humans are "rationalising beings," then so too, being human, are economists. All economic models have cognitive and computational limits. They model reality; they don't and can't reproduce it.

In the often misquoted words of George Box and Norman Draper (from Empirical Model-Building and Response Surfaces, New York: John Wiley 1987, p. 63):

All models are wrong; the question is how wrong do they have to be to not be useful.

Mark Harrison

27 Jul 2009 09:15

| ![]() Tags: Economics Keynes Politics Recession

| Comments (3)

| Report a problem

Tags: Economics Keynes Politics Recession

| Comments (3)

| Report a problem

February 23, 2009

New Romantics

Writing about web page http://www.guardian.co.uk/commentisfree/2009/feb/20/economics-emotions-human-values

There is a strong case for thinking about how emotion and mood affect economic decisions.

Does my own mood affect my decisions? I discussed this with my wife, and she agreed I'm a model of level headed rationality. But she knows lots of people for whom that wouldn't be true. She's not saying who (but I bet they're not economists).

If mood can affect decisions, does it affect the decisions that really matter? Not all decisions are important. But isn't it at least possible that powerful emotions like joy, fear, sadness, or enthusiasm interfere with our ability to calculate an optimum? Suppose that emotions frame our vision of the future; suppose they are capable of boosting our willingness to provide for the future or winding it down; suppose they make us more or less willing to shoulder risks. In that case, important economic decisions will indeed swing with our moods.

Again the net effect, averaged across millions people, might not add up to much. If one person's mood cancels out another's, the total effect should be zero. But if the moods of millions swing together, in a concerted way, billiions of pounds could swing with them into -- or out of -- particular markets.

And it is intuitively plausible, to say the least, that the mood of millions of people is taking a hit at the moment, as homes and jobs are lost and the fear of loss infects our nation.

As Jon Elster pointed out some years ago in The Journal of Economic Literature (1998), economists have given much closer attention to cognitive limits on rationality than to emotional limits.

Which brings us to the critics of orthodox economics. There are so many at the moment ... it seems invidious to pick and choose. But choose we must, so we'll pick from my daily newspaper which, despite the fact that it is written mainly by and for lunatics, remains The Guardian. On February 16, 2009, Larry Elliott wrote:

There have been many economists down the years who have expressed scepticism about reducing their discipline to a mechanistic subject. Malthus told Ricardo to be wary of becoming too attached to abstract hypotheses; Schumpeter talked of creative destruction; Hayek saw the market as a voyage of discovery; Keynes stressed the importance of "animal spirits."

And:

Mervyn King says Britain is in a deep recession ... Interestingly, the governor cited Keynes at the Bank's inflation report press conference, noting that animal spirits were currently depressed. With confidence so weak, it is hard to envisage an early or a robust recovery.

Two days later, Sam Whimster (Professor of Sociology at London Metropolitan), commented:

We should also consider the place of emotions in economic life. The share price of UK banks fluctuates wildly as traders attempt to calculate their capital value from future estimated losses and profits. Keynes, in 1933 in his lectures on his General Theory, said that current yields of firms exercise an "irrational" influence on estimating future worth.

In the boom years that have ended so abruptly, Whimster continues:

Infectious greed and optimism was the mindset of economists, bankers, politicians and regulators - leading to behaviour that no regulatory mechanism could have controlled. But the extent of the greed and adventurism, and the flouting of standard banking precautions which had been stress-tested by decades of history, raises the question of what determines which emotions come to the fore.

The question of whether economists should take emotions into account is a good one. But where are the answers? Not as easily to hand as one might hope. Let me mention some issues that everyone should think about at this point.

To begin with, emotions are just one more variable. There is a lot going on in the world economy that we understand all too imperfectly. But it doesn't help our understanding to say, after the event: Oh -- people have been behaving irrationally, it must be because of their emotions. Change the context a little and you'll see how fainthearted and pathetic this is. Imagine me telling my wife: You've been behaving irrationally, it must be because of your emotions. (I can't imagine saying it, but you can try.) She'd kill me, and rightly so. The reason is not just that it's insufferably patronising, but that it also devalues emotions into something irrational, flighty, whimsical, and beyond understanding.