All 8 entries tagged Using-Data

No other Warwick Blogs use the tag Using-Data on entries | View entries tagged Using-Data at Technorati | There are no images tagged Using-Data on this blog

December 13, 2014

Was the Soviet 1923 Male Birth Cohort Doomed by World War II?

Writing about web page http://downloads.bbc.co.uk/podcasts/radio4/moreorless/moreorless_20141213-0600d.mp3

Tim Harford's BBC Radio programme "More or Less" asked me to comment on a claim that is widely repeated on the internet, for example on Buzzfeed:

Almost 80% of the males born in the Soviet Union in 1923 did not survive World War II.

My answer

Here's the numbers I worked from on the programme(in thousands, rounded to the nearest hundred thousand). Each of the lines is sourced below.

- Males born in the Soviet Union in 1923: 3,400

- Infant (0-1) mortality: 800

- Childhood (1-18) mortality, famine, and terror: 800

- Surviving to 1941: 1,800

- Wartime mortality: 700

- Surviving to 1946: 1,100

My comment

The Buzzfeed claim is overstated, although not by a wide margin. Around two thirds (more exactly, 68%) of the original 1923 male birth cohort did not survive World War II. But the war is not the most important reason for the poor survival rate; almost half of them died before the war broke out.

The babies of 1923 were born at an awful time and faced a dismal future. The country they were born in was poor and violent. Between 1914 and 1921 their families had endured seven years of war and civil war, immediately followed by a major famine. Their society lacked modern sanitation, immunization programmes, and antibiotics. Rates of infant mortality and childhood mortality were shockingly high. Moreover, violence and famine were not a thing of the past. The 1923 cohort would be aged nine in the first year of the next major famine (1932) and fourteen in the year of Stalin's Great Terror (1937). They turned eighteen just as Germany attacked their country (1941).

The German invasion of 1941 was a deep national trauma. The young men born in 1923 were inexperienced conscripts for an army that was repeatedly shocked, taken by surprise, encircled, and pulverized. It suffered terrible losses. In the first six months, three million troops were killed or taken prisoner, and most of those taken prisoner did not survive. If they survived that, they faced more years of battlefield attrition or else and exhaustion on the home front. In all the Soviet Union suffered around 25 million war deaths, plus or minus a million (Harrison 2003). Red Army deaths alone were 8.7 million.

The overall mortality of the Soviet 1923 male birth cohort can be distributed over four stages of life. Around 800 thousand died in their first year. These died of birth defects, disease, accidents, abuse, and neglect. Another 800 thousand died between the ages of 1 and 18 from a range of causes that included those just mentioned and extended beyond them to famine and political violence. Then, from age 18 to 22, another 700 thousand were carried off in the war. That left just over a million to live on into middle and old age.

It may be surprising that war was not the major cause of premature death up to 1946 for the young men born in 1923. But in this there should be two harsh reminders. The first reminder is that nature is wasteful: everywhere until very recently only a minority of babies survived to adulthood, even in peacetime. This was still the situation for the Soviet Union in 1923. The second reminder is that 700,000 wartime deaths from a single birth cohort of young men is still a shocking figure. It is, for example, more than twice the total number of British military and civilian casualties in World War II.

My working

I took the data from Andreev, Darskii, and Khar'kova (1993). These three Russian demographers reworked the Soviet census and registration records immediately after the collapse of the Soviet Union opened up the archives for independent research. Everyone abbreviates the reference to ADK so I will too. ADK (p. 118) give the total of births in the Soviet Union in 1923 as 6,523 thousand. Assuming a normal male/female split of 107/100, male births were 3,372 thousand. This is the size of the 1923 male cohort that we have to reckon with.

ADK do not give exact figures for the numbers of the 1923 male cohort surviving to 1941 and 1946, but you can read them off a chart (p. 79) as approximately 2 million and 1.2 million, implying 800 thousand wartime deaths. For our purpose, however, these figures require adjustment for border changes. In 1946 Soviet borders were wider than in 1923. In 1939/40 the Soviet Union expanded to absorb the Baltics, eastern Poland, and some other territories. Because of this the population was boosted (p. 118 again) from 168.5 to 188.8 million, or about 12 percent). So we need to multiply by 168.5/188.8 to take the 1923 male birth cohort as reported in 1946 back to the original borders of 1923. This gives survivors to 1941 as 1,785 thousand, wartime deaths as 714 thousand, and 1,071 thousand survivors to 1946.

A cross-check

If these figures are right, two thirds (rather than 80 per cent) of the original 1923 male birth cohort were dead by the end of World War II. But the war was not the largest cause of death, for nearly half of them were dead by 1941, before the war broke out. How reasonable is that?

There are two factors that explain heavy peacetime mortality. First, infant mortality: ADK give infant mortality in 1923 (p. 135) as 229 per thousand (with 220 as a lower bound and 238 as an upper bound). Applying their central estimate gives 770 thousand deaths in the first year of life, leaving 2,600 thousand survivors to 1924.

Second, childhood mortality, famine, and violence. For consistency with 1,785 survivors in 1941, we obtain deaths over the period from 1924 to 1941 as a residual, and the number of these is found to be 814 thousand, which is a larger number than the number of deaths in the first year of life. Is that reasonable? Elsewhere (pp. 19, 20. 35), ADK give survival tables for male newborns based on the three interwar censuses, from which it is clear that male child mortality over 1 to 3 years was never much less than over 0 to 1. Taking into account famine, terror, etc., a figure for 1-18 mortality that slightly exceeds 0-1 mortality is plausible.

Soviet demography is not an exact science. All these figures are more fuzzy than might appear at first sight -- one reason my opening summary rounds everything to the nearest hundred thousand. On the same programme you can hear Mike Haynes (he and I reach similar conclusions) reminding listeners that the error margin on Soviet war deaths, plus or minus one million, is another number that is greater than the number of British war deaths. The one thing that saves us from complete confusion is that demographic accounts have to be consistent, both internally and externally. The requirement of consistency helps us to judge that some claims are reasonable and others are ruled out.

References

- Andreev, E. M., L. E. Darskii, and T. L. Kharkova. 1993. Naselenie Sovetskogo Soiuza, 1922-1991. Moscow: Nauka.

