All 31 entries tagged Economics

View all 245 entries tagged Economics on Warwick Blogs | View entries tagged Economics at Technorati | There are no images tagged Economics on this blog

August 08, 2011

Reform of the West: Lessons from the East

Writing about web page http://keithhennessey.com/2011/07/30/risk-and-the-governments-credit-rating/

Twenty years ago, the idea of post-communist "transition" looked straightforward. There were 30 or so economies that qualified as "transitional." The starting point (communism) and the end point (a democratic market economy) would be roughly the same for all of them, with a short one-way street in between.

Looking back, what impresses is the astonishing variety of routes out of communism, more and less marketized and more and less democratic. Compare Poland with Russia, China, Belarus, and Uzbekistan, for example. Explaining that diversity is a vast and worthy undertaking.

I'm reading Timothy Frye's new book, Building States and Markets after Communism: The Perils of Polarized Democracy (Cambridge University Press, 2010). Using lots of quantitative and narrative data from the former Soviet bloc, Frye argues that post-communist reforms were faster and more consistent, with more social transfers, when the political system was democratic. He shows, however, that the benign influence of democracy was conditional on low political and socio-economic polarization. Polarized democracies pursued reforms at a slower pace, with less perseverance and more wavering, and less generous assistance for the losers. The outcomes of polarized democracy were scarcely better than those of autocracy.

Polarized democracy: What Western country does that remind you of? America springs to mind. Growing socioeconomic inequality and increasing Red-Blue polarization have made America's problems increasingly intractable. America's public finances demand reform, but reform has been delayed and inconsistent. The debt-ceiling process was just a high-profile symptom.

Before Europeans start thumbing their noses at America, remember that the reform gridlock in the European Union looks as insoluble, or worse. Europe is polarized between debtors and creditors. And, for the purposes of the only reform that looks able to solve this polarization, a fiscal union, Europe lacks democratic government at the centre.

It turns out that reform of the West could be informed by the experience of reform in the East.

An afterthought: Let me belatedly advertise the most insightful comment that I've read on America's fiscal stalemate, Risk and the government's credit rating, by my Hoover colleague Keith Hennessy, published online just before the decisive vote in the House of Representatives. He argues that American leaders were balancing liquidity risk, solvency risk, and political risks (to themselves). Did they get it right? Read and find out.

Mark Harrison

08 Aug 2011 19:03

|

Mark Harrison

08 Aug 2011 19:03

| ![]() Tags: Economics Politics

|

Tags: Economics Politics

|  Comments (0)

|

Comments (0)

|  Report a problem

Report a problem

Please wait - comments are loading

Please wait - comments are loading

July 15, 2011

Pakistan: Is the War Contractible?

Writing about web page http://www.ft.com/cms/s/0/3574b5ee-ab15-11e0-b4d8-00144feabdc0.html

Relations between the United States and Pakistan have been going downhill since the killing of Osama bin Laden. Ex ante, it seemed likely that the Pakistan Army had offered some degree of shelter to the world's most wanted terrorist. Ex post, Pakistan has halted U.S. access to a drone base on the Afghan border; cut back on visas for U.S. training missions; and detained a doctor said to have helped U.S. intelligence identify bin Laden's family. In retaliation, the United States is now threatening to withhold $800 million in military aid.

The Pakistan response to this threat throws further light on the status of Pakistan as a U.S. ally in the war against Al-Qaeda and the Taliban. On July 10, 2011, the Financial Times reported:

Lieutenant General (retired) Moinuddin Haider, a former Pakistani interior minister, said that the halt on US aid would further strain the two countries’ relationship and called on the US to reconsider. “This move will only add to the anti-Americanism in our country,” he said.

The following day, Reuters reported:

Politically, [the suspension of aid] would be damaging to the relationship, said Pakistan's former ambassador to the United States, retired Major-General Mehmood Durrani said, reflecting a widespread view in Pakistan that it was fighting America's war, for which Washington must reimburse it.

So: Is Pakistan an ally or an enemy? Neither, it seems. There is anti-Americanism, but Pakistan is not an enemy. For Pakistan does make available services and facilities to combat AQ and the Taliban. But Pakistan is not an ally, either.

Nearly 50 years ago, Mancur Olson and Richard Zeckhauser worked out the basic theory of burden sharing in alliances. Consider two countries -- call them A and P -- that face a common enemy. A and P can fight together or separately. By fighting together, they can share the synergies from each other's efforts. For this reason, an alliance is vulnerable to free-riding: the more A contributes, the less P needs to put in. This turned out to explain quite well the pattern of burden sharing in NATO under the doctrine of massive retaliation.

The same theory leads to a straightforward prediction about what will happen if A suspends assistance to P for some reason. On its own, denied the help of A, P will put more resources into the struggle.

But what Pakistanis are saying does not fit this model. What they are saying is that, denied the help of America, Pakistan will fight less, not more. It is "America's war."

If neither an ally nor an enemy, what is Pakistan? Pakistan is a contractor. There is a contract between America and Pakistan, so that America mostly pays and Pakistan mostly fights or helps America fight. Pakistan will help resist AQ and the Taliban if America pays, and not otherwise. It is the same as a contract between me and a builder: I pay, so the builder builds, and not otherwise. There is no intrinsic common interest that we share. Incentives are aligned by agreed payments, not by anything else.

The work that my builder does, however, is contractible. That means we can write a contract that spells out the obligations of both sides with reasonable completeness, and includes most reasonably foreseeable contingencies. He works to my wife's satisfaction, I pay, and we part amicably. Otherwise, we may end up in court.

The war on AQ and the Taliban may not be contractible in the same sense. There are three reasons.

- First, there is asymmetric information. It's hard to tell whether the Pakistan Army is doing a good job, because it is hard for the Americans to monitor progress in harsh terrain among often hostile communities. As a result, America cannot know whether Pakistan is fulfilling its part of the bargain.

- Second, there is moral hazard. The Pakistan Army can explain almost any setback by "We didn't know" (that bin Laden was living under our noses) or "They got away." As a result, Pakistan has a strong incentive not to try very hard.

- Third, the Pakistan Army has residual ownership rights in the literal sense that it owns much of the Pakistani economy and is much more of a sovereign government than the nominal civilian government in Islamabad. As a result, when contingencies arise that are not in the contract, it can control its response in ways that do not formally breach its understanding with the United States over Afghanistan, yet are not ones that the United States would choose. For example, it can secure nominal improvement on the North West frontier by diverting Islamists into Kashmir or on to Mumbai.

A standard solution when a venture is non-contractible is vertical integration. In this case it would require the United States to take on the responsibilities of a colonial power. Ruling this option out on grounds that probably don't need spelling out, we are left with an interesting problem and no obvious solution.

