All 27 entries tagged Pensions;

No other Warwick Blogs use the tag Pensions; on entries | View entries tagged Pensions; at Technorati | There are no images tagged Pensions; on this blog

January 28, 2021

Pension scheme valuation versus pension funding and the cost of prudence (with reference to USS)

My argument in this latest draft of my paper on pensions valuation and funding (pensionsvaluation5.pdf) is relevant to all defined benefit schemes, of which there are still over 5300. It is aimed primarily at the regulator, who is faced with a siituaton of worsening deficits, and secondly at the actuarial profession. It is also directed at all who are involved in the valuation of the University Superannuation Scheme, whether executive, directors or the stakeholders UCU or UUK.

According to the latest Purple Book published by the Pension Protection Fund, total combine deficits of all DB pension schemes as at March 2020, have reached £90.7 billion last year compared with £12.7 billion the year before. This is before the effects of covid-19 have been felt and more and more schemes have to depend on the PPF.

The pensions crisis, that has been getting worse for a number of years, and has led to many schemes closing to new accrual, is exacerbated by a regulatory system requiring market price valuations, combined with very low gilt rates (due to government monetary policy/ quantitative easing) used to calculate liabilities. But this is not the only methodology that can be used: it is aimed at ensuring schemes with weak employer support have enough assets they can liquidate to pay the pensions should they have to close. But for an open scheme with a strong employer covenant it is very misleading and leads to cost increases that undermine it. For an open scheme it is better to make a direct analysis of funding needs comparing projected investment earnings with benefit outgo (something that actuaries did in the past).

Where there is a very large and significant difference between the se two methodologies is in the risk metric that determines the cost of prudence. The mark-to-market methodology must use a very much greater risk allowance - due to the much greater volatility of asset market prices as compared with investment earnings. This means that the regulatory system we are using artificially inflates the cost of prudence. It contains a serious bias that makes schemes appear much more expensive, and deficits much bigger, than would be the case if they were valued as open schemes.

This is a serious issue for the USS which has so far stuck religiously with the mark-to-market methodology despite it being an open scheme with a strong multi-employer covenant. Stakeholders should demand a re-appraisal using the traditional actuarial methodology before reaching any conclusions about the future of the scheme.

Dennis Leech

28 Jan 2021 02:35

|

Dennis Leech

28 Jan 2021 02:35

| ![]() Tags: Pensions; Uss

|

Tags: Pensions; Uss

|  Comments (0)

|

Comments (0)

|  Report a problem

Report a problem

Please wait - comments are loading

Please wait - comments are loading

December 17, 2018

USS Institutions Meeting very disappointing

Last week was the annual USS Institutions Meeting, an opportunity for employers to be updated about the state of the pension scheme.

I attended as an elected member-nominated rep on the Advisory Committee (part of the formal USS governance structure). Attendees were invited to submit a question. I was disappointed that mine was not addressed but instead a heavily edited version substituted - and even that was not fully answered. My question was addressed to the chief executive, Bill Galvin, but the substitute question was answered by the actuary.

At bottom the issue facing the USS and the focus of the dispute is intellectual: a matter of methodology. A pension scheme must have sufficient funding to cover its liabilities when they fail due to be paid. That is obvious but there are different ways of assessing a scheme's ability to fund its pension payments over the years. However the law only requires the trustees to report on one of them, the Statutory Funding Objective, which requires the assets must be at least equal to the actuarial valuation of the liabilities known as the technical provisions, otherwise there is a deficit that must be filled by a recovery plan.

The actuarial profession is not united that this method - valuation - is necessarily the right approach and that it may be problematic. Many actuaries instead advocate projecting the flow of income - from both contributions and investments - to see if it will cover the flow of future benefits. I wanted to cite an important reference critiquing the valuation method: the paper by Simon Carne, which shows that the projection method is perfectly rigorous.

I wanted to show that it makes perfect sense to use both methods to get a rounded view. And Bill Galvin had previously accepted the point when I had asked a similar question two years ago. But it was evident that the the USS executive and the board are committed to one and only one valuation.

Here is my question:

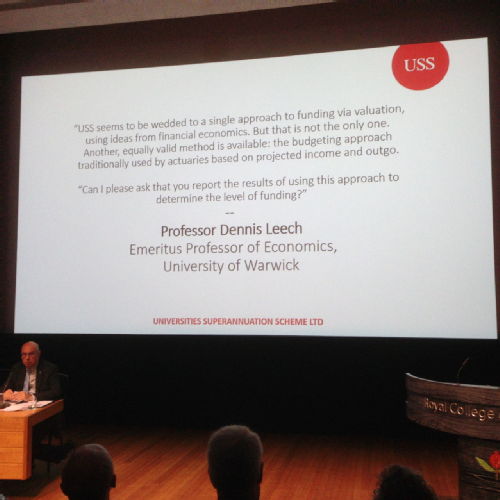

The USS seems to be wedded to a single approach to funding via valuation, using ideas from financial economics. But that is not the only one. Another, equally valid method is available: the budgeting approach traditionally used by actuaries based on projected income and outgo. Simon Carne, in his seminal paper “Being Actuarial with the Truth”, showed this method to be perfectly rigorous and most of the claims of financial economists against it to be false. For a scheme with a strong covenant like the USS it has the advantage of avoiding the use of volatile asset prices and problematic discount rates.

It answers the question: by how much is the pension fund in surplus or deficit on the premise that the existing investment strategy is maintained, with all future reinvestment following the current investment strategy? It would be useful for the USS to know the answer to that question, in addition to the valuation. This method - which does not depend on discount rates driven down by the artificialities of the government’s quantitative easing policy, nor the market risk introduced by excessive asset price volatility - has been advocated by First Actuarial and applied to many schemes, including USS, showing only small deficits or surpluses.

At this meeting two years ago I asked if you would use this approach as a supplement to the statutory valuation. Bill Galvin replied: “Triangulation of different approaches is very much part of our first principles approach, with the use of a number of different lenses rather than a single lens; then we are very open to that as well.”

Can I please ask that you report the results of using this approach to determine the level of funding?”

Here is the question that was put to the scheme actuary, who was easily able to dismiss the suggestion of an alternative approach. It did not seem from his answer that he had seen the original question.

This illustrates a great weakness of the current management of the USS: that it fails to engage with the intellectual arguments surrounding pensions. Since the USS is the pension scheme for universities, it might be expected that the trustees, most of whom are academics, would be keenly interested in the arguments about actuarial practice and financial economics that have been going on for over twenty years, in order to try to get a better understanding. But no, they seem to want to manage the scheme as if there is nothing to question about the methodology, and their job consists in little more than unthinkingly applying the rules designed essentially for small commercial companies. It is unfortunate that academics and others who are thinking about these crucial methodological questions are not being taken seriously by the management. It is hard to avoid the conclusion that the USS has become a scheme FOR universities rather than a true university scheme.