- Harrison, Mark. 2003. Counting Soviet Deaths in the Great Patriotic War: Comment. Europe-Asia Studies 55:6, pp. 939-44.

Mark Harrison

13 Dec 2014 17:16

|

Mark Harrison

13 Dec 2014 17:16

| ![]() Tags: Politics Russia Using-Data War

|

Tags: Politics Russia Using-Data War

|  Comments (0)

|

Comments (0)

|  Report a problem

Report a problem

Please wait - comments are loading

Please wait - comments are loading

September 11, 2014

British Growth is Best in the World — Since When?

Writing about web page http://www.telegraph.co.uk/finance/economics/11036043/Top-of-the-world-UK-economy-winning-global-growth-race.html

Summary: On a restricted definition of "the world" (limiting it to our neighbours of similar size in northwestern Europe), British growth is best in the world since ... well, since 2012. This shouldn't count for much. More importantly, and perhaps surprisingly, British growth is also best in "the world" since the 1970s. To go on to a more tendentious point, the economy of the United Kingdom appears to be benefiting still from the relative growth advantage that it gained in the Margaret Thatcher years. I thought I'd mention this while the UK still exists.

Here's the full argument, with evidence. To start with, just how well is the UK economy doing at the moment? Here are the top three results of a Google search on "British growth best in world":

- Top of the world: UK economy winning global growth race (The Telegraph, 15 August 2014)

- UK economy now best in the world as new figures show (The Daily Mail, 15 August 2014)>

- Britain will be best performing of the world's largest economies in 2014 (The Guardian, 8 April 2014)

These have been recent headlines, but anyone with a little knowledge of recent economic history knows it's not so simple. The UK economy is growing fast, in part, because it is making a belated recovery from its deepest postwar recession, which began in 2008. In the crisis, the UK economy went down hard. As the crisis wore on the economy continued to perform dismally, with recovery continually postponed. In that setting, Britain's current rapid growth is no more than partial compensation for its underperformance earlier in the recession.

In other words, how well the British economy is performing today depends critically on when you start the clock. If you start it from yesterday, the British economy looks great. If you start from a few years back, its performance looks unimpressive at best.

How far back should you go? While the previous peak, in 2007, is a natural reference point, it is still only a few years ago. As an economic historian I'd prefer to take a longer view. How well is the British economy doing today, relative to other countries, if we shift the starting point still further back into the past? This is an easy thing to do, and it produces some surprises.

Here's what I did: I found figures for the real GDP of the United Kingdom and of five European neighbours, per head of the population. These neighbours are Belgium, France, Germany, Italy, and Netherlands. I chose these because they are not only nearby, but also because they are important trading partners, comparable to the UK in both income levels and economic size. The result is a small sample, but this is just a blog and I want to make a simple point. Anyone can repeat the exercise with more countries and then you will naturally find a more nuanced story. I looked at each country's growth rate comparing 2013 with every previous year: 2012, 2011, 2010, and so on, back to 1950. Germany is in the data, but only back to 1990, because before that it was two countries, and you cannot easily compare Germany today with West Germany in, say, 1970 or 1950. Finally, I worked out Britain's rank among the six countries (five before 1990) based on its growth rate up to 2013, starting from every one of the preceding years.

The chart below shows the result. It plots Britain's rank compared with our European benchmark competitors, based on growth rates of average incomes up to 2013, and it shows how that rank depends on the year you start from. In other words it answers the question: British growth is best in "the world" -- since when?

Source: Data for real GDP per head of the population in international (Geary-Khamis) dollars and 1990 prices are from The Conference Board Total Economy Database,January 2014,

Notes:

Each data point is the UK's relative position among five or six West European countries, based on the increase in real GDP per head in 2013 over its level in the base year shown. Countries are Belgium, France, Germany (from 1990, the year of East and West German reunification), Italy, Netherlands, and the United Kingdom. Because Germany is counted only from 1990, there are six countries from the present to 1990 (red squares), but only five before that year (blue squares).

Here's how to read the chart. As of 2013, Britain's growth is best in "the world" (OK, the little world of our Western European neighbourhood) since ... well, since 2012. But there is more! As of 2013, Britain's growth is also best in "the world" since 1995, 1994, ... and since every previous year right back to 1970. Now I'll discuss this in more detail.

If you measure Britain's growth over the last twelve months that are shown, from 2012 to 2013 Britain's performance was the best of the six countries. So, the red square on the far left puts Britain in first place out of six. For those who prefer numbers, here they are (and they remind us that economic recovery has been pretty anaemic everywhere):

- United Kingdom 0.8% growth of GDP/head, 2012 to 2013

- Germany 0.6%

- Belgium 0.0%

- France -0.3%

- Netherlands -0.9%

- Italy -1.1%

The chart also shows how Britain's relative position collapses as we move the starting point back to the beginning of the global crisis. Thus, the red squares to the right of 2012 and back to 2007 fall back to the second, third, and fourth ranks. If we start the growth story on the eve of the Great Recession, British growth to the present is nearly worst in "the world," ranked fifth (out of six):

- Germany 1.1% average annual growth of GDP/head, 2007 to 2013

- Belgium 0.3%

- France -0.5%

- Netherlands -0.8%

- United Kingdom -1.1%

- Italy -2.2%

Now for a surprise. As you take the starting point further back into the twentieth century, Britain's relative performance starts to look better and better. The red and then blue squares reflect this by rising back up to show Britain recovering to fourth, third, and second place, and eventally back to first place. If, for example, you wind the clock right back to 1979, the year that Margaret Thatcher took office, then British growth from that year to the present is faster than of any of the other European economies in the sample (which now excludes Germany). Here are the figures:

- United Kingdom 1.9% average annual growth of GDP/head, 1979 to 2013

- Belgium 1.7%

- Netherlands 1.5%

- France 1.2%

- Italy 1.0%

Note: Britain's relative growth advantage is seen for a whole run of starting points, beginning in 1995 and ending in 1970. This does not mean that the turnaround in Britain's fortunes began in 1970, for in the 1970s British economic performance remained relatively poor. The turnaround began in the 1980s under Margaret Thatcher. At that time Britain began to grow faster, just as our European neighbours decelerated. The way our chart looks at things, however, the benefits of that turnaround cast a beneficial "shadow" back onto earlier years, considered as starting points for the measurement of growth.