Mark Harrison

15 Jul 2011 21:24

| ![]() Tags: Economics Pakistan Politics

| Comments (0)

| Report a problem

Tags: Economics Pakistan Politics

| Comments (0)

| Report a problem

June 24, 2011

Russia's Crisis, Greece's Tragedy

Writing about web page http://www.ft.com/cms/s/0/4dfcca24-9e46-11e0-8e61-00144feabdc0.html

On the plane back from Moscow, I read Martin Gilman's No Precedent, No Plan: Inside Russia's 1998 Default (MIT Press, 2010). Gilman was the IMF's man on the spot during the Russian debt crisis of August 1998.

I flew into Moscow a few days after that crisis broke. Business life seemed to be paralysed. Many people that I met were panicked or in despair. But in retrospect, Gilman points out, this was the start of Russia's sustained recovery from the economic collapse that accompanied the breakup of the Soviet Union.

The crisis itself was very ugly. The disarray in Russia's public finances had built up over years, with persistent overspending, repeated failures to generate taxes, and the high inflation and high interest rates that resulted. In the private sector, Russian banks borrowed in dollars at low interest rates and bought up high-interest ruble bonds. In the crisis, the exchange rate plunged by a third, resulting in widespread bank insolvencies.

Gilman recounts the fear that Russia would turn away from a market economy and economic integration to ultra-nationalism and autarkic controls. In fact, there was no tragedy. At a lower exchange rate, the Russian economy regained international competitiveness and embarked on a decade of rapid growth that just about doubled real incomes.

As I read the story of Russia's crisis thirteen years ago, I was caught up in the parallels with Greece today. There are very important differences, of course. Greece is much smaller, with 11 million people to Russia's 140 million. Greeks are far richer on average, with $16,000 per head (at 1990 prices) compared with $5,000 per head for Russians in 1994. (And Greece doesn't have huge armed forces armed with nuclear weapons.) Surely, Greece's problems today should be more manageable than Russia's then.

In fact, Greece's crisis is similar to Russia's -- at best. When you add up all the political and financial claims on the economy, they exceed the resources available by an unsustainable margin. In Greece, people expected the public sector to guarantee jobs. They expected free services and benefits. They expected to retire early on fat pensions. They expected all this without paying taxes. The result was a growing debt, which had to be serviced. The government expected to be able to service the debt by borrowing more, so debt rose more rapidly. This was fine as long as interest rates were low, and as long as they could get away with misreporting what they were up to.

Now the only solution is to cut back on some or all claims on the economy. But whose, specifically? If Greece is not to default on the public debt at some point, there must be a huge fiscal adjustment. Back in February, the Financial Times put the tightening at somewhere between 8 and 22 percent of GDP -- and that was just to stabilize the debt, not reduce it. Greek living standards must fall by an unrealistically large amount. in fact, as Mervyn King reiterated today, Greece is insolvent. Default would at least allow Greece to transfer some pain to bondholders -- but domestic reform and retrenchment are still necessary, because who will lend to a defaulting government to cover its deficit?

In Greece now, as in Russia then, pain is inevitable but there is no prospect of agreement on how the pain should be distributed. Every group in the population -- the rich, the poor, the farmers, the business sector, the bankers, the public employees, the students, the pensioners -- looks for a way to pass the parcel onto others. The government does not have the authority to stop the game.

Moreover, much Greek debt is held abroad, so European bondholders, many of them French and German bankers, and increasingly the European Central Bank, are in the game too. The French and Germans are playing pass the parcel with the ECB; the British certainly don't want the parcel; as fast as the others pass it back to Greece, the Greeks hand it over again.

It is in everybody's interest to solve the Greek crisis quickly, but it is in nobody's interest to accept the role of victim. This must go on as long as at least one special interest inside or outside the country expects to gain by blocking a solution. Resistance will stop only when things are so bad that no one can any longer hope to derive a one-sided benefit from further delay.

In another respect, Greece's problem is worse than Russia's. The Russians could devalue. Devaluation of the ruble restored competitiveness and also cut incomes -- everyone's incomes -- by pushing up import prices. This put an end to argument over who should suffer the pain. Moreover, the pain was short-lived because recovery followed. Greece cannot copy this while it remains in the Euro zone. In fact, the only way of restoring Greek competitiveness is to wait while Greek wages and prices fall -- but this will not only take years; it would have the further highly unwanted side effect of further increasing the real burden of Greek debt.

Much good advice is being dispensed in the financial media about how to handle Greece's problems in an orderly, even optimal way. An orderly solution would mean several things at once: an agreed recheduling or restructuring of Greek obligations that decides how the pain is shared between Greece and external debtors; a fiscal programme that decides how the domestic adjustment is shared between taxes and spending, and between the various claimants on the Greek government; and a long term programme to liberalize Greek wages and prices and restore competitiveness.

There is nothing in the economic history of Russia or any other country to suggest that there can be an orderly solution for Greece. If an orderly solution was possible now, the problem would never have reached this point. Rather, it is more or less certain that the Greek crisis will break while everyone is unprepared, and it will work out in a chaotic, unplanned way, with unforeseeable consequences for Europe. For, without an exit from the Euro, the Greeks have no prospect of the rapid recovery that Russia made. An orderly exit from the Euro: what are the chances of that?

The Russian financial crisis came to a head in August 1998, unexpectedly, when many government officials, bankers, and IMF staffers were on vacation. As you pack your bags this summer, think about it.

P.S. I sincerely hope to be wrong.

Mark Harrison

24 Jun 2011 22:33

| ![]() Tags: Banking Economics Greece Recession

| Comments (0)

| Report a problem

Tags: Banking Economics Greece Recession

| Comments (0)

| Report a problem

April 26, 2011

The History of Britain's Public Debt Does Not Give Grounds for Complacency

Writing about web page http://www.johannhari.com/2011/03/29/the-biggest-lie-in-british-politics

Twice recently, the journalist Johann Hari has suggested that we are going through a manufactured crisis. The history of Britain's public debt, he argues, show that present levels are modest and there is no need for precipitate action to restrain government spending:

Here’s the lie. We are in a debt crisis. Our national debt is dangerously and historically high. We are being threatened by the international bond markets. The way out is to eradicate our deficit rapidly. Only that will restore “confidence”, and therefore economic growth. Every step of this program is false, and endangers you.

Let’s start with a fact that should be on billboards across the land. As a proportion of GDP, Britain’s national debt has been higher than it is now for 200 of the past 250 years.

The quote is from Johann Hari's blog, The biggest lie in British politics(March 29, 2011). Before that, in When will David Cameron's soufflé of spin collapse?(February 11, 2011) Hari wrote:

Beneath Cameron's entire agenda runs the biggest lie of all: that Britain is facing an "unprecedented" level of debt. In reality, Britain's national debt has been higher as a proportion of GDP for 200 of the past 250 years.