Dennis Leech

17 Dec 2018 21:52

| ![]() Tags: Pensions; Uss

| Comments (0)

| Report a problem

Tags: Pensions; Uss

| Comments (0)

| Report a problem

August 17, 2018

The USS analysis of reliance is seriously flawed and biased against the scheme

Evidence to the Joint Expert Panel

by

Dennis Leech, Emeritus Professor of Economics, University of Warwick, 15 August 2018

The assessment of reliance on the employers’ covenant is fundamental to the valuation and funding of the scheme. If the likelihood of the employers being asked to make additional payments above the maximum they can afford is too high, then that spells too much reliance and there will have to be benefit cuts. The details of their approach to this calculation are set out in various USS documents, including the Draft 2017 Actuarial Valuation, 1 September 2017, and Proposed approach to the methodology for the 2017 actuarial valuation: response to the Valuation Discussion Forum, 22 November 2016, and formalized in their various Tests.

The reliance measure is the difference between the scheme’s assets and what is termed the ‘self sufficiency’ liability. Self sufficiency is the level of assets that would be required for a low-risk investment strategy with a low probability of ever needing further contributions to provide benefits. The self sufficiency liability is described by USS as a ‘safe haven’ because it could be covered by investing in government bonds that are completely safe. Self sufficiency liability is calculated using a ‘gilts plus’ discount rate (gilts plus 0.5 or 0.75%) regardless of the actual investment strategy of the scheme. Because current gilt rates are so very low due to government monetary policy, this gives an extremely large figure of £82.4 billion for the liabilities. The conclusion reached by the USS from this is that the reliance is near the maximum that the employers can support.

There are however, serious problems with this approach to reliance. The methodology is flawed in two important ways.

- Essentially what is at issue is a choice between two statistical hypotheses that have far reaching consequences that are very different: on the one hand, the scheme remains open indefinitely, and on the other, there is a high likelihood of it having to close at some stage in the not-too-distant future. An even-handed treatment that tested the two hypotheses fairly would use the method of scientific testing of statistical hypotheses. This has not been done and instead the USS approach has, in effect, been biased in favour of supporting the second hypothesis.

- The treatment of risk by the USS is not consistent. In particular no allowance has been made for the fact that risk is not an absolute factor like it would be in a gambling situation, but is conditioned by circumstances. It is different for each of the two hypothesis under consideration. Two types of risk need to be considered: that which depends on the particular hypothesis being tested and that which is independent of it. We can call these respectively endogenous and exogenous risk.

Mistaken testing methodology

The USS tests of the reliance of the scheme on the covenant amount to essentially testing two hypotheses against one another using statistical reasoning. Either the scheme remains open indefinitely, and continues as it has been until now, or it eventually changes fundamentally and makes the journey to self sufficiency or closure. However, in their analysis, the USS have not treated both hypotheses in the same way, as a truly scientific approach would warrant. The hypothesis that the scheme remains open without undue reliance has not been thoroughly investigated and has been rejected nonetheless.

The scientific approach to testing a statistical hypothesis proceeds by first deriving the probability distribution of the relevant test statistic on the assumption that the hypothesis is true. The decision about whether to accept or reject the hypothesis is made by partitioning the theoretically possible values of the test statistic into two sets, the acceptance region and the rejection region. The test statistic is then computed and a decision made depending on where its value falls.

The test statistic in this application is the liability and the decision rule used is to compare the liability with the assets plus the amount of reliance that the institutions can afford. The affordable maximum reliance has been fixed at around 7 percent of payroll over 40 years.

The key point that the USS has ignored is that the liability depends on the particular hypothesis being assumed true and tested. If the scheme is regarded as continuing indefinitely then it can invest in high volatility assets to gain the higher returns that such assets will bring. High volatility is not a source of risk in this case. And if the scheme is cash positive, as the USS is and is forecast to continue to be indefinitely (see the paper by Salt and Benstead) it need not match the risk of the assets held with the liabilities. As Salt and Benstead put it:

“Being an open scheme brings significant investment advantages, which can be exploited to the benefit of the employers and members. The investment time horizon is infinitely long. An open scheme pays its benefits from contribution and asset income without any need to sell investments. If the asset income is sufficient, fluctuations of their market value is relatively unimportant.”(p8)

It follows that the liability for an open scheme will be appropriately calculated using a – higher - discount rate reflecting the expected return on the assets held in the investment portfolio. That will give a low figure for the liability.

On the other hand, if the scheme is seen as being in danger of closure, the volatility of the asset prices assumes central importance, and becomes risk. Under this ‘weak covenant’ hypothesis there is a danger that the scheme will have to sell off assets to pay benefits at some time in the future when prices are low and will be unable to pay the benefits in full. Therefore on this hypothesis the scheme needs to invest in – low volatility - assets that match the liabilities in terms of risk and return. The appropriate discount rate is therefore the - low – bond rate. The USS ‘self sufficiency’ portfolio is calculated on this basis.

The proper assessment of reliance therefore requires two different calculations of the liability: one assuming a strong covenant, that uses a liability based on best estimate returns from an income-seeking investment portfolio (such as the current one); and one for a weak covenant, that uses the self-sufficiency gilts-plus approach, assuming a low risk portfolio. Both calculations should be done. If they both give a reliance figure that is probably above 7 percent of salary, then the result is clear that the employers are unable to continue to support the scheme.[1]

It seems likely however that if the two approaches are applied correctly by the USS they will give different results. The assets on the valuation date of 31 March 2017 were £59.9 billion and the best-estimate liability figure was £51.7 billion, giving a surplus of £8.2 billion, and therefore no further reliance on the employers is indicated.[2] On the other hand, the self-sufficiency-gilts-plus liability was £82.6 billion, a reliance of £22.6 billion, larger than the target reliance of £10 billion.

The conclusion is that the result of the tests depends on what is assumed. On the hypothesis that the scheme remains open the inference is that it does not place particularly great reliance on the employers, and therefore we should accept the hypothesis and keep the scheme open. On the other hand, on the hypothesis that the scheme does not remain open indefinitely, there is likely to be high reliance on the employers.

Keeping the scheme open indefinitely would seem to be a perfectly reasonable and prudent course of action that would require neither increases in contributions nor cuts in benefits.

Inconsistent idea of risk

When valuing pension schemes it is important to separate the risks they face into two types: those that exist independently of the valuation, exogenous risks; and those which are consequent on it, what might be called endogenous risks.

A scheme in deficit is threatened by an existential risk due to the deficit itself, whatever other risks there may be. The need for the employer sponsor to make additional payments into the scheme threatens the company’s solvency and weakens the covenant. Many schemes have closed as a result of the actuarial valuation showing a deficit requiring deficit repair contributions over and above the employer’s regular contributions.

