Comments on the USS valuation

There is a lot more involved in the USS dispute than what the level of gilt rates is on 31 March. Actually focusing on itgets in the way of understanding the true situation which is much more nuanced.

The idea that the market interest rate on government bonds - that fluctuates daily, with stock market movements - somehow matters to the pensions members will draw in two, three, four decades time is akin to a belief in magic.

The valuation (that compares assets and liabilities on a given date) is not the pension. It is not ‘counting the beans’ as many people seem to think. It is not an objective procedure. It is contextual.

The valuation is a statutory solvency check designed for those schemes that need to sell assets to pay pensions, usually company schemes closed to new members. USS is not one of those. It does not need to sell assets. So the context for USS is different; for it the valuation is really little more than a formality to comply with the rules.

The context of the valuation (and the regulatory code generally) is one that premises ultimate closure which results in higher perception of risk and greater cost of prudence. A scheme like USS, open with a strong employer covenant and a stream of new joiners, is in a very different situation as regards prudent funding and investment opportunities. That should lead our thinking.

The true funding situation is actually much better. It is not only that the extremely low interest rates of the past twelve years of QE are now back at a more normal level which has sent many pension schemes into surplus.

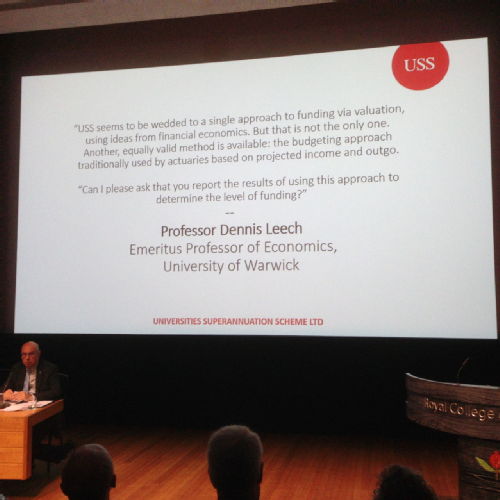

We should not be satisfied with that. There is a lot more that we should be demanding. We should STILL be challenging the valuation methodology.

The news about the USS is undeniably good. UUK have agreed to reinstate benefits in principle and USS have confirmed that should be possible given the surplus. But there are not just two parties involved in the dispute. Besides UUK and UCU there is the USS who manage the investments and do the valuation sums according to their own beliefs. And behind them there is the government in the shape of the DWP and Pensions Regulator who set the rules for DB pensions.

So it is possible UUK negotiators may not be able to deliver on everything they want (even if they speak for all their institutional members). Our main concern should be the context in which USS invests and does the valuation which to date has been a widely held conviction among actuaries, regulators, accountants, consultants, scheme investors that assumes the ultimate closure of DB schemes. So there is still a battle of ideas to be fought both with the USS executive and also with the DWP/Regulator.

What is really encouraging however is not only the joint letter from UUK/UCU/USS to the Regulator but also the USS response to the Regulator’s latest consultation on the Draft Code in which they make it absolutely clear that the scheme should be allowed to be runon the basis that it will remain open for decades to come. Supporting this means widening campaigning for university pensions to the parliamentary sphere, enlisting support from MPs and peers for the principle of keeping Defined Benefits pensions open.

There is also a need to keep up the pressure on the USS executive to change the assumptions that determine how they see risk in the valuation. At present liabilities are inflated enormously because market risk is (incorrectly) modelled in terms of stock market volatility,giving rise to the need to build in excessive prudence to hedge it, hugely bloating the liabilities figure. Capital exhaustion simulations are far too pessimistic. There is also the little matter of LDI. And many assumptions that go into the valuation assume closure (for example the key concept of self sufficiency). So there is need for a culture change in the USS executive.

But if the scheme is seen as open indefinitely, with a strong employer covenant, it does not need to worry unduly about asset price excess volatility. Risk it needs to worry about is in the future cash flows from contributions and investment receipts that fund the pensions. So the cost of prudence is far lower.

We are winning the argument. But it would be premature to think it is won.

Dennis Leech

03 Apr 2023 11:38

|

Dennis Leech

03 Apr 2023 11:38

|  Comments (0)

|

Comments (0)

|  Report a problem

Report a problem

Please wait - comments are loading

Please wait - comments are loading

Loading…

Loading…