The full argument, widely blogged and tweeted, goes like this:

- Current debt levels are historically modest.

- So, there is no need for drastic action to contain the debt through deficit reduction.

- In fact, advocates of public spending reductions are creating a phoney sense of emergency in order to vandalize the welfare state for other reasons.

On a closer look, this line of reasoning raises interesting issues. Here is a chart that shows the evolution of Britain's public debt as a percent of national income since 1692:

(The figures from 1692 to 2010, and a forecast for 2011, compiled by Christopher Chantrill, can be found at http://www.ukpublicspending.co.uk/. I added the Office of Budget Responsibility forecasts for 2012 to 2014.)

First, is it true that Britain’s current debt level is historically modest? Yes, clearly -- although Hari exaggerates. As of 2011, Britain's debt ratio has been higher than it is now for just 169 (not 200) of the last 250 years (or you could say "200 of the last 282 years").

Next, is there anything else of interest in these figures? Well, since the level of debt today is the sum of past changes, we could also look at the rate of change of Britain’s public debt. Interestingly, there have been just 36 years in the last 320 when the debt grew faster as a percent of GDP than in 2009 to 2011. Let me give some twentieth century examples, and you'll get the idea. One run of years when the public debt climbed faster was 1915 to 1919. Another was 1941 to 1946.

In other words, Britain's debt has been growing in the last couple of years at rates generally exceeded only in major wars. It's particularly dangerous because, as I explained here, debt has persistence. Once the conditions have been created for it to grow rapidly, it'll go on rising under its own momentum until you take steps to control it. The longer you leave it, the harder it gets.

In some general sense, however, Hari has a point. It's true that Britain’s debt has been higher than it is now for more than two of the last three centuries. He overstates the case, which I dislike, but I accept that most policy advocates do that most of the time, and they can't all be wrong at once.

Now, some economic history. My point here is that there are important reasons why Britain today cannot handle the 200% plus debt ratios that characterized the 1820s (after the Wars of the Austrian and Spanish Successions, the Seven Years' War, and the Napoleonic Wars) and the 1950s (after World Wars I and II). If much higher debt levels were okay then, why not now? The answer begins with: because times have changed. We no longer live in the 1820s or the 1950s. It’s the twenty-first century.

How did Britain sustain that kind of debt in the past? Well, how do you handle a debt that is twice your income? The important thing is that you have to be able somehow to limit the interest payments. If debt is twice national income, as long as you can borrow at no more than 3%, you have to transfer only 6% of national income each year to bond holders. But, if the interest rate goes up to 12.5% (as it is today for Greece and Ireland) then the transfer eventually goes up to an infeasible 25% of national income. Basically, you’re insolvent.

How do you keep the interest rate down to 3%? In one of two ways. Either you dominate the world capital market – as Britain did in the eighteenth and nineteenth centuries. Or, you close the domestic capital market off from the world, so you can dominate your own little pool of saving – as Britain did in the mid-twentieth century. Either way, you can borrow if there's no one else for people to lend to.

In the eighteenth and nineteenth centuries, Britain could handle a much higher debt ratio than today’s because an integrated global capital market developed in which the British economy was the major borrower and lender. There was little credible competition with British bonds. As a result, British public debt remained universally acceptable despite its relative abundance. (The United States has enjoyed a similar position since World War II, but the uncontrolled U.S. budget deficit may eventually put an end to that.)

Before the twentieth century, moreover, the British government did not have major commitments to social spending at home. The spending of the central government was principally on administration and defence. As a use of government revenue, interest payments did not have to compete with major entitlement claims. This kept government guarantees of repayment credible.

The two world wars broke up the global capital market. Although no longer the world's financier, in the mid-twentieth century Britain could continue to handle a much higher debt ratio than today’s for a reason that was completely different from before. In a closed domestic capital market, British bonds were protected from competition. British lenders could not freely buy the bonds of other countries, even if they wanted to, because of government controls on foreign exchange and capital movements. With alternatives kept out of the market, British public debt continued to be acceptable at home.

Today, these conditions have gone. There is a global capital market again. British bonds have no specific advantage for foreign lenders (as they had in the eighteenth and nineteenth centuries), and domestic lenders can pick and choose among bonds issued by many countries (something they could not do in the middle of the twentieth century).

This is why a level of debt that was sustainable decades or centuries ago is not sustainable today. Today, no one has to lend to the British government for lack of alternatives. In short, whether or not it is true, it is irrelevant that "Britain’s national debt has been higher than it is now for 200 of the past 250 years." The conditions of those 200 years have gone.

Here is the first reason why it is important for the British government to control the level of public debt: the day of reckoning would be upon us if we didn't. A combination of rising debt, declining confidence, and rising interest rates would then force us to close the budget deficit even faster than planned at present. The world doesn't owe us a living; we already owe them. In fact, don't feel sorry for us; feel sorry for Americans that the U.S. Treasury has enough discretion to put off its day of reckoning until the fiscal mess there will be still more dire than it is now.

The world has changed; for Britain, has it changed for better or worse? Some people might think "for worse." There are those that don't like globalization on principle; others might wonder, more pragmatically, whether the conditions of the capital market half a century ago could be restored. Talk of capital controls is in the air again. If capital account liberalization made it more difficult for us to carry on with deficit spending and a rising public debt, then why not restore the protected capital market regime of the 1950s?

The case might be that, by restricting the choices of British lenders again, we could increase the domestic demand for British debt. (By the same token, however, we would also eliminate the foreign demand.) On closer inspection, this course of action hardly recommends itself. When lenders lose the will to lend, as with Greece, Ireland, and Portugal, it is usually for good reason. Taking away their option to buy elsewhere would amount to sticking fingers in our ears so as not to hear bad news.

Besides, if we restored the conditions that enabled the government to borrow more than twice GDP, what reason is there to suppose that the government would make better use of the money than private borrowers? Still one of the richest countries in the world, Britain’s prosperity has come from private enterprise and innovation, industrial and commercial revolution, and trade and finance; it did not come from Whitehall.

To finish up, the second reason for fixing Britain's debt while it is still at today's historically "modest" level is that having a debt twice your income is a sign that something went terribly wrong; a run of major wars, for example. Faced with the worst recession in 80 years, the British government was right to let its budget go into deficit temporarily. At that moment an increase in Britain's debt was inevitable. Now it's right to bring it back under control over a few years.

So, if the British government today cannot dominate its capital market and continue to eat up national resources beyond the willingness of the population to pay taxes -- there is reason to be glad.