A scheme in surplus does not face that risk but is still subject to exogenous risks from other sources. A company, or association of employers such as the USS, can become insolvent for reasons unconnected with its pension scheme. For example large numbers of students might start deciding that a university degree is not worth the cost and refuse to incur the level of debt required leading to universities becoming insolvent.

The assessment of the reliance on employers should separate out these two types of risk and treat them fundamentally differently in the analysis. The exogenous risks can be allowed for by adjusting discount rates for prudence according to the usual actuarial principles.

However the endogenous risks require recognition of the simultaneity between the liability valuation and the covenant. If the covenant is strong the scheme can remain open and invest in high return assets and ignore the short term volatility in their prices. Therefore the risk of not being able to pay the benefits is low. But if the covenant is regarded as weak there is a non-negligible risk of not being able to pay the benefits.

The reliance calculation that has been done by the USS is deeply flawed because it ignores this endogeneity of the liability with respect to the strength of the covenant. It uses a liability value calculation based on a low-risk investment portfolio, with a low – gilts-plus - discount rate, appropriate to a situation of weak covenant. This leads to a greatly exaggerated idea of the scale of risk and therefore biases the analysis against finding that employers can afford the scheme - provided it remains open indefinitely. The USS is in effect assuming what it is setting out to test: by using the ‘safe haven’ valuation for the self-sufficiency liability it is assuming the existence of risk that is a consequence of an assumption of a weak covenant, and then claiming it shows there is too much reliance. It is circular reasoning.

The calculation by the USS is incoherent because it fails to recognize that the liability depends on the assumed strength of the covenant. The self-sufficiency-as-safe-haven definition is appropriate for an assumption of a weak covenant where prudence requires the lowest risk investment strategy. But if the covenant is assumed strong, so that short run market volatility does not pose a serious threat, the scheme can remain open to new joiners indefinitely and implement an investment strategy accordingly. It can invest in assets like equities that have high expected returns since their greater price volatility does not pose risk to its survival.

The analysis of reliance by the USS does not establish what is being claimed for it.

References

Salt, Hilary and Derek Benstead, Progressing the valuation of the USS, Report for UCU, First Actuarial, 8 August 2017

USS, Proposed approach to the methodology for the 2017 actuarial valuation: response to the Valuation Discussion Forum, 22 November 2016.

USS, Draft 2017 Actuarial Valuation, 1 September 2017.

[1] Strictly the two hypotheses are non-nested with respect to each other. Neither is a special case of the other. The result of the tests may be indeterminate in that both are accepted or both rejected.(See for example https://core.ac.uk/download/pdf/7092823.pdf)

[2] This figure includes no allowance for prudence as required. However it is hard to believe it would not still be very large after such allowance was made.

Dennis Leech

17 Aug 2018 09:51

| ![]() Tags: Expert Joint Panel Pensions; Uss;

| Comments (0)

| Report a problem

Tags: Expert Joint Panel Pensions; Uss;

| Comments (0)

| Report a problem

June 25, 2018

Pensions: A sustainable social contract

Pension schemes are often described disparagingly – without evidence – as being unsustainable or unfair between generations, or even according to some people, a kind of fraud, a form of Ponzi scheme. That is because they are fundamentally intergenerational, in that pensions require the working generation to supply goods and services to the retired. That is inescapable and therefore all pensions are essentially pay-as-you-go in this sense.

This paper pensionssocialcontract.pdfcalculates the investment returns required for pension schemes on various assumptions and finds that if they are properly designed they are perfectly sustainable given the typical investment returns that are currently achievable.

It is important to note that the rate of interest on government bonds, ‘gilts’ – which are presently very low due to government policy known as ‘quantitative easing’ and such – is not the same as the rate of return on investments. Investment returns on equities and property are determined in the market and not related to government-policy driven interest rates.

The USS chief executive Bill Galvin has recently issued yet another statement in which he argues the opposite. He says that the cost of future accrual in the scheme is as much as 37.4 percent of salary. It is hard to accept such a high figure without a proper explanation. It would be good to know what lies behind it.

Dennis Leech

25 Jun 2018 02:58

| ![]() Tags: Pensions; Uss

| Comments (0)

| Report a problem

Tags: Pensions; Uss

| Comments (0)

| Report a problem

April 30, 2018

The Joint Expert Panel will fail unless it is both radical and transparent

The agreement between the UUK and UCU provides that a “Joint Expert Panel, comprised of actuarial and academic experts nominated in equal numbers from both sides will be commissioned to deliver a report. Its task will be to agree key principles to underpin the future joint approach of UUK and UCU to the valuation of the USS fund.” If it is to achieve anything worthwhile it must carry out its task in a transparent manner.

The panel’s job will be to get at the truth against opposition from the vested interest of the USS executive who seem committed to a particular controversial view. The only way it can succeed in doing that is for it to proceed on the principles of free and open academic enquiry. Otherwise it will end up just rubber stamping what the USS is saying.

Let’s not forget that the scheme valuation according to the USS has not just been sprung on us. UUK and UCU, and their advisers and actuaries, have been discussing the draft valuation for months, if not years, since at least before the last valuation, for March 2014.

The UCU has been robustly challenging the methodology being followed by the USS, and many of its key assumptions. But it has been brushed off by Bill Galvin, the chief executive, and his executive team, without them seriously engaging with the arguments, while the Directors, in whose name they act, have remained silent, at least in public. It is to be hoped that some of them speak out against this one-sided approach, if only in board meetings.

If it is to do its job properly, the JEP needs to be radical, to address fundamental issues and ask basic questions. It is not enough just to hold a couple of meetings, listen to evidence behind closed doors and then issue its findings. It needs to transparently set out what its agenda will be in terms of “key principles to underpin the future joint approach of UUK and UCU to the valuation of the USS fund”. Only then, and if it openly publishes the detail of how it will do that, and is seen to subject the flawed USS approach to a radical re-appraisal backed up by evidence, will it satisfy members.

Issues for the JEP agenda

1. Accountability to members. The latest videos put out by the USS, featuring the CEO Bill Galvin, head of risk Guy Coughlan and scheme actuary Ali Tayyebi, fail to provide a satisfactory account of why changes are necessary and prompt questions about accountability. The Pension regulations state duties of a trustee in terms such as: “... ensure their pension scheme delivers good outcomes for members' retirement savings”; “Trustees must act in the best interests of the scheme’s beneficiaries”. It is arguable that the USS executive and trustees are falling short in their duty to the members.

2. Need to follow actuarial guidelines Actuarial guidelines say trustees “ ... must choose a method for calculating the scheme’s technical provisions, ie the value of benefits accrued to a particular date. You must take advice from the actuary on the differences between the methods and their impact on the scheme.”