Finally, you can push the starting point right back into the 1960s and 1950s, but eventually relatively slow British growth in the so-called Golden Age of Brettton Woods takes its toll, so that Britain's ranking slips back down again to the bottom. Here are the last figures:

- Italy 2.7% average annual growth of GDP/head, 1950 to 2013

- Belgium 2.4%

- France 2.3%

- Netherlands 2.2%

- United Kingdom 2.0%

Note: There's a surprise here for Italians. In almost all these estimates Italian growth has been worst in "the world"; notoriously, Italian incomes have marked time over the last 20 years. The surprise is that if you measure growth since 1950, Italian performance shows up as best in "the world"! That's the legacy of a postwar economic miracle: Italian incomes tripled in just two decades from 1950 to 1970.

Here's my bottom line. Just how good is British economic performance today? The answer depends critically on "Since when?"

- The British economy has done relatively well since 2011, outpacing our nearest European competitors. But this is no surprise, because British economic performance was so spectacularly poor in earlier years of the Great Recession.

- The British economy has done relatively well since the 1970s, and this deserves greater recognition. Even today, despite the dismal experience of the Great Recession, the British economy continues to benefit from its reversal of fortunes under Margaret Thatcher.

Mark Harrison

11 Sep 2014 15:06

| ![]() Tags: Economics Recession Thatcher Using-Data

| Comments (0)

| Report a problem

Tags: Economics Recession Thatcher Using-Data

| Comments (0)

| Report a problem

April 26, 2011

The History of Britain's Public Debt Does Not Give Grounds for Complacency

Writing about web page http://www.johannhari.com/2011/03/29/the-biggest-lie-in-british-politics

Twice recently, the journalist Johann Hari has suggested that we are going through a manufactured crisis. The history of Britain's public debt, he argues, show that present levels are modest and there is no need for precipitate action to restrain government spending:

Here’s the lie. We are in a debt crisis. Our national debt is dangerously and historically high. We are being threatened by the international bond markets. The way out is to eradicate our deficit rapidly. Only that will restore “confidence”, and therefore economic growth. Every step of this program is false, and endangers you.

Let’s start with a fact that should be on billboards across the land. As a proportion of GDP, Britain’s national debt has been higher than it is now for 200 of the past 250 years.

The quote is from Johann Hari's blog, The biggest lie in British politics(March 29, 2011). Before that, in When will David Cameron's soufflé of spin collapse?(February 11, 2011) Hari wrote:

Beneath Cameron's entire agenda runs the biggest lie of all: that Britain is facing an "unprecedented" level of debt. In reality, Britain's national debt has been higher as a proportion of GDP for 200 of the past 250 years.

The full argument, widely blogged and tweeted, goes like this:

- Current debt levels are historically modest.

- So, there is no need for drastic action to contain the debt through deficit reduction.

- In fact, advocates of public spending reductions are creating a phoney sense of emergency in order to vandalize the welfare state for other reasons.

On a closer look, this line of reasoning raises interesting issues. Here is a chart that shows the evolution of Britain's public debt as a percent of national income since 1692:

(The figures from 1692 to 2010, and a forecast for 2011, compiled by Christopher Chantrill, can be found at http://www.ukpublicspending.co.uk/. I added the Office of Budget Responsibility forecasts for 2012 to 2014.)

First, is it true that Britain’s current debt level is historically modest? Yes, clearly -- although Hari exaggerates. As of 2011, Britain's debt ratio has been higher than it is now for just 169 (not 200) of the last 250 years (or you could say "200 of the last 282 years").

Next, is there anything else of interest in these figures? Well, since the level of debt today is the sum of past changes, we could also look at the rate of change of Britain’s public debt. Interestingly, there have been just 36 years in the last 320 when the debt grew faster as a percent of GDP than in 2009 to 2011. Let me give some twentieth century examples, and you'll get the idea. One run of years when the public debt climbed faster was 1915 to 1919. Another was 1941 to 1946.

In other words, Britain's debt has been growing in the last couple of years at rates generally exceeded only in major wars. It's particularly dangerous because, as I explained here, debt has persistence. Once the conditions have been created for it to grow rapidly, it'll go on rising under its own momentum until you take steps to control it. The longer you leave it, the harder it gets.

In some general sense, however, Hari has a point. It's true that Britain’s debt has been higher than it is now for more than two of the last three centuries. He overstates the case, which I dislike, but I accept that most policy advocates do that most of the time, and they can't all be wrong at once.

Now, some economic history. My point here is that there are important reasons why Britain today cannot handle the 200% plus debt ratios that characterized the 1820s (after the Wars of the Austrian and Spanish Successions, the Seven Years' War, and the Napoleonic Wars) and the 1950s (after World Wars I and II). If much higher debt levels were okay then, why not now? The answer begins with: because times have changed. We no longer live in the 1820s or the 1950s. It’s the twenty-first century.

How did Britain sustain that kind of debt in the past? Well, how do you handle a debt that is twice your income? The important thing is that you have to be able somehow to limit the interest payments. If debt is twice national income, as long as you can borrow at no more than 3%, you have to transfer only 6% of national income each year to bond holders. But, if the interest rate goes up to 12.5% (as it is today for Greece and Ireland) then the transfer eventually goes up to an infeasible 25% of national income. Basically, you’re insolvent.

How do you keep the interest rate down to 3%? In one of two ways. Either you dominate the world capital market – as Britain did in the eighteenth and nineteenth centuries. Or, you close the domestic capital market off from the world, so you can dominate your own little pool of saving – as Britain did in the mid-twentieth century. Either way, you can borrow if there's no one else for people to lend to.

In the eighteenth and nineteenth centuries, Britain could handle a much higher debt ratio than today’s because an integrated global capital market developed in which the British economy was the major borrower and lender. There was little credible competition with British bonds. As a result, British public debt remained universally acceptable despite its relative abundance. (The United States has enjoyed a similar position since World War II, but the uncontrolled U.S. budget deficit may eventually put an end to that.)

Before the twentieth century, moreover, the British government did not have major commitments to social spending at home. The spending of the central government was principally on administration and defence. As a use of government revenue, interest payments did not have to compete with major entitlement claims. This kept government guarantees of repayment credible.