Mark Harrison

26 Apr 2011 18:18

| ![]() Tags: Economics Keynes Recession Using-Data

| Comments (0)

| Report a problem

Tags: Economics Keynes Recession Using-Data

| Comments (0)

| Report a problem

April 24, 2011

Surely You're Joking, Mr Keynes?

Writing about web page http://www.debtonation.org/wp-content/uploads/2010/06/Fiscal-Consolidation1.pdf

The British government is seeking to bring the public debt under control by cutting back public spending. A popular story is going around, however, that suggests this is either crazy or a thinly disguised plot to undermine the public sector; see for example Johann Hari's blog, The biggest lie in British politics, March 29, 2011.

How does this story work? It runs like this. Start from the government’s plan for cutting public spending:

- With lower spending, the national income will fall.

- With lower national income, tax revenues will fall.

- With lower tax revenues, public borrowing will remain high.

- With public borrowing still high, the public debt will be hard to shrink.

- The burden of the debt relative to GDP could even rise.

In this story, the public debt is hard to control because it pushes back when the government tries to cut spending. It pushes back so hard that cutting public spending is actually counter-productive. In fact, the story implies that the government should spend its way out of debt! This is because more public spending would generate higher national income, higher tax revenues, less borrowing, and less debt relative to GDP.

How good is this story? It has a logic, purely Keynesian in spirit. But is it true? One issue could be that it leaves such factors as business confidence and the exchange rate out of the calculation. Ultimately, however, it’s an empirical question. That is, it can be answered by looking at how the public debt has actually responded to changes in public spending in the historical record.

It’s clear how both the UK Treasury and the independent Office of Budget Responsibility answer this question. They predict that, with the current fiscal squeeze, Britain’s public debt will rise more slowly, peak in 2014 at around 70 percent of GDP, and then start to fall. In other words, deficit reduction will eventually win. Given enough time, cutting public spending will not be counterproductive.

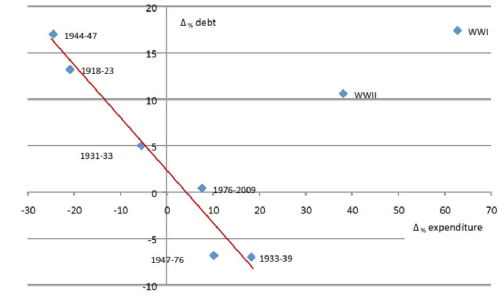

The Economic Consequences of Mr Osborne is a paper that Victoria Chick (of UCL) and Ann Pettifor (of the New Economics Foundation) circulated in June last year. It tells a more pessimistic story. It uses a century of data to suggest that the public debt varies negatively, not positively, with public spending. Fiscal cutbacks, they conclude, have consistently increased, not reduced, the burden of public debt. The key result is illustrated by their figure, below. The figure compares the change in the burden of the debt relative to GDP (the vertical axis) with the percent change in nominal public spending on goods and services (the horizontal axis), measured in annual averages over varying periods of time. The idea, I guess, is that nominal spending is the one thing over which the government has direct control; how does it affect the burden of the debt?

This chart suggests that a change in the public debt is negatively associated with a change in nominal public spending. When public spending falls, debt rises. Chick and Pettifor also report this result as a regression (the Δ symbol means “change in”):

Δ public debt/GDP = 2.2 – 0.6 x Δ public spending

Notes:

- The 2.2 means that the public debt would have risen on average by 2.2 percent of GDP per year in every episode if public spending remained unchanged.

- The 0.6 means that, in addition, debt tended to rise by 0.6 percent of GDP for each one percent cut in nominal public spending.

- Chick and Pettifor state that this relationship explains 98 percent of the total peacetime variation in the debt.

There are two implications. One is that deficit reduction is pointless because it will worsen the burden of the debt. The other is that the government can and should spend, not save its way out of debt.

This finding has been widely blogged and tweeted. It even made its way into a quarterly newsletter of the Royal Economic Society. But I have not seen any serious commentary so far. So, let me try. To begin, there are four odd things about the picture in the chart.

- The compression of 100 years of annual data into eight data points.

- The exclusion of the two data points that don’t fit (the two World Wars).

- The six data points that are used to fit the line are very different in coverage, ranging from two years (1931 to 1933) to 32 years (1976 to 2009).

- Regardless of the length of the period covered by each data point, the effect of public spending on debt is assumed to be exactly contemporaneous.

Is this a sufficient basis for a very important policy prescription? In my view, absolutely not.

Let’s look again at the data, which Chick and Pettifor helpfully provide in an appendix. Like them, I'll use nominal public spending changes to try to predict changes in the public debt burden. Unlike them, I’ll use all the data. I won't leave out any inconvenient observations. I’ll work on the basis that, if the relationship we are looking for exists, it ought to be simple and direct; it should not be instantaneous, but it should be speedy; and it should be there, year on year, in every period, regardless of other circumstances.

One other thing I'll do differently: Remember the 2.2 percentage points a year of upward drift in the debt burden that Chick and Pettifor found. Remember also the official forecasts that expect the Osborne budget cuts at first only to slow the growth of the public debt; not until 2014 will the debt start to fall relative to GDP. This reflects an important problem that Chick and Pettifor left out of account: the burden of debt has a momentum of its own.

What does this mean? Suppose there is a lot of public borrowing, causing the debt to rise rapidly. If the government reduces its deficit but does not eliminate it, the public debt will go on rising, but more slowly. It will not fall until the deficit is closed altogether. Moreover, while it is rising, the additional interest payments will be added to the debt, increasing it further. In other words, whether or not there is pushback in the public debt, there is certainly persistence. This is matched by the data, which suggest that public debt has moved systematically up or down over long periods under its own momentum. You can't ignore this if you want to understand how current fiscal policies affect the evolution of the debt.

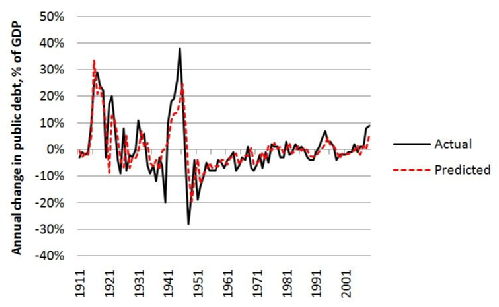

My own calculation uses year-on-year changes in public spending (percent of previous year) and public debt (percent of GDP) from the Chick-Pettifor data. It allows the change in the public debt in a given year to be influenced by not one but two things, both in the previous year: how public spending was changing, and how the debt itself was changing. Including the latter means we can work out the historical persistence factor in the change in the debt from one year to next year. Using Δ to mean “change in” and “(-1) to mean “in the year before,” here are the numbers that come out:

Δ public debt/GDP = -0.01 + 0.74 x Δ public debt/GDP (-1) + 0.14 x Δ public spending (-1)

Notes:

- The 0.74 means there is quite a lot of persistence in the debt: if public spending was unchanging, but the public debt increased by one percent of GDP, it would increase again by 0.74 percent the following year.