The USS are not doing that because they are failing to properly consider different methods which give a different picture. This is not just of academic interest; there is a wide gap between what we are told by the USS executive and what makes sense to, for example, an intelligent person, whether a specialist such as an economist, statistician, or non-specialist, using a different method. They are doggedly working to a fixed blueprint and failing to consider alternatives which may benefit members.

The JEP should therefore insist that the USS executive be required to give a rounded view (ie taking into account analyses from different angles) of how the scheme is doing, and do so in simple language. They present only a single - relentlessly negative - view that clashes with the fact that the scheme is not in deficit in the ordinary sense of the word.

3. Need to explain the deficit. The overriding requirement is to require USS executive to explain how the present - apparently quite large - annual cash surplus of over a billion pounds per year turns into a deficit. Although this question has been asked many times by the UCU, so far no response has ever been forthcoming. Instead we just get a sort of financial hocuspocus. We need to know if there is really a deficit in a practical sense or it is merely a cconsequence of a particular theoretical approach lacking a sound empirical basis.

4. USS is a special case. The JEP should recognise that the USS is an extremely large scheme covering an important sector of the economy, one that provides vital public services. It is therefore unacceptable that it be managed solely according to a template intended for commercial company pension schemes. The scheme should be reviewed and valued in a manner that recognises the specific features of the pre-92 HE sector. It is not a typical company scheme and should not be compared with other DB schemes in a superficial or simplistic way (as the scheme actuary does in the video). Higher education should not be thought of as run in the same way as Woolworths.

5. Get power relations right. It is important that the JEP terms of reference have a proper regard to the power relations among the parties. The stakeholders are the UUK and UCU. The UUK institutions are the sponsors and therefore the senior partners. They ultimately call the shots. The USS board is accountable to the stakeholders, who appoint its members. They also employ the executive.

6. Role of the Pension Regulator. The regulator’s role, as a government body, is to ensure proper governance of pension schemes. It cannot and should not be taken as a substitute for the trustee and sponsor. The pensions regulation system is designed for (mostly small) schemes involving a single company in the market place. The university sector is quite different, and big and important enough not to be dominated by the regulator. Also it must be remembered that the pension regulations give trustees and sponsors wide discretion on many aspects of the valuation.

The rules as not as strict as we are often told and the regulator uses its enforcement powers only reluctantly.

7. Strength of covenant. The JEP should thoroughly and seriously examine the strength of the employer covenant, that is the ability and capacity of the 300 plus employers, including 68 pre-92 institutions, collectively to support the scheme. The scheme should be seen as one covering a whole large and important sector of the economy, which is more resilient than the mere financial solvency of the current members of the USS. The activities of teaching and research that are the business of the members are not related solely to the existence of particular institutions, and the need for them will continue after an insolvency, requiring the continued support of a pension scheme.

So it is wrong to look at covenant exclusively in terms of the solvency of individual institutions without considering the pre-92 sector as a whole.

8. Take a long-term view. Pensions are long-term commitments and funds ought to be invested on that basis. The valuation should also take a long-term view and ignore short-term fluctuations in asset prices. Short term market volatility is of minor, if any, relevance. Keeping the scheme open to new members is key. An open scheme with positive net cash flow can invest in assets that have a high expected return in the long run, such as equities. The efficient and rational running of the scheme suggests this.

9. The assessment of the covenant should beware circular reasoning. The discount rate used in the valuation reflects the strength of the covenant: where there is a weak covenant, prudence leads to a high liabilities figure based on a low-risk gilt rate being used as the discount rate. So it is circular to then use this liabilities figure in asking about the employers’ capacity to support the scheme, that is, whether the covenant is strong or weak. That is putting the cart before the horse: the assumption of a weak covenant leads to the conclusion that the covenant is weak.

Equally, basing the discount rate on an assumption of a strong covenant, giving the scheme freedom to invest in higher-return higher-risk assets for the long term, a higher discount rate and hence lower liabilities, might lead to the opposite conclusion. Assuming a strong covenant and valuing the liabiities on that basis might very well point to the employers being well able to afford to support the scheme indefinitely. The present covenant assessment method assumes the result it sets out to find and is not fit for purpose.

10. Further detailed questions. The JEP should require answers from the USS actuary and executive to questions of detail. It should not be satisfied with generalisations presented without evidence, which is their usual style.

Members should ask for further detailed information as follows:

(a) Analysis of the scheme in terms of cash flow projections for income and outgo. Preliminary studies based on partial information done by First Actuarial have suggested strongly that the scheme is long-term sustainable over a range of assumptions. More work needs to be done, building on this, using the actual data from USS.

(b) Question the excessive use of index linked gilts (which are currently producing a negative return). The idea that investing in government bonds - following actuarial habit from a time when such assets provided a steady and safe return - should be questioned in light of today’s very low interest rates that result from government policy. It is highly irrational to invest in a way that guarantees losing money - money that will have to be found from higher contributions. The notion that such an investment strategy is a ‘safe harbour’ (as Guy Coughlan puts it) needs to be subjected to detailed scrutiny. Is the scheme actuary just following the customary practice, not noticing that its rationale no longer exists?

(c) Why not use the internal rate of return? Every pension scheme has an implicit internal rate of return required for its investments for it to be sustainable. It would cast a lot of light on the scheme and answer fundamental questions around sustainability if these could be provided and compared with actual and expected rates of return.

(d) Are investment returns in fact too low? The USS executive claim that expected investment returns have fallen too low for ‘most asset classes’. It is certainly true of gilts. But is it also true of higher income assets such as equities? The JEP needs to examine this argument carefully, because, even if expected returns have fallen, that may make little difference to affordability in practice - if discount rates are based on investment returns not gilts - especially if the scheme is in surplus.

(e) Investigate in detail the ‘best estimate’ valuation. The USS valuation document reports a ‘best estimate’ surplus of £5.1bn. Their statement that ‘the best estimate surplus has only a 50:50 chance of success’ need to be examined since it seem to be lacking in precise meaning. This 50:50 argument comes from the fact that the liabilities estimate is an average (median) over the distributon of investment-portfolio-return-based discount rates, but that in itself does not seem to tell us about the likelihood of the surplus not being achieved.

(f) Focus on the income from the investments not their price. This is a major issue that seems to be almost universally ignored in pension valuations. The fact is that the stock market and bond markets are much more volatile than the income that drives them - whether dividends or interest - well known from the work of e.g. Shiller and others. This excess volatility greatly amplifies risk if assets are valued at market prices. A true economic analysis would allow for this but it is being ignored by the USS executive. In an open scheme like USS it is income from investments that are important to pay the pensions and their asset prices are of minor importance.

Valuing the scheme using asset market prices instead of investment earnings greatly amplifies risk. The JEP should commission an alternative valuation along these lines, with assets valued at discounted present value of expected future income.