The two world wars broke up the global capital market. Although no longer the world's financier, in the mid-twentieth century Britain could continue to handle a much higher debt ratio than today’s for a reason that was completely different from before. In a closed domestic capital market, British bonds were protected from competition. British lenders could not freely buy the bonds of other countries, even if they wanted to, because of government controls on foreign exchange and capital movements. With alternatives kept out of the market, British public debt continued to be acceptable at home.

Today, these conditions have gone. There is a global capital market again. British bonds have no specific advantage for foreign lenders (as they had in the eighteenth and nineteenth centuries), and domestic lenders can pick and choose among bonds issued by many countries (something they could not do in the middle of the twentieth century).

This is why a level of debt that was sustainable decades or centuries ago is not sustainable today. Today, no one has to lend to the British government for lack of alternatives. In short, whether or not it is true, it is irrelevant that "Britain’s national debt has been higher than it is now for 200 of the past 250 years." The conditions of those 200 years have gone.

Here is the first reason why it is important for the British government to control the level of public debt: the day of reckoning would be upon us if we didn't. A combination of rising debt, declining confidence, and rising interest rates would then force us to close the budget deficit even faster than planned at present. The world doesn't owe us a living; we already owe them. In fact, don't feel sorry for us; feel sorry for Americans that the U.S. Treasury has enough discretion to put off its day of reckoning until the fiscal mess there will be still more dire than it is now.

The world has changed; for Britain, has it changed for better or worse? Some people might think "for worse." There are those that don't like globalization on principle; others might wonder, more pragmatically, whether the conditions of the capital market half a century ago could be restored. Talk of capital controls is in the air again. If capital account liberalization made it more difficult for us to carry on with deficit spending and a rising public debt, then why not restore the protected capital market regime of the 1950s?

The case might be that, by restricting the choices of British lenders again, we could increase the domestic demand for British debt. (By the same token, however, we would also eliminate the foreign demand.) On closer inspection, this course of action hardly recommends itself. When lenders lose the will to lend, as with Greece, Ireland, and Portugal, it is usually for good reason. Taking away their option to buy elsewhere would amount to sticking fingers in our ears so as not to hear bad news.

Besides, if we restored the conditions that enabled the government to borrow more than twice GDP, what reason is there to suppose that the government would make better use of the money than private borrowers? Still one of the richest countries in the world, Britain’s prosperity has come from private enterprise and innovation, industrial and commercial revolution, and trade and finance; it did not come from Whitehall.

To finish up, the second reason for fixing Britain's debt while it is still at today's historically "modest" level is that having a debt twice your income is a sign that something went terribly wrong; a run of major wars, for example. Faced with the worst recession in 80 years, the British government was right to let its budget go into deficit temporarily. At that moment an increase in Britain's debt was inevitable. Now it's right to bring it back under control over a few years.

So, if the British government today cannot dominate its capital market and continue to eat up national resources beyond the willingness of the population to pay taxes -- there is reason to be glad.

Mark Harrison

26 Apr 2011 18:18

| ![]() Tags: Economics Keynes Recession Using-Data

| Comments (0)

| Report a problem

Tags: Economics Keynes Recession Using-Data

| Comments (0)

| Report a problem

April 24, 2011

Surely You're Joking, Mr Keynes?

Writing about web page http://www.debtonation.org/wp-content/uploads/2010/06/Fiscal-Consolidation1.pdf

The British government is seeking to bring the public debt under control by cutting back public spending. A popular story is going around, however, that suggests this is either crazy or a thinly disguised plot to undermine the public sector; see for example Johann Hari's blog, The biggest lie in British politics, March 29, 2011.

How does this story work? It runs like this. Start from the government’s plan for cutting public spending:

- With lower spending, the national income will fall.

- With lower national income, tax revenues will fall.

- With lower tax revenues, public borrowing will remain high.

- With public borrowing still high, the public debt will be hard to shrink.

- The burden of the debt relative to GDP could even rise.

In this story, the public debt is hard to control because it pushes back when the government tries to cut spending. It pushes back so hard that cutting public spending is actually counter-productive. In fact, the story implies that the government should spend its way out of debt! This is because more public spending would generate higher national income, higher tax revenues, less borrowing, and less debt relative to GDP.

How good is this story? It has a logic, purely Keynesian in spirit. But is it true? One issue could be that it leaves such factors as business confidence and the exchange rate out of the calculation. Ultimately, however, it’s an empirical question. That is, it can be answered by looking at how the public debt has actually responded to changes in public spending in the historical record.

It’s clear how both the UK Treasury and the independent Office of Budget Responsibility answer this question. They predict that, with the current fiscal squeeze, Britain’s public debt will rise more slowly, peak in 2014 at around 70 percent of GDP, and then start to fall. In other words, deficit reduction will eventually win. Given enough time, cutting public spending will not be counterproductive.

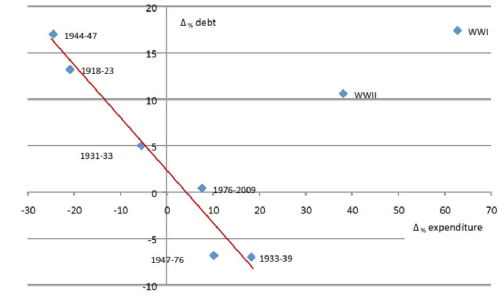

The Economic Consequences of Mr Osborne is a paper that Victoria Chick (of UCL) and Ann Pettifor (of the New Economics Foundation) circulated in June last year. It tells a more pessimistic story. It uses a century of data to suggest that the public debt varies negatively, not positively, with public spending. Fiscal cutbacks, they conclude, have consistently increased, not reduced, the burden of public debt. The key result is illustrated by their figure, below. The figure compares the change in the burden of the debt relative to GDP (the vertical axis) with the percent change in nominal public spending on goods and services (the horizontal axis), measured in annual averages over varying periods of time. The idea, I guess, is that nominal spending is the one thing over which the government has direct control; how does it affect the burden of the debt?

This chart suggests that a change in the public debt is negatively associated with a change in nominal public spending. When public spending falls, debt rises. Chick and Pettifor also report this result as a regression (the Δ symbol means “change in”):

Δ public debt/GDP = 2.2 – 0.6 x Δ public spending

Notes:

- The 2.2 means that the public debt would have risen on average by 2.2 percent of GDP per year in every episode if public spending remained unchanged.