- The 0.14 means that the historical relationship between a change in the public debt and the change in public spending one year previously is actually positive. This is the most important result. Allowing for the persistence factor, if the government increased nominal public spending by 1 percent, the public debt tended to rise by 0.14 percent of GDP the following year.

- The explanatory power in this relationship is quite high. For the experts, the t-ratios of the 0.74 and the 0.14 are 11.0 and 5.2 respectively, meaning that the probabilities of finding this pattern by accident are extremely low. Nearly 60 percent of the total historical variation of the change in the public debt is explained. Of course, this is much less than the 98 percent that Chick and Pettifor say their model explains. I set myself a far stiffer test, however, by using 98 (not 6) observations, so that there is much more variation in the data to be explained. I also included all the years that Chick and Pettifor arbitrarily dropped in order to get their result.

The next figure shows how well the regression equation predicts the actual year-on-year changes in the debt ratio over the whole period.

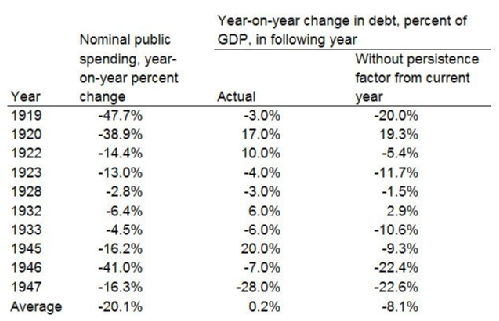

As a final check, I narrowed my focus down to those years in which nominal public spending actually fell. Public spending was unlikely to fall without a deliberate government policy of fiscal consolidation. Never mind what happened on average across the century as a whole; what happened to the public debt when the government took an axe to public spending? There were just ten such years within the sample. This is what happened in them.

The first column shows that in these years nominal public spending was cut on average by 20 percent. The second column shows that in the next year the debt burden did not fall on average, and even rose slightly. Perhaps Chick and Pettifor would see this as validation of their idea. But it ignores the persistence factor in the debt. In most years that public spending was cut, there was already a large deficit that fuelled rapid growth of the debt. Unless the deficit was eliminated immediately, the debt would still grow, but at a slower rate. In the third column, I estimate how the debt would have behaved without the inherited momentum. On that basis, the debt would have fallen in eight of the ten years shown, and it would have fallen on average by 8 percent of GDP.

I'd never claim that this is the best that can be done. I do claim that, if you treat the same data properly, they can tell a very different story from the one that Chick and Pettifor come up with.

To sum up: Deficit reduction works. As for the Chick-Pettifor story, it is not completely wrong. There is a grain of truth in it. Once the public debt is set on a particular course, it is hard to change that course quickly. But it is just persistence that takes time to reverse; it is not a pushback so strong that trying to controll it becomes pointless or counterproductive. Once we allow for the momentum of the debt burden, we can uncover the simple, intuitive, positive relationship between spending and debt that even a non-economist might expect to find.

At the beginning I outlined a Keynesian story that starts with deficit reduction and ends with an increased burden of the debt. It is an intriguing story and it is popular among those that are easily satisfied when a result seems to match their preconceptions. But, like many intriguing stories, it is a fiction. What the figures actually show is that more public spending means more public debt.

Spend our way out of debt? Surely you’re joking, Mr Keynes.

Mark Harrison

24 Apr 2011 23:11

| ![]() Tags: Economics Keynes Recession Using-Data

| Comments (2)

| Report a problem

Tags: Economics Keynes Recession Using-Data

| Comments (2)

| Report a problem

March 18, 2011

Student Finance: Bias at the BBC?

Writing about web page http://www.bbc.co.uk/news/education-12767850

According to a new report on the BBC website, headlined in last night's BBC TV and Radio news, "Graduates 'could pay back double their student loans."

It sounds scary. I can see another few hundred families around the country listening to the news and deciding university sounds just too expensive.

That would be a shame. There is a story here, but it is not the story on the surface. It is a deeper story, one of distortion and misrepresentation.

- First: There is nothing new in this "news."

Anyone who borrows will eventually repay more -- mechanically adding up the cash amounts, year after year -- than they borrowed. Interest charges ensure this result. Moreover, the longer is the period over which you borrow, the greater is the excess of cash repayments over the initial loan.

But why do borrowers pay interest? Because not having to wait is valuable. This has an important implication. A pound today is worth more than a pound next year or the year after. When you take out a loan, you've made the calculation that it's better to have the house or car now than wait for years in rented accommodation or sharing public transport while you save up. It's better to borrow and buy despite the fact that, having borrowed, you will have to repay more later.

By the same argument, the money you will have to repay next year should be considered worth less than the same money now. This is called discounting: we discount the future compared with the present.

Because future money has to be discounted to find what it is worth today, it is wrong to add up money in different periods without adjustment. Rather, the future values should be discounted, year by year, before they are added up.

Imagine the following scenario. In the BBC's story, the graduate has a debt of £43,000. In my scenario, you decide to borrow the same sum, but as a fixed rate mortgage, not a student loan. Suppose the lender's interest rate is 3 percent a year. Suppose you repay the debt in full, in equal annual instalments over 30 years.

On these assumptions, the sum of your undiscounted cash-out repayments will be a little over £67,000. But, if we revalue your payments in every year by discounting them back the present at 3 percent annually, the present value of the sum of your discounted repayments will fall to ... oh, £43,000.

The present value of the repayments is the same as the value of the loan!

- Second, therefore, there is no story. You repay -- in present value -- exactly what you borrowed.

But wait. That leaves a puzzle in the BBC account.

Remember that, in my example, you repaid everything at the market interest rate, and yet the undiscounted sum of your cash-out repayments was just £67,000, compared the £43,000 borrowed.

Compared with that, under the government's student finance proposals, graduates will enjoy three concessions. They'll repay nothing, and accrue no interest, while their salaries remain below £25,000. Between £25,000 and £41,000, they'll pay a reduced interest rate. And anything outstanding after 30 years is forgiven. Under those assumptions, surely, graduates should end up repaying less than you?

Yet, in the BBC version, graduates have to repay much more than you. The BBC puts the sum of undiscounted repayments at sums varying between £72,000 and £84,000, depending on the income of the graduate. It's the latter figure that lets them claim: "Graduates 'could pay back double their student loans."

What's going on?