(g) Question the facile assumption that equities are universally riskier than bonds. This assumption leads to statements being made with an undue degree of certainty and calculations done with spurious precision. Many equities provide good long-term investments without a lot of risk. Bond markets are also subject to short-term volatility like equity markets and there is excess volatility in both.

(h) Examine in detail projections of key parameters including mortality rates, salary growth, inflation, etc. Also the level of prudence.

Dennis Leech

30 Apr 2018 15:19

| ![]() Tags: Pensions; Uss;

| Comments (0)

| Report a problem

Tags: Pensions; Uss;

| Comments (0)

| Report a problem

March 21, 2018

Response to Urgent update from the USS trustees from member

The following response from a member was passed on to the UCU Pensions Officers discussion list by Sunil Banga

Dear USS,

Thank you for your “Urgent update from the USS trustees”, which I received on 17 March 2018, and which helped to dispel some of the rumour and disinformation that has circulated around the pensions issue. It is a great relief to learn that I am not expected to live to 147 years of age.

A number of other even more scurrilous and damaging pieces of misinformation have come to my attention, and I hope you can clear up these pieces of mischief before they inflict further damage on the reputation of USS and the higher education sector.

I have heard a vicious rumour circulated by the BBC’s education and family correspondent that the chief executive of USS, Bill Galvin, received an £82,000 pay rise this year, bringing his pay package up to £566,000 per year.[1] Only the most hardened cynic could believe this. It would, after all, mean that his pay rise alone is greater than the annual salary of many of those whose pensions the USS has proposed drastically to reduce.

What gives this rumour a particularly nasty edge is that after claiming that the running costs for the pension scheme are £125 million per year, including two staff members earning more than £1 million, the BBC correspondent quotes Mr Galvin as saying that the pension scheme is “excellent value”.

I think it would be a good idea to ask the BBC to publish a retraction, because this sort of rumour is likely to undermine the reputation not only of USS but of the higher education sector as a whole. I hope I will receive another urgent update on this matter as soon as possible.

An even more damaging piece of misinformation surrounds the results of the September 2017 survey of member institutions of USS. USS reported the survey found that 42% of employers wanted a lower level of risk.[2] This finding justified the “de-risking” exercise that increased the projected deficit in the pension fund and which ultimately gave rise to this unfortunate dispute. Could there be any greater mischief than the ugly rumour, originating with the Financial Times’s pension correspondent, that UUK “told the FT that Oxbridge colleges accounted for one third of the total wanting less risk” because Oxbridge colleges “are employers in their own right” and hence each college was counted as having an independent vote?[3] If a third of those wanting lower risk were Oxbridge colleges, this would mean that, beyond Oxford and Cambridge, the opinions of barely a quarter of the respondents to the survey justified the reduction in benefits that led to the strike.

Anyone gullible enough to believe that USS would accept this sort of gerrymandering must think that we still live in feudal times! I think it is important that USS nip this story in the bud. It is the sort of thing that might otherwise lead to the complete collapse of trust in both USS and UUK.

The thing that worries me, though: how did hackers manage to plant these stories with the BBC and the Financial Times correspondents? Could this be part of a concerted digital attack by a hostile foreign power?

As if that weren’t enough, the rumour-mongers must have hacked into Cambridge University’s response to the September 2017 survey, in which one finds the following justification for lowering the level of risk: “The University (and the other financially stronger institutions) continues to lend its balance sheet to the sector, which contains the cost of pension provision for all employers. In a competitive market for research and student places the University would be concerned if this appeared to be having an adverse effect on the University’s competitiveness (by allowing competitor universities access to investment financing or reducing their PPF costs in a way that would not be possible on a stand-alone basis).”[4]

No one could possibly believe that Cambridge University would be so selfish as to drive the whole education sector into turmoil in order to improve its relative position on the capital markets vis-à-vis other universities—or that the USS posture would collude with this sort of behaviour.

I hope you can see the urgency of correcting this bit of misinformation. The mystifying thing, though, is how someone has managed to plant the quoted statement in Cambridge’s response to the September 2017 survey, found on Cambridge’s own website. What evil force is trying to tarnish higher education in this way?

What USS must correct most urgently of all, though, is the following narrative: that in 1996, rather than build up a healthy surplus, USS permitted the employers to reduce their pension contributions from 18.55% to 14%, on the understanding that there would be no reduction in benefits; that the employers reduced their funding between 1997 and 2009, when hard times hit us all; and that when the fund was found to be in deficit, rather than ask the employers to pay a surcharge to compensate for their earlier reduction, USS instead instituted a series of reductions of benefits to the pension beneficiaries.

This story is the most damaging of all. Any child who has been immunised against profligacy by the fable of the grasshopper and the ant would recognise the impropriety in allowing the grasshopper employers to reduce their contributions in the apparently endless summer of 1997 to 2009, then requiring the employees (who, conscientious as we are, never reduced our contributions) to accept lower benefits in response to bad times. No responsible adult would let the employers get away with this, let alone an organisation like USS with fiduciary responsibilities. If we were to believe this story, we would have to believe that every time push came to shove, the independent chair of the Joint Negotiating Committee sided with the employers. That is not possible, because the very first words of the “urgent update” you just sent say that USS “has the primary duty to act in the best interests of the scheme’s beneficiaries”. No organisation would be so shameless as to allow itself to quote those words having permitted the employer to treat the beneficiaries in the way this mean-spirited story recounts.

I do hope that USS sees the urgency of dispelling the rumours that I have reported. If they continue to circulate, they will reinforce the belief that USS has acted as the servant of the most aggressive employers in the sector, who want to improve their balance sheet position even if that poisons relations between universities and their staff for a generation, destroys trust in USS and UUK, drives university employees into penury in their old age, tarnishes the reputation of the higher education sector, and thus does irremediable harm to the nation.

I look forward to your next urgent update containing apologies from all of those whose words and actions have brought USS and higher education into disgrace.

With my best wishes,

a USS beneficiary

[1] Sean Coughlan, BBC News education and family correspondent, “University Pension Boss’s £82,000 Pay Rise,” http://www.bbc.co.uk/news/education-43157711.

[2] “UUK Responds to USS’s Consultation on Funding Proposals”, https://www.uss.co.uk/how-uss-is-run/valuation/2017-valuation-updates/uuk-responds-to-usss-consultation-on-funding-proposals.

[3] https://twitter.com/JosephineCumbo/status/966205373349801985.

[4] Response to Question 3B, “University of Cambridge

Responses to Questions from the UUK Survey on the 2017 USS Valuation,” https://www.staff.admin.cam.ac.uk/general-news/uss-pension-valuation.

Dennis Leech

21 Mar 2018 13:28

| ![]() Tags: Pensions; Uss;

| Comments (0)

| Report a problem

Tags: Pensions; Uss;

| Comments (0)

| Report a problem

November 23, 2017

Is the USS really in crisis?