- The 0.6 means that, in addition, debt tended to rise by 0.6 percent of GDP for each one percent cut in nominal public spending.

- Chick and Pettifor state that this relationship explains 98 percent of the total peacetime variation in the debt.

There are two implications. One is that deficit reduction is pointless because it will worsen the burden of the debt. The other is that the government can and should spend, not save its way out of debt.

This finding has been widely blogged and tweeted. It even made its way into a quarterly newsletter of the Royal Economic Society. But I have not seen any serious commentary so far. So, let me try. To begin, there are four odd things about the picture in the chart.

- The compression of 100 years of annual data into eight data points.

- The exclusion of the two data points that don’t fit (the two World Wars).

- The six data points that are used to fit the line are very different in coverage, ranging from two years (1931 to 1933) to 32 years (1976 to 2009).

- Regardless of the length of the period covered by each data point, the effect of public spending on debt is assumed to be exactly contemporaneous.

Is this a sufficient basis for a very important policy prescription? In my view, absolutely not.

Let’s look again at the data, which Chick and Pettifor helpfully provide in an appendix. Like them, I'll use nominal public spending changes to try to predict changes in the public debt burden. Unlike them, I’ll use all the data. I won't leave out any inconvenient observations. I’ll work on the basis that, if the relationship we are looking for exists, it ought to be simple and direct; it should not be instantaneous, but it should be speedy; and it should be there, year on year, in every period, regardless of other circumstances.

One other thing I'll do differently: Remember the 2.2 percentage points a year of upward drift in the debt burden that Chick and Pettifor found. Remember also the official forecasts that expect the Osborne budget cuts at first only to slow the growth of the public debt; not until 2014 will the debt start to fall relative to GDP. This reflects an important problem that Chick and Pettifor left out of account: the burden of debt has a momentum of its own.

What does this mean? Suppose there is a lot of public borrowing, causing the debt to rise rapidly. If the government reduces its deficit but does not eliminate it, the public debt will go on rising, but more slowly. It will not fall until the deficit is closed altogether. Moreover, while it is rising, the additional interest payments will be added to the debt, increasing it further. In other words, whether or not there is pushback in the public debt, there is certainly persistence. This is matched by the data, which suggest that public debt has moved systematically up or down over long periods under its own momentum. You can't ignore this if you want to understand how current fiscal policies affect the evolution of the debt.

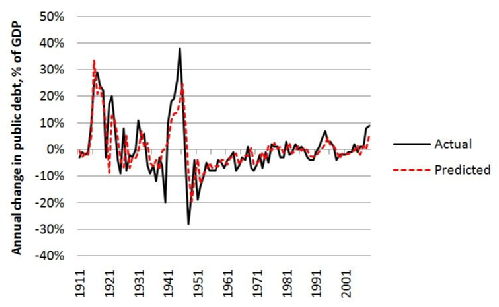

My own calculation uses year-on-year changes in public spending (percent of previous year) and public debt (percent of GDP) from the Chick-Pettifor data. It allows the change in the public debt in a given year to be influenced by not one but two things, both in the previous year: how public spending was changing, and how the debt itself was changing. Including the latter means we can work out the historical persistence factor in the change in the debt from one year to next year. Using Δ to mean “change in” and “(-1) to mean “in the year before,” here are the numbers that come out:

Δ public debt/GDP = -0.01 + 0.74 x Δ public debt/GDP (-1) + 0.14 x Δ public spending (-1)

Notes:

- The 0.74 means there is quite a lot of persistence in the debt: if public spending was unchanging, but the public debt increased by one percent of GDP, it would increase again by 0.74 percent the following year.

- The 0.14 means that the historical relationship between a change in the public debt and the change in public spending one year previously is actually positive. This is the most important result. Allowing for the persistence factor, if the government increased nominal public spending by 1 percent, the public debt tended to rise by 0.14 percent of GDP the following year.

- The explanatory power in this relationship is quite high. For the experts, the t-ratios of the 0.74 and the 0.14 are 11.0 and 5.2 respectively, meaning that the probabilities of finding this pattern by accident are extremely low. Nearly 60 percent of the total historical variation of the change in the public debt is explained. Of course, this is much less than the 98 percent that Chick and Pettifor say their model explains. I set myself a far stiffer test, however, by using 98 (not 6) observations, so that there is much more variation in the data to be explained. I also included all the years that Chick and Pettifor arbitrarily dropped in order to get their result.

The next figure shows how well the regression equation predicts the actual year-on-year changes in the debt ratio over the whole period.

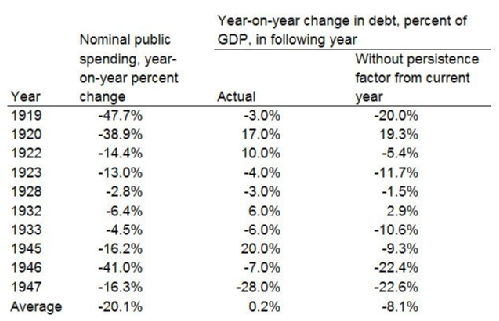

As a final check, I narrowed my focus down to those years in which nominal public spending actually fell. Public spending was unlikely to fall without a deliberate government policy of fiscal consolidation. Never mind what happened on average across the century as a whole; what happened to the public debt when the government took an axe to public spending? There were just ten such years within the sample. This is what happened in them.

The first column shows that in these years nominal public spending was cut on average by 20 percent. The second column shows that in the next year the debt burden did not fall on average, and even rose slightly. Perhaps Chick and Pettifor would see this as validation of their idea. But it ignores the persistence factor in the debt. In most years that public spending was cut, there was already a large deficit that fuelled rapid growth of the debt. Unless the deficit was eliminated immediately, the debt would still grow, but at a slower rate. In the third column, I estimate how the debt would have behaved without the inherited momentum. On that basis, the debt would have fallen in eight of the ten years shown, and it would have fallen on average by 8 percent of GDP.

I'd never claim that this is the best that can be done. I do claim that, if you treat the same data properly, they can tell a very different story from the one that Chick and Pettifor come up with.