The BBC commissioned "leading accountants," including the firm Baker Tilly, to support this story. It's based on a spreadsheet, available from the BBC website, "showing the calculations." The spreadsheet shows that the BBC's accountants sneaked in a hidden assumption, not reported in the story.

They built in 2 percent yearly inflation. In each year, they added 2 percent inflation to the repayment thresholds, 2 per cent inflation to the graduate's salary, and 2 percentage points to the interest paid.

What's wrong with that? Nothing -- except this: The 2 percent inflation assumption also pumps up the nominal undiscounted cash sums that their graduate repays every year. That was how they made the figures support that scary headline: "Graduates 'could pay back double their student loans."

Inflation is a further reason why it's wrong just to add up the column of annual cash repayments. Except in the first year, the annual payments are not in present-day prices. They are in different prices of different years, all of them higher than today's and some of them much higher. It's just plain wrong, and misleading, to lump them all together.

The BBC's calculation should have been done throughout in constant prices, so that the purchasing power of £1 would be the same in every year. But, if done at constant prices, there would have been less of a story. After proper discounting, there would have been no story at all. In fact, it would have emerged that:

- Most graduates will repay less, in present values and constant prices, than they borrow at the outset.

This brings us back to "the leading accountants." Given who they are, I guess they know their stuff. But do they? The mess behind this story leaves only two possibilities. They understood these issues perfectly well when they made their calculations -- or they didn't.

Either way, it looks bad for the accountants. Incompetent, or colluding with a misleading agenda? I'll leave it to you to decide on that.

It looks bad for the BBC, too. Remember, this is not the BBC reporting the news. It is the BBC inventing the news.

- Finally, a note for readers interested in open-source data.

The BBC website provides the spreadsheet with the figures, in their words, "showing the calculations." That's good.

The problem is that, before uploading the spreadsheet, they converted all the spreadsheet formulae to values. It is the formulae that enable to user to track the links from one number to another, and see at a glance how the calculations were made. The truth is that the spreadsheet does not show any calculations at all, only numbers. That's bad.

I can see no purpose in it, except to make checking more difficult.

Mark Harrison

18 Mar 2011 12:21

| ![]() Tags: Economics Universities Using-Data

| Comments (5)

| Report a problem

Tags: Economics Universities Using-Data

| Comments (5)

| Report a problem

January 09, 2011

Mine's a Litre: Are We Paying Too Much for the Road Lobby?

Writing about web page http://www.guardian.co.uk/business/2011/jan/09/fuel-prices-truckers-threaten-blockades

Yesterday a friend asked if I liked UK Petrol Blockade 2011. It turned out to be a cry for Something to Be Done:

Fuel has gone up too far now the tax is mad By the end of 2011 it will rise to over 1.50 a litre so remember the petrol blockade in 2000 Time for that again i say it will lose the Fuel companys money so the government will also lose money and look bad as the companys will add pressure on to the government so will have to do something about it it will take time but we need to do something now

I didn't take this too seriously until this morning, when I read in The Observer:

The spectre of trucks blockading streets in protest at record fuel prices – on top of student and public-sector worker demonstrations – will be raised tomorrow when the haulage industry unveils a campaign to force government to halt rises in petrol duty.

I thought hard about this. What was it all about? It seemed to be aimed at the government. Maybe the logic behind it was this:

- Fuel taxes are rising because the government needs more revenue just to pay for public services and welfare benefits that are currently funded from borrowing. Let's stop the government raising some of the taxes it needs, and force them to strip even more funding out of benefits, care homes, and so on.

No, it couldn't be that. Maybe the real target was the oil companies:

- Pension funds are already hurting because BP suspended dividend payments after the Gulf oil spill. Let's hit the pensioners even harder by disrupting oil company operations so that they face higher costs and lose more revenue and profits, and cut dividends further ...

No, it couldn't be that, either. Maybe it was simpler than I thought:

- Consumers are already hurting because of job losses and price and tax increases. Let's hurt them some more by blockading fuel supplies so that we can't move around, go to work, or buy stuff ...

Hmm. Somehow, I thought, we're getting further and further away from reality. This was my last throw:

- Food and oil prices are rising because the global economy's recovering from a dangerous recession. The recovery is increasing jobs, incomes, and the demand for commodities. As a result, oil prices have risen again. If the recovery is the problem, the solution's obvious. Let's stop the recovery and take the economy back into recession. If we can bring back the recession, oil prices can drop back down, making it cheaper for the people who lose their jobs a second time to drive the cars they won't be able to afford any more ...

I'm still struggling with that one.

The fact is that fuel should be taxed, for two reasons. First, fuel taxes are hard to avoid, so it's a good way to raise revenue. Second, burning fuel emits a lot of pollution and carbon dioxide, and the people that use it should pay society back for the damage they do to the environment we all have to share.

Is there any kind of case for giving the road haulage industry special treatment? A case that's been made involves unfair foreign competition.

Britishtruckers.com is arguing that UK firms are more at risk because of competition from abroad with foreign vehicles able to operate in Britain using cheaper fuel picked up on the continent.

It sounds compelling -- but think about it. There is less here than meets the eye.

Some truckers compete with foreign vehicles; others don't. The ones that face foreign competition are on the same routes as vehicles from overseas. That means they have exactly the same opportunities to pick up cheap fuel on the continent as their competitors. It's their choice if they fail to do so. No unfairness there.

In reality, the truckers that compete internationally are a situation no different from those that compete in the domestic market. If their fuel costs go up, they can either pass them on or not. If they can pass higher costs on to the customer, they're all right. If they can't, because their customers won't pay, there's a message in that -- like it or not.

It's not a case for special treatment.

On one point, I agree. In the UK, taxes on fuel are too high, relative to road charges. Fuel taxes should come down and, to compensate for this, congestion charges should be put in place in city centres and motorways. (And, of course, these charges will be paid the same by British and foreign truckers.) Why should this happen?

It is costly to provide roads, but in the UK nearly all road use is free. Because road usage is not priced, many of our roads are over-used. As a result, there is pressure to expand the road network, creating costs that would be avoided if road usage was not free of charge.

Other results of our lack of road charging include excessive wear and tear of roads (mainly by heavy trucks) and congestion (mainly by light passenger vehicles). Congestion wastes everyone's time and also increases fuel consumption because vehicles burn too much fuel while idling, creeping forward, and starting and stopping.

Some of the burden on motorists should be shifted from taxes on fuel consumption to charges for road usage. With less traffic on the most congested roads, we can save money on providing and maintaining them, and less time will be wasted in queues and jams. We could all end up better off.

There's only one problem: Campaigners for lower fuel taxes often turn out to be the most vehement opponents of road charging (not to mention speed limits, speed cameras, traffic lights, and other stuff). In other words, they're not interested in improving things for society. They just want to shift the costs of their own choices and activities onto other people.