Threat to the defined benefit pension scheme

The employers have said that they want to close the USS defined benefit pension (DB) scheme to future accrual, which means that new members will not be allowed to join, and existing members will not be able to contribute any more into it than they have already built up. Future pensions contributions will all go into a defined contribution (DC) pension pot via the Investment Builder.

Defined benefit pensions are much cheaper and less risky

This is a very bad decision because DB pensions are much better than DC ones. They are a guarantee of a secure 'wage' in retirement for life, whereas a DC pension scheme works differently: it gives a single sum of money on retirement which you have to turn into an income. And pension freedom puts you in the position of having to take some very serious decisions about what to do with this pot of money that will affect the rest of your life. A lot can go wrong, especially as a result of poor financial advice, and you may have to live out your retirement with the consequences of one bad decision.

A DC pension is risky because how much your 'pot' is worth depends on the vagaries of the stock market. Academic research has shown that it costs between fifty percent more and double to provide a given secure income in retirement via a DC pension scheme than than DB.

Essentially, there is less risk in a DB pension because of the collective nature of the scheme. None of us knows when we will die, which is the biggest risk facing us if we are having to live off a DC 'pot': if we do our 'drawdown' sums wrong we might run out of money before we die, or leave unused retirement money as an unplanned legacy if we die earlier than planned. (It is actually rather far fetched to believe we can plan for our retirement in this way.) But actuarial life expectancy tables solve this problem in a DB scheme: the longevity risk is simply pooled.

Likewise it is much less costly to build up a DB than a DC pension because the investments are pooled in a large diversified portfolio, exploiting economies of scale and the law of averages which are not available to a DC fund.

A pension is a 'wage' in retirement for life. A DB scheme is designed to provide that while a DC pension does not. A DC scheme is really an employer-subsidised saving scheme. How you turn the savings you have built up into a pension is another matter that you have to decide and that is not easy or cheap.

The source of the problem facing USS

Contrary to what a lot of people think, the USS is not a government scheme backed by the taxpayer, like the teachers, civil service, health service and others. It is a private scheme run and regulated like a company scheme. It comes under the Pensions Regulator in the same way as, for example the schemes at BT, Royal Mail, British Steel, BHS, etc. Like all these it is 'funded' which means, in effect, that it must stand on its own feet, that its trustees must be able to show the regulator that it will have enough funds to pay the pensions members have been promised and expect every month after they have reitred.

The source of all the controversy about valuing the scheme is the interpretation of the phrase 'enough funds to pay the pensions'. Does that mean a capital sum or a flow of income? The difference has a big effect on how much risk there is.

The UUK have said the scheme must close because it is in deficit, the deficit is growing and that is unsustainable because it means the institutions will have to make ever larger recovery payments.

Let us examine the claims of the UUK. First, the scheme is not in deficit in the ordinarily meaning of the term. Second, there is no evidence that investment returns are too low for the scheme to be sustainable. Third, the scheme is sustainable as long as it remains open and continues into the future along with the universities it serves. Fourth, it is highly questionable that there is a deficit even in the narrow technical meaning in which the word is being used here.

Where is the deficit?

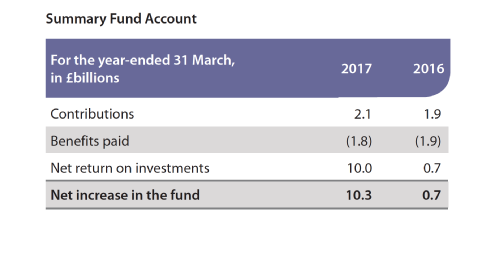

Figure 1 (below) taken from the USS Annual Report for 2017 shows the income from contributions and investments and payments of benefits. It shows that there is not actually a deficit in the usual meaning of the word. Income from contributions by employers and members totals £2 bn, while pensions in payment come to £1.8 bn. In addition it made a return on its investment portfolio of £10 bn (mostly this was from market price movements but that figure includes over £1 billion in dividends, interest, rent etc).

We usually think of a deficit in the George Osborne sense of not enough money coming in to pay the outgoings, necessitating selling assets or borrowing more. The USS is clearly not in deficit. It is cash rich and every year investing its surplus in new assets such as Thames Water, Heathrow Airport, and many other infrastructure projects in addition to traditional assets like company shares and bonds.

Figure 1: Deficit?

Will there be a deficit in the Future? Here we must enter the realm of intellectual speculation and deal with economic theorising, market fundamentalism and evidence-free opinion

Looking at one year's figures is not enough since they may not be typical and we need to look into the future. We need to find a way of seeing if there will be enough money to pay the pensions when they come due.

It is not obvious how that can be implemented. We have to do a thought experiment.

Consider a pension payment to a young lecturer early in his or her career, when he or she has retired, say in 50 years from now. There has to be enough funds to pay that. The pension can be forecast on assumptions about longevity, salary growth, inflation and other factors. But how can we tell if will be enough money? One approach is to ask how much will be needed to be invested today to give enough in 50 years to pay the expected pension.

Since the trustees have to be sure that the money will be there, they must be prudent in their assumptions. How prudent is prudent enough? Since nothing is ever certain, if they wish to be very prudent, they cannot rely on contributions from employers or members in the future. Theoretically the scheme could close (maybe all the member institutions go under for some reason we do not yet know) and there could be no contributions. So it is arguably best to err on the safe side and make this assumption.

And they have to decide how the money is invested to pay the pension in 50 years. Since nothing is certain in investments it would be imprudent to rely on risky assets like equities, even though they are almost certain to grow handsomely in a long enough period. Prudence - paradoxically - requires investing in secure bonds, which have a poor rate of return. At the moment the rate of return on government bonds is at a record low level due to the government's policy of quantitative easing.

If we do this calculation for all prospective pension payments, we get a figure for the liabilities. Comparing that with the value of the assets the scheme owns gives the funding level or deficit/surplus.

The liabilities figure is very large because it is based on the very powerful arithmetic of compound interest over long periods of time. It is also very sensitive to assumptions made - for the same reason. And it must ignore a host of real world factors that can change dramatically. The figure for the deficit is very inaccurate and volatile since it is the difference between two very large numbers, the liabilities and the assets, both of which are highly volatile.The deficit figure quoted by the UUK and USS executive has changed by over £2billion in little over two months. This fact alone suggests that this way of valuing the scheme is unreliable: the actual value of the benefits can not have changed in that time by more than a miniscule amount.

Another other problem with this approach, that has not been sufficiently discussed, is that it begs the question of how the capital value of the assets is to be converted into money to pay the pensions - that is, an income stream. That process needs to be spelled out and not just assumed. Can a scheme as big as the USS just sell assets on a large scale if need be without disturbing the market? It seems unlikely.

Are investment returns really too poor?