To sum up: Deficit reduction works. As for the Chick-Pettifor story, it is not completely wrong. There is a grain of truth in it. Once the public debt is set on a particular course, it is hard to change that course quickly. But it is just persistence that takes time to reverse; it is not a pushback so strong that trying to controll it becomes pointless or counterproductive. Once we allow for the momentum of the debt burden, we can uncover the simple, intuitive, positive relationship between spending and debt that even a non-economist might expect to find.

At the beginning I outlined a Keynesian story that starts with deficit reduction and ends with an increased burden of the debt. It is an intriguing story and it is popular among those that are easily satisfied when a result seems to match their preconceptions. But, like many intriguing stories, it is a fiction. What the figures actually show is that more public spending means more public debt.

Spend our way out of debt? Surely you’re joking, Mr Keynes.

Mark Harrison

24 Apr 2011 23:11

| ![]() Tags: Economics Keynes Recession Using-Data

| Comments (2)

| Report a problem

Tags: Economics Keynes Recession Using-Data

| Comments (2)

| Report a problem

March 18, 2011

Student Finance: Bias at the BBC?

Writing about web page http://www.bbc.co.uk/news/education-12767850

According to a new report on the BBC website, headlined in last night's BBC TV and Radio news, "Graduates 'could pay back double their student loans."

It sounds scary. I can see another few hundred families around the country listening to the news and deciding university sounds just too expensive.

That would be a shame. There is a story here, but it is not the story on the surface. It is a deeper story, one of distortion and misrepresentation.

- First: There is nothing new in this "news."

Anyone who borrows will eventually repay more -- mechanically adding up the cash amounts, year after year -- than they borrowed. Interest charges ensure this result. Moreover, the longer is the period over which you borrow, the greater is the excess of cash repayments over the initial loan.

But why do borrowers pay interest? Because not having to wait is valuable. This has an important implication. A pound today is worth more than a pound next year or the year after. When you take out a loan, you've made the calculation that it's better to have the house or car now than wait for years in rented accommodation or sharing public transport while you save up. It's better to borrow and buy despite the fact that, having borrowed, you will have to repay more later.

By the same argument, the money you will have to repay next year should be considered worth less than the same money now. This is called discounting: we discount the future compared with the present.

Because future money has to be discounted to find what it is worth today, it is wrong to add up money in different periods without adjustment. Rather, the future values should be discounted, year by year, before they are added up.

Imagine the following scenario. In the BBC's story, the graduate has a debt of £43,000. In my scenario, you decide to borrow the same sum, but as a fixed rate mortgage, not a student loan. Suppose the lender's interest rate is 3 percent a year. Suppose you repay the debt in full, in equal annual instalments over 30 years.

On these assumptions, the sum of your undiscounted cash-out repayments will be a little over £67,000. But, if we revalue your payments in every year by discounting them back the present at 3 percent annually, the present value of the sum of your discounted repayments will fall to ... oh, £43,000.

The present value of the repayments is the same as the value of the loan!

- Second, therefore, there is no story. You repay -- in present value -- exactly what you borrowed.

But wait. That leaves a puzzle in the BBC account.

Remember that, in my example, you repaid everything at the market interest rate, and yet the undiscounted sum of your cash-out repayments was just £67,000, compared the £43,000 borrowed.

Compared with that, under the government's student finance proposals, graduates will enjoy three concessions. They'll repay nothing, and accrue no interest, while their salaries remain below £25,000. Between £25,000 and £41,000, they'll pay a reduced interest rate. And anything outstanding after 30 years is forgiven. Under those assumptions, surely, graduates should end up repaying less than you?

Yet, in the BBC version, graduates have to repay much more than you. The BBC puts the sum of undiscounted repayments at sums varying between £72,000 and £84,000, depending on the income of the graduate. It's the latter figure that lets them claim: "Graduates 'could pay back double their student loans."

What's going on?

The BBC commissioned "leading accountants," including the firm Baker Tilly, to support this story. It's based on a spreadsheet, available from the BBC website, "showing the calculations." The spreadsheet shows that the BBC's accountants sneaked in a hidden assumption, not reported in the story.

They built in 2 percent yearly inflation. In each year, they added 2 percent inflation to the repayment thresholds, 2 per cent inflation to the graduate's salary, and 2 percentage points to the interest paid.

What's wrong with that? Nothing -- except this: The 2 percent inflation assumption also pumps up the nominal undiscounted cash sums that their graduate repays every year. That was how they made the figures support that scary headline: "Graduates 'could pay back double their student loans."

Inflation is a further reason why it's wrong just to add up the column of annual cash repayments. Except in the first year, the annual payments are not in present-day prices. They are in different prices of different years, all of them higher than today's and some of them much higher. It's just plain wrong, and misleading, to lump them all together.

The BBC's calculation should have been done throughout in constant prices, so that the purchasing power of £1 would be the same in every year. But, if done at constant prices, there would have been less of a story. After proper discounting, there would have been no story at all. In fact, it would have emerged that:

- Most graduates will repay less, in present values and constant prices, than they borrow at the outset.

This brings us back to "the leading accountants." Given who they are, I guess they know their stuff. But do they? The mess behind this story leaves only two possibilities. They understood these issues perfectly well when they made their calculations -- or they didn't.

Either way, it looks bad for the accountants. Incompetent, or colluding with a misleading agenda? I'll leave it to you to decide on that.

It looks bad for the BBC, too. Remember, this is not the BBC reporting the news. It is the BBC inventing the news.

- Finally, a note for readers interested in open-source data.

The BBC website provides the spreadsheet with the figures, in their words, "showing the calculations." That's good.

The problem is that, before uploading the spreadsheet, they converted all the spreadsheet formulae to values. It is the formulae that enable to user to track the links from one number to another, and see at a glance how the calculations were made. The truth is that the spreadsheet does not show any calculations at all, only numbers. That's bad.

I can see no purpose in it, except to make checking more difficult.

Mark Harrison

18 Mar 2011 12:21

| ![]() Tags: Economics Universities Using-Data

| Comments (5)

| Report a problem

Tags: Economics Universities Using-Data

| Comments (5)

| Report a problem

March 25, 2009

Naomi Klein, Milton Friedman and Me

Writing about web page http://www.warwick.ac.uk/go/markharrison/comment/shockdoctrine.pdf

On February 24, 2009, by Naomi Klein was awarded the first Warwick International Prize for Writing, for her book The Shock Doctrine. On behalf of the panel of judges, the novelist China Miéville described The Shock Doctrine as "a brilliant, provocative, outstandingly written investigation into some of the great outrages of our time."