Ironically, therefore, the road lobby itself is one of the biggest obstacles to moving towards a more efficient distribution of the tax burden -- including lower fuel taxes. Everyone's aware of the price we pay for petrol, but what about the price we pay for the road lobby? It may be higher than you think. Someone should do something about it.

Mark Harrison

09 Jan 2011 19:51

| ![]() Tags: Economics Politics Recession

| Comments (2)

| Report a problem

Tags: Economics Politics Recession

| Comments (2)

| Report a problem

December 31, 2010

Russia in 2010: One Step Forward, Two Steps Back

Where will Russia go in 2011? Under Putin and Medvedev, Russia is not a democracy but the Russian government is not heading back to Soviet-type totalitarianism. The absence of political competition is not the primary problem; it is the absence of the rule of law.

Russia today has markets and private property. It is not the Soviet totalitarian state; nor is it, strictly, a “mafia state.” That is one step forward. But Russia’s government seeks the power to intervene at will, selectively and at its own discretion, in markets and property relations. The government stands above the law. The result is two steps back. You can see this clearly in four stories from 2010.

Story no. 1: Russia suffered a harvest failure and nobody died

My first story comes from agriculture. The summer of 2010 saw a severe drought across Russia. Harvests failed disastrously. In the Soviet past, failures on similar proportions occurred in 1932 and in 1946. When that happened, there were severe regional famines in which millions of people starved to death.

After the harvest failure of 2010, two things happened that were in striking contrast with the Soviet past. First, no one died. Instead, when food prices at home threatened to rise, the Russian government responded by imposing an export ban, requiring Russian food suppliers to break their contracts with foreign buyers. Second, this exposed the fact that, for the first time since the 1920s, Russia is exporting food to the West. Under a market economy, Russian agriculture has become a competitive success. (It does not take much to be a success by Russian standards.)

The reflex responsive of the Russian administration was a bad sign, however: to try to control prices by restricting the market and breaking contracts. This will limit the incentives for Russian farmers to make the forward looking investments that will reduce harvest volatility in the future. Foreigners will become less ready to make forward contracts for Russian exports, knowing the state can override them at any time.

Story no. 2: President Medvedev has seen the future, but can he make it work?

In 2010, President Medvedev visited Silicon Valley – the urban sprawl south of San Francisco that has generated the world’s biggest concentration of innovation start-up ventures. Now, the Russian government wants to build an analogue in the district of Skolkovo outside Moscow.

The goal is to promote five presidential high-tech directions (one is tempted to substitute the Soviet-era jargon of “priorities”) of modernization: Energy production, IT, telecommunications, and bio-medical and nuclear technologies.

There is some sound logic behind this. Yes, it’s true that economic development involves new urbanized configurations. Yes, it’s true that Russians don’t live today in the right places for innovation.

Most Russians are spread out across Russia’s vast landmass in small and medium sized towns. They are too immobile (apart from the ones that have gone to live abroad, many in places like Silicon Valley). Lots of young people need to move to big sprawling cities and suburbs to squash up and rub together, mix ideas and talents, get funding, and start up new innovation-based ventures. In fact, quite a lot of them would like to, but can’t because Moscow is congested and operates a restrictive system of residence permits.

Like other poor countries, Russia may also need to experiment in new ventures to uncover new comparative advantages.

In short, there is a respectable case for the Russian government to do more to encourage movement away from rural districts and remote small towns, and let its largest cities grow further. It should also stand ready to subsidize pioneering entrepreneurs.

But what Medvedev actually has in mind is to create a controlled environment for approved people and favoured companies to sit in a green field outside Moscow. This is not the process that gave rise to Silicon Valley. The Russian government will not be able to commit itself not to meddle and grab. The powerful military-industrial lobby will not be able to stand aside and let individual enterprise make and take profits.

If it is ever built, Russia’s new innovation city will drain the state budget of grants and subsidies. There will be just enough spin-offs that everyone will declare it a success. The aggregate net benefit will be zero or negative.

Story no. 3. You have been warned: Russia has a new law on the secret police

After the Soviet Union collapsed, Russia went from a government system of micro-controls on everything to too little government control. In the 1990s, public confiscation was replaced by “piratization” (from the title of a book by Marshall Goldman). The Russian state went from having far too much capacity to having too little capacity to raise taxes and regulate public life. In fact, the thing that gave the first Putin administration its legitimacy was public recognition that some restoration of state capacity was deeply necessary.

Up to a point.

But Prime Minister Putin is ex-KGB, and part of his mission has been to restore the power and prestige of Russia’s secret services.

Russia’s Parliament has given first reading to a new law on the FSB (the domestic security service), which illustrates the direction of movement today. It gives the FSB the power to issue legally binding warnings to people who might be about undertake illegal actions. This reinstates the legal basis of the KGB practice of controlling the behaviour of persons who were on the edge of politically or culturally deviance or defiance by warning them off.

The reinstatement of the early warning system matters not only in itself, but for what must lie beneath. The KGB’s ability to control deviance by giving out early warnings rested on a vast apparatus of informers and mass surveillance. It could hand out tens of thousands of warnings a year across the vast Soviet territory because it kept individual tabs on millions. Mass surveillance enabled the selective intervention that kept the population quiet and conformist.

The new law on the secret police does not bring back totalitarian control, but it makes little sense unless the FSB is quietly rebuilding its networks of spies and informers on a mass scale.

Story no. 4: Some go to jail, some go free

After the violent London demonstrations over tuition fees, the British police identified and arrested 180 participants suspected of carrying significant responsibility. After race riots in Moscow, the Russian police rounded up no less than 800 ringleaders (I don’t know what happened to them after that). So there is something, at least, that the Russians can do better!

Probably, no one I know is going to shed any tears over the fate of violent ultra-nationalists and fascists. I confess to feeling ever so slightly sorry for them. They were used by the Russian government as a lightning rod until the voltage ran out of control. Now they can be slapped down, at least for the sake of appearances. Moreover, the same police that could locate and arrest hundreds of suspects in the course of weekend doesn’t seem to be able to find the murderers of dozens of journalists killed in Russia in the Putin era. Hmm.

Which brings me to the latest victim of selective Russian justice: Mikhail Khodorkovskii. Khodorkovskii was put away originally for trying to break away from the “mafia state” that originally gave him his fantastic wealth. The first time, he was put away for evading taxes on his company’s profits. The second time, it was for stealing his company’s entire revenues.

If you treat this literally, it is then hard to explain how it was that his company was making taxable profits at the same time that Khodorkovskii was stealing the revenues. But the underlying principle is not that complicated. In Russia, the state decides first who is guilty. Then, it decides what they are guilty of.