The UUK give one of the reasons for the deficit that investment returns have fallen. It is certainly true that gilt rates are at the lowest they have ever been, lower than inflation. It would not really be sensible for a rational investor to invest in gilts since that would guarantee losing money. But other investments, particularly equities, produce a good return that would seem to be enough for the pension scheme to continue to be viable, if it continued to invest in them.

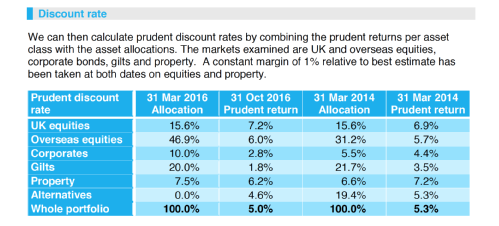

Figure 2 below shows the estimated returns on different investments that were prepared for the UCU by its actuary, First Actuarial. They contain a suitable margin for prudence to enable them to be the basis of a discount rate. The returns have fallen dramatically to low levels on bonds particularly government bonds.

Figure 2: Poor investment returns?

Is the USS unsustainable?

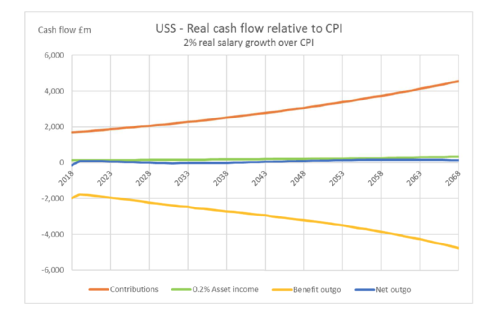

Another thought experiment is to ask if there is likely to be enough cash flow to pay the pensions, based on a projection of income from contributions and investment earnings and liabilities. This is a natural, direct approach that requires less in the way of assumptions than the capitalisation approach described before. In particular it does not require a discount rate for compound interest calculation.

Figure 3, below, shows projected cash flows for the USS that have been prepared for the UCU union by its actuaries (First Actuarial). This is just one of a number of scenarios that have been studied but all show the same picture (2% real salary growth, real asset income of 0.2 percent). It is clear that from this point of view, where the scheme remains open indefinitely, in the same way as is highly likely the pre-92 university sector will, the pension scheme will be perfectly sustainable, having a small deficit or surplus.

Figure 3: Unsustainable?

Is the scheme in technical deficit or is it in surplus?

There is a fundamental difference in the methodology between the situation where the scheme is assumed to be open indefinitely and where it is assumed to be getting prepared to close. In the latter case it must find a way of ensuring it is funded at all times, or at least as soon as possible while it can rely on the employer being able to support it. Volatility of the technical 'deficit' due to market fluctuations in asset prices represents risk here. The risk is that the scheme will close and the valuation will crystallise with assets values low due to a depressed market, such that they are inadequate to pay the liabilities. Hence the need for recovery payments to meet the cost of covering this risk.

On the other hand, if the scheme is open indefinitely with a strong covenant, it can be assumed it will never need to close. Therefore asset price volatility is not important. The ability of the scheme to pay benefits depends on there being sufficient investment and contribution income coming in. Therefore market volatility is not a source of risk. There is much less risk and therefore the scheme is cheaper because there is no need to cover it. Also the scheme does not need to invest in 'safe' assets like gilts for the same reason. An open scheme can, and should rationally, invest in assets that bring the highest return.

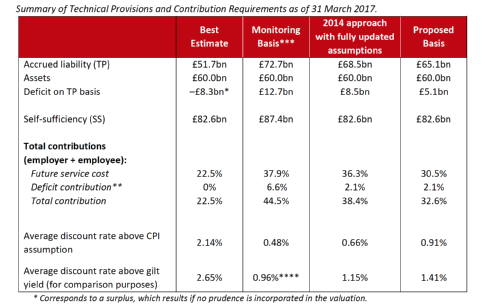

Figue 4 below (from the Technical Provisions Consultation document, September 2017) is the analysis, by the USS executive (not the UCU actuary this time, but the USS exectutive itself under its requirement to provide a fair view of the scheme), of the 'deficit' based on these two different assumptions. On the assumption that the scheme may have to close and therefore must be extremely prudent, so called 'gilts plus', which is the proposed basis, the 'deficit' is £5.1bn. (This has been changed since the TP document was published and is now £7.1 bn. The fact that these figures are so very volatile, with pension liabilities which change very slowly over decades being valued at amounts varying from month to month by billions calls into question the whole methodology.) On the other hand, if the scheme remains open, there is no need to apply a great layer of prudence to all the calculations, and the valuation of the liabilities can be done using the 'best estimate' of the investment returns as the discount rate. On this basis the scheme is massively in surplus, to the tune of £8.3bn!

Figure 4: 'Deficit' or 'Surplus'?

All the efforts of the scheme trustees, the employers and the Pensions Regulator should be devoted to ensuring the scheme remains open. The biggest risk comes from the deficit recovery payments calculated on the basis that the scheme might close. It is therefore a self-fulfilling prophecy. If the scheme is assumed to be ongoing and open then there is little risk.

Risk is not an absolute exogenous quantum as some suggest. It is contextual. And assumptions about it are self fulfilling. The problem with the methodology that is being used is that it is based on an assumption that risk is the same in all circumstances. That is a theory which is false empirically.

Why can't the Pension Protection Fund help?

What is puzzling is that the methodology takes no account of the safety net provided to all pension schemes by the Pension Protection Fund. The USS contributes its share of the levy to this government scheme which guarantees pensions in payment and ensures active members will receive pensions at 90 percent of the DB scheme level.

Why does the USS valuation ignore this? It seems directly relevant since it manifestly limits the risk.

It is said that if the USS entered the PPF it would be too big for it. But the PPF would take on the assets as well as the liabilities. Since the PPF is a government body there can be no problem of it failing to support the schemes in its portfolio, as there is with a private sector employer with a weak covenant. There is no problem with short term market volatility posing a risk.

Therefore we can argue that because the USS is protected by the PPF, a statutory body supported by government, the greatest part of its risk is removed. The valuation should therefore be done without such a large amount of prudence, and therefore the deficit will be much smaller or non-existent. Therefore the scheme is not in danger of failing and of having to enter the PPF.

Can anybody explain why this argument is not being used?

Dennis Leech

23 Nov 2017 02:06

| ![]() Tags: Pensions; Uss

| Comments (0)

| Report a problem

Tags: Pensions; Uss

| Comments (0)

| Report a problem

September 15, 2017

USS in Crisis? What is really going on? A message for all USS members.

This is the message sent to members of the USS from the UCU today.

USS in crisis? What’s really going on?

Academic staff in universities within the USS pension scheme have seen their pay fall in real terms since 2009, the cumulative loss to pay (compared to rises in RPI) is over 16%.

There are 53,237 academic staff at Pre 92 universities on fixed term contracts, many of them attempting to build a career.