That got my attention. Here's why. On August 26, 2008, Kurt Jacobsen reported in The Guardian about opposition to plans to set up a Milton Friedman Institute at the University of Chicago. The report included some claims that I thought were wrong. So, I replied. Here's my letter, published on August 28:

Your feature on Chicago's proposal to establish a Milton Friedman Institute of economic research (Milton Friedman gives Chicago a headache, August 26) is misinformed in some important respects.

You state: "In postwar America, Friedman's market fundamentalism was regarded as lunatic-fringe stuff." This was never the case. I learned economics in Cambridge in the late 1960s. My professors followed Keynes and Marx, but they rightly made Friedman's work part of my undergraduate syllabus. Friedman's scholarship, not his opinions, made him one of the most influential economists of the 20th century.

You state that Friedman "worked for General Pinochet". While Friedman visited Chile, he did not work for the dictator. His advice was that Chile should turn back from state control of economic life; in the long run, he argued, free markets and political freedoms go hand in hand.

Finally, you give the impression that the mission of the proposed Friedman Institute is tendentious: "The design and evaluation of economic policy requires analyses that respect the incentives of individuals and the essential role of markets in allocating goods and services ... design of public policy without regard to market alternatives has adverse social consequences." While such a statement may be infinitely qualified, few economists today would dispute the principle.

I didn't expect to get away scot-free. On August 30, The Guardian published a letter from David Waddilove of Teignmouth, Devon:

Mark Harrison (Letters, August 28) is disingenuous about the relationship of Milton Friedman to Pinochet's Chile. Neither does he mention the havoc, bloodshed and mass starvation wrought on the people and economies of, among others, Uruguay, Argentina, Russia and Iraq by the Chicago School's symbiotic relationship with sundry dictators and their personal financial gain from those relationships. Nor, of course, does he mention the benefits to US corporate power wrought by the destruction of the public sector in each country the Chicago School meddles with. It is sad to see Warwick University, once the harbinger of some radical thought, now accommodating such "free" market orthodoxies without reference to their real-life testing grounds. Naomi Klein's The Shock Doctrine should be required reading for anyone interested in what actually happened.

I didn't think of replying, but I didn't like the tone. It seemed to be all guilt by association: Chicago-Pinochet. Chicago-Harrison. Harrison-Pinochet. Harrison-Warwick. Warwick-Pinochet. It looked like I must have blood on my hands. If that was the spirit of The Shock Doctrine, I wasn't sure I wanted to read it. Still, it stuck in my mind.

Months went passed. Then, the prize went to ... Naomi Klein for The Shock Doctrine. Not just any prize, but the first biennial Warwick Prize for Writing, a major literary award endowed by a great university, one that I love and have worked and lived for over thirty years.

Maybe I had missed something.

I got hold of the book and read it. It had a big, important message that I wrestled with. I asked my colleagues what they thought about it. It turned out none of them had read it. I think that is a mistake: the book has already had a significant influence on how people see economics and economists, David Waddilove of Teignmouth being one.

After some reflection, I wrote down what I think about the book in a paper called Credibility Crunch: A Comment on The Shock Doctrine. This is how it begins:

If you think that free markets haven’t worked that well recently, it is perhaps not surprising. If you think that free markets are spread only when business executives, politicians, soldiers, technocrats, and economists join to overwhelm popular resistance by force and violence, then you may have read it first in Naomi Klein’s The Shock Doctrine.

It concludes:

For the [Warwick Prize] panel, China Miéville described The Shock Doctrine as "a brilliant, provocative, outstandingly written investigation into some of the great outrages of our time." The Shock Doctrine merits this praise, but it does not merit belief.

If you are still interested, I hope you'll look at my paper and see the reasoning that fills the gap between my opening and my conclusion.

Mark Harrison

25 Mar 2009 09:12

| ![]() Tags: Globalization Naomi-Klein Politics Using-Data

| Comments (9)

| Report a problem

Tags: Globalization Naomi-Klein Politics Using-Data

| Comments (9)

| Report a problem

January 23, 2009

Gaza: A Lesson From History

Writing about web page http://www.publications.parliament.uk/pa/cm200809/cmhansrd/cm090115/debtext/90115-0013.htm

On January 15, Sir Gerald Kaufman, MP, told the House of Commons:

My parents came to Britain as refugees from Poland. Most of their families were subsequently murdered by the Nazis in the holocaust. My grandmother was ill in bed when the Nazis came to her home town of Staszow. A German soldier shot her dead in her bed.

My grandmother did not die to provide cover for Israeli soldiers murdering Palestinian grandmothers in Gaza. The current Israeli Government ruthlessly and cynically exploit the continuing guilt among gentiles over the slaughter of Jews in the holocaust as justification for their murder of Palestinians. The implication is that Jewish lives are precious, but the lives of Palestinians do not count.

On Sky News a few days ago, the spokeswoman for the Israeli army, Major Leibovich, was asked about the Israeli killing of, at that time, 800 Palestinians—the total is now 1,000. She replied instantly that "500 of them were militants.”

That was the reply of a Nazi. I suppose that the Jews fighting for their lives in the Warsaw ghetto could have been dismissed as militants.

Let's think about this.

The recent Israeli incursion into Gaza lasted 23 days (December 27, 2008, to January 11, 2009). Ten Israeli soldiers were reported killed in action.

The population of the Gaza Strip is currently in excess of 1.4 million. Estimates of the Palestinian death toll during the Israeli assault range from 1,330 (Hamas) to 500-600 (an anonymous Palestinian hospital doctor, reported by the Italian journalist Lorenzo Cremonesi). We can't verify either figure. For the sake of argument we'll take the higher figure; it suggests a death rate of around 1 per thousand of the population "at risk," about half of them unarmed civilians. (The lower figure would suggest less than 0.5 deaths per thousand with few unarmed civilian deaths among them.)

The Warsaw Ghetto uprising of 1943 lasted 120 days (January 18 to May 16, 1943). Sixteen German soldiers were reported killed in action.

The initial population of the Warsaw Ghetto is not known. Between 1939 and 1942, the German occupation concentrated between 300 and 400 thousand Jews in Warsaw. In addition to an unknown number of deaths from hunger and disease, between 250 and 300 thousand were deported to Treblinka and murdered over the summer of 1942. Jewish deaths during the uprising itself amounted to 13,000; after the insurgents' surrender, the 43,000 survivors were deported for extermination. The final death rate amongst the population "at risk" approached 100 percent.

On these figures, the fate of the Warsaw Ghetto in 1943 does not look like a close parallel for that of the Gaza Strip today.

That's enough about outcomes. What about intentions?

In Warsaw 55 years ago, the intentions of the two sides were clear. The Germans intended to exterminate the Jews regardless of age, sex, or combatant status; the ghetto uprising simply forced them to accelerate the process. The intention of the insurgents, who had a good idea of what had happened to those deported to Treblinka in 1942, was to resist otherwise certain death.

In Gaza this year, the intentions of each side are open to more than one interpretation. The Israelis said they intended to avoid civilian casualties as far as possible, but "as far as possible" is a difficult phrase. Certainly, civilians were killed, certainly in dozens, possibly in hundreds. Setting moral feeling aside, most of us (including me) have no practical idea of what words like "possible" or "necessary" mean in that context. But we can turn the question round. If the Israelis had intended to cause civilian casualties, was it within their military-technical capacity to do so on the scale of the Warsaw Ghetto? Without doubt, yes. If an army fighting in a crowded city with the military technology of the 1940s could kill tens of thousands of civilians in a few weeks, then surely it can be done again today; but that is not what happened, as we see.

As for the intentions of the Hamas militants, they were defending ... hmm. Not sure. The right to fire rockets freely across the border into Jewish settlements, I think.

To make sure you understand me, let me add: Crime deserves trial and punishment. If Israeli troops behaved badly in Gaza, what happened in Warsaw more than half a century ago does not justify it. (And exactly the same applies to those who organize indiscriminate suicide or rocket attacks against civilians.) Things that were done to us in the past do not remove anyone's moral responsibility for what we do in the present or plan for the future.

In fact, in solving conflict, history is generally not much use. It is part of the problem more often than of the solution. As Ed Glaeser has written, the memory of past crimes, real or imagined, fuels the fear of crimes yet to be committed, and so hatred, and encourages people to feel justified in committing more crimes themselves! Usually, nothing positive can be achieved unless all sides can learn to forget a whole lot of the past.

But history that is manipulated, or distorted, or misremembered, is worse than anything, because it adds the petrol of hatred to the fire of conflict. So, for as long as we have to have it, let's try to get the history right.

Mark Harrison

23 Jan 2009 14:57

| ![]() Tags: History Israel Palestine Using-Data

| Comments (0)

| Report a problem

Tags: History Israel Palestine Using-Data

| Comments (0)

| Report a problem

November 16, 2008

Child Protection: They're missing something, but what is it?

Writing about web page http://www.guardian.co.uk/society/2008/nov/15/baby-p-child-abuse

The Guardian’s front page, Saturday Nov. 15, reported “Eight in 10 seriously harmed children ‘missed’ by agencies. Government research reveals scale of gaps in child protection.” The reporter, Robert Booth, noted that our child protection register lists 29,200 children “known to be suffering harm”. But, of the “189 children whose death or serious injury prompted a local authority serious case review between 2005 and 2007,” no less than 156 were not on the register, according to an analysis of the most serious cases that ministers will receive in the New Year. Conclusion: “The research has raised concerns that, across the country, procedures that should result in children at risk being protected by the government’s flagship anti-child abuse system are not being followed, leading to deaths that could be avoided.”

Sounds bad for social workers, doesn’t it? And yes, it’s a possible conclusion. But it is not the only evaluation we could make. I’ll show that a completely different conclusion is also possible. The point is that, in order to evaluate social work intervention we have to look at what they did do, as well as what they didn’t do. And evaluating what they did do turns out to be surprisingly difficult, because it involves asking the question: “What would have happened in the absence of any social work intervention?”

The report states that, over the three years from 2005 to 2007, 33 of the 29,200 children registered as “known to be suffering harm” were killed or seriously injured—a rate of approximately 1 per 1,000. What would have happened to these children if social workers had not registered them and watched their welfare? There’s a clue: it lies in the 156 children killed or injured that were not registered. It is not completely clear what this means, however, in so far as we don’t appear to know the size of the total pool of children suffering harm that were never spotted in advance and so never registered.

Here are two possibilities.

- First, suppose the number at risk but unregistered was quite small, say, one tenth of those registered. In that case, the rate of death or injury among the unregistered children suffering harm must have been very high—156 divided by 2,920, or 54 per thousand. Apply this rate to all the children hypothetically suffering harm then, the 29,200 registered plus the 2,920 unregistered. That suggests, conditional on no social work intervention, more than 1,700 casualties. But in actual fact, there were “only” 189. On this scenario, by registering nearly all children at risk, our social workers reduced casualties by an order of magnitude; they deserve congratulations, not brickbats, for the successful protection of thousands of children.

- Alternatively, suppose the number at risk but unregistered was much larger, say, as many as the total number registered. In that case the rate of death or injury among the unregistered children at risk was much lower—156 divided by 29,200, or 5.4 per thousand. This time, applying 5.4 per thousand to all the 29,200×2 children hypothetically suffering harm, it appears that, without any social work intervention, there would have been some 315 casualties. In this scenario social work intervention would appear to be less effective. Social workers missed half the children at risk, and their efforts did not even halve the casualties. In their defence, however, a further point would then need to be made. This is that, with nearly 60,000 children suffering harm, and half of them undetected and entirely lacking the protection they need, abuse must be far more widespread in our country than has been assumed in resourcing our hard pressed family services. While there is less in this scenario for which social workers should be praised, the main lesson would be that society is in much worse shape than we thought, and criticism for not recognising this should be reserved for ministers and policy advisers.

Two possibilities; which is it? I’ve never worked in or on child protection (I’m just a parent). Like you, I rely on the experts to tell me. But if the experts don’t ask, we’ll stay in ignorance.

Mark Harrison

16 Nov 2008 11:48

| ![]() Tags: Social-Work Using-Data

| Comments (0)

| Report a problem

Tags: Social-Work Using-Data

| Comments (0)

| Report a problem

Loading…

Loading…