In this context, the USS pension scheme is a vital and valued benefit for these staff, to some extent offsetting the pressure on pay and careers for these hard-pressed staff.

Since 2011, after 35 years of being a stable pension scheme, USS has been affected by great instability and turbulence.

Successive valuations in 2011 and 2014 have produced notional deficits that have been used to justify cuts to members’ pension benefits, with the closure of final salary pensions to new members in 2011 and then in 2014 the complete closure of final salary, together with the introduction of inferior Defined Contribution benefits for staff currently paid above £55,500.

In both cases, industrial action taken by UCU members staved off the introduction of significantly worse packages.

On 31st March 2017, the latest valuation of the USS scheme produced a notional deficit of £5 billion and the Trustee Board of the scheme indicated that to cover this, the cost of pensions need to be raised by 6 to 7%.

UCU is deeply concerned that if further cuts to pension benefits are proposed it will inject real long term risk into the USS scheme by making it increasingly less attractive to staff.

This is a real threat. USS faces the risk that it will become a decisively inferior package to the Teachers’ Pension Scheme, which staff in new ‘post-92 universities’ pay into. For example, a researcher joining USS at 38 with a 30 year career will receive more than £200,000 less in the USS scheme than they would in TPS over an average retirement.

The scheme is fundamentally sound

UCU argue that the USS scheme is fundamentally sound. Cash flows are positive. The sector is not likely to implode, the employer covenant is robust and the contributions from active members broadly cover pensions in payment. The scheme has £60 billion in assets to back up this situation. It is a ‘last man standing’ scheme where employers share the risk.

However, the way in which USS values the scheme is creating the appearance of a crisis which, the solution to which, ironically, threatens to generate a real long-term problem.

Since 2011, UCU has consistently argued that the USS ‘deficit’ is based on a flawed actuarial model. This model is creating an appearance of a scheme in crisis that then means it invests in more and more ‘safe assets’ which leads to lower returns then it is more expensive in effect a vicious circle.

Creating the appearance of crisis

The USS Board has opted for a valuation methodology based on a set of assumptions that UCU argue undervalues the robustness and unique nature of the USS scheme, which is one of the largest private sector schemes in the UK.

Most fundamentally, the Board has chosen to interpret the Pensions Regulator’s call for ‘prudence’ with unnecessary strictness by insisting on discounting the scheme’s liabilities using a complex measure termed Test 1 which is expressed in terms of the rate of return on government bonds rather than the rate of return on the scheme’s actual mix of assets.

As many commentators and pension experts have noted, this insistence on tying valuations to historically low gilts yields is creating artificially inflated deficits in many defined benefit pension schemes.

UUK is consulting the employers on the draft technical provisions which if accepted would lead to a watering down of benefits for scheme members. UCU argue that more confidence in the sector from employer and its ability to grow and support a decent pension scheme for staff would not only be important in retention but be valuable in recruiting world class academics.

UCU has commissioned its own actuarial analysis from First Actuarial, based on a different methodology, ‘Best Estimate minus’. ‘Best Estimate’ assumes that schemes will continue to pay out benefits as they fall due and make an actuarial best estimate of the future returns they will make on their actual investments, the minus is the introduction of prudence. We believe this methodology better reflects the reality of the sound fundamentals in the USS scheme and the UK higher education sector. Using this produces a surplus rather than a deficit in the scheme and obviates the need for the flawed ‘Technical Provisions’ being proposed.

At the very least, the fact that this is possible demonstrates the wildly different situations that can be generated by small changes in the assumptions being made by the Board.

Given what is at stake, we believe this makes it incumbent on the Board to reconsider this alternative approach in its valuation assumptions.

Summary

The approach being taken by the USS Board may be supported by the Pensions Regulator but the facts remain that:

- their approach has been criticised by significant pensions experts who recognise that it is creating artificial deficits by linking asset values to historically low gilt yields;

- their assumptions are based on a harsh, some might say ‘fantasy’ interpretation of prudence that does not reflect the real performance of actual USS assets;

- the vision of ‘prudence’ is founded on a vision of the UK higher education sector suddenly shutting up shop overnight and winding itself up;

As a result of this, UK higher education employers who have cut staff pay consistently for years have taken fright and indicated they will not raise their contributions any further, leaving hard-pressed academic staff, vast numbers of whom are struggling to build careers on insecure contracts, to pay more or work longer to get a decent pension.

USS shows no sign of deviating from its chosen course and University employers show no sign of willingness to take on extra risk to cover the requirement for increased contributions that will inevitably follow.

Such a situation is highly likely to lead to significant industrial action in the UK higher education sector.

Dennis Leech

15 Sep 2017 22:37

| ![]() Tags: Pensions; Uss

| Comments (0)

| Report a problem

Tags: Pensions; Uss

| Comments (0)

| Report a problem

May 26, 2017

The market–based regulation of pensions is a source of risk and deficits

My evidence to the DWP Green Paper consultation on Defined Benefit pensions

May 14, 2017

The ongoing crisis in occupational pensions, that is a result of the closure of many

company superannuation schemes, and their replacement with inferior alternatives, is a

ticking time bomb for society. Millions of workers will, in years to come, face a choice

between retirement with inadequate income and continuing to work into old age.

However it is not clear that there is anything fundamentally wrong with defined benefit pension schemes. A common complaint that one sometimes hears from experienced trustees and finance managers is that a pension scheme that appeared ostensibly to have been in good shape was closed on actuarial advice, after having been shown to be in technical deficit.

I wish to argue in this paper that a major contributor to such deficits are biases inherent in the approach and methods used by actuaries and accountants, based on recent developments in finance theory that are not empirically well founded. The regulatory rules themselves - that are supposed to protect agaist bad outcomes - are actually leading to those very outcomes.

To read more, download the paper here

Dennis Leech

26 May 2017 13:04

| ![]() Tags: Pensions;

| Comments (0)

| Report a problem

Tags: Pensions;

| Comments (0)

| Report a problem

September 05, 2016

Financial Times article arguing that pension scheme response to deficits makes the problem worse

An article in today's Financial Times argues that the conventional approach to pension scheme deficits by "de-risking" and "liability-driven investing" makes the problem worse.

cure_for_uk_pension_funds_deficits_inflicts_more_pain_ftcom.pdf

It makes the same arguments I made in my last blog. See:

http://blogs.warwick.ac.uk/dennisleech/

What the article is saying is directly relevant to the universities scheme, the USS, because it is committing the same mistakes it describes, in common with very many of the 6000 other private sector (because - surprisingly - the universities' scheme is a private sector scheme) schemes.

Dennis Leech

05 Sep 2016 01:01

| ![]() Tags: Pensions; Uss

| Comments (0)

| Report a problem

Tags: Pensions; Uss

| Comments (0)

| Report a problem

Loading…

Loading…