It is cheering to see violent thugs get what’s coming to them, but it is still a mistake to cheer when you see a few unpleasant people put behind bars. Under the rule of law, you go to prison because you have broken the law, not because some official has decided you might be a threat.

These four stories suggest where Russia is moving: towards a state with increased discretionary power to intervene as it chooses to control prices and direct resources, subsidize favoured interests, control deviance, and lock up or kill inconvenient people. By the standards of Russia’s Soviet past it is definitely one step forward. This one step is hugely important. Russia is no longer a totalitarian state of mass mobilization and thought police. But, compared with the “normal” society that Russians deserve, and that Russia's friends wish for, it is two steps back again.

PS The best things I have read about Russia recently are:

- How law may come to Russia, by Anatol Lieven in the Financial Times, December 6, 2010.

- And, on Medvedev versus Putin, The Khodorkovsky Verdict: The Power Struggle Is Now On, by Paul Gregory in his blog, December 28, 2010.

Mark Harrison

31 Dec 2010 10:25

| ![]() Tags: Economics Politics Russia

| Comments (3)

| Report a problem

Tags: Economics Politics Russia

| Comments (3)

| Report a problem

October 21, 2010

The Welfare State: Reports of Death Exaggerated

Writing about web page http://www.direct.gov.uk/prod_consum_dg/groups/dg_digitalassets/@dg/@en/documents/digitalasset/dg_191696.pdf

Panic is in the air, especially in the British public sector. Yesterday's comprehensive spending review prompted BBC Radio CWR to ask me this morning if this marks the end of Britain’s welfare state.

There will be a major contraction, for sure. At the same time, it is far from the end of welfarism as we have known it since the late 1940s. George Osborne’s cuts, if and when they take effect, will bring the government’s share of GDP back down just below 40 percent – that is, where it was in the early 2000s. At that time, less than a decade ago, the welfare state was still alive and well.

What will have changed? Most likely tomorrow's welfare state will be smaller than it is now. And the principles on which it is based are evolving. But given the scale of cutbacks, the evolution of the principles is surprisingly slow.

Principles of the Welfare State

At their simplest, the principles of welfare that were implemented after World War II can be put like this: The state would make minimum provisions for everyone. Coverage would be universal; no one would be allowed to opt out. The insurance provided would be lifelong, from the cradle to the grave. Everyone would contribute according to their means; everyone would get the same low, flat-rate benefits in case of need at any time in their lives.

At first sight, it’s not obvious why we, as a country, couldn’t afford this now and forever. After all, the main changes that have happened since 1950 would seem purely advantageous. On average, we are several times richer now than then. On average we lead longer, healthier lives. What could spoil this?

At the core of the problem is a simple fact: while our lives have improved rapidly, our sense of entitlements has increased out of proportion. This is best illustrated by the problem of pensions.

Why Old Age has Become a Problem

Work produces the wages and profits that are taxed to pay for the welfare state. Since 1950, childhood and retirement have encroached on the years of life in between, during which most people work.

- In 1950, many people left school at age 14. Today, in contrast, many do not enter the workforce until their early twenties.

- In 1950, male retirement was normally at age 67. Today, the average age of men’s retirement has fallen to their early sixties.

- In 1950, most men died before retirement. Only a minority lived long enough to collect a pension. Today, men’s life expectancy has increased to exceed the retirement age by about 15 years.

Old age has become a joy for millions. Free of family chores and work responsibilities, still in good health, our seniors can please themselves – provided they have an income. But the proportion of retirees in the population is rising steadily while the proportion that works to pay for them is declining. It can’t go on.

The government is bringing forward increases in the normal retirement age, one year at a time. It would be more sensible to link these changes to measured life expectancy. For example, if we should expect to spend half our lives working, then the retirement age should rise by six months when life expectancy rises by a year.

From Universal Benefits to the Means Test

The principles of minimum provision and universal coverage are still surprisingly strong in the British welfare state. There is still universal health care that is largely free, and there is free compulsory primary and secondary schooling. There is still a universal state pension with universal pensioner benefits – free TV licenses, bus passes, and winter fuel allowances.

If anything, it is a problem that these benefits are too generous. They are no longer at the low level that made the welfare state affordable in the 1950s. The fault lies largely with the strength of the pensioner lobby – all those healthy voters with time on their hands and nothing better to do than demand more rights.

To me it is a scandal that, over 60, but in good health and in full time employment on a good salary, I'm entitled to a bus pass and a winter fuel allowance. We know winter fuel allowances aren’t spent on winter fuel. These benefits go to millions of people who are neither poor nor fuel-poor. The poor exist, for sure; but the idea of the "fuel-poor" is just a vote-selling scam.

Although the principle of universal benefits is still alive, the British welfare state has always imposed means tests for some entitlements. Their role has been increasing for some time; in fact, as chancellor under Tony Blair, Gordon Brown made important use of means tests to target funding on child poverty and pensioner poverty. George Osborne has now extended the practice, most notably by stopping child benefit payments to higher rate taxpayers.

it seems inevitable that high level income support and care funding will become ever more conditional and selective. This started long before George Osborne and will continue long after him. But the spirit in which it is happening right now owes a lot to the coalition government’s approach to fairness, as I see it.

The Undeserving Poor

The comprehensive spending review claims that the burden of cutbacks will fall disproportionately on the highest income groups. This claim has been criticized already on the grounds that it includes higher-rate income tax increases adopted by the outgoing Labour administration. Actually, it seems reasonable to me for the government to borrow some credit for this. Under better circumstances, surely, Conservative leaders would have liked to reverse the Labour income tax increases. To them, therefore, it was a deliberate choice to retain them. If that deserves a little credit, then let them have it.

Undoubtedly, however, a considerable burden must still fall on the poor. What I see in the spending review is a perspective on fairness that sets out to be fair to one section of the poor: the deserving poor. As for the rest, they are undeserving.

The idea of the undeserving poor goes back centuries; it is not even Victorian, although many Victorians followed it; see Alfred Doolittle’s well known definition.

Who, in George Osborne’s book of morals, are the deserving poor? They are the working parents and the pensioners that worked long and hard to save for retirement. To these will be given. To the undeserving poor, especially the parents that don’t work and the pensioners that took early retirement and didn’t save up for it, the spending review offers only tough love.

Controlling the Consequences

For a country of its size, Britain is said to have one of the most centralized systems of local government finance in the world. A significant paragraph in the spending review cuts away at overcentralization. While central government funding of local authorities will fall by one quarter, most of the ring fencing will be removed, freeing the hands of local councils to decide on local priorities.

Much of the non-cash dimension of the welfare state is decided locally through spending on social and care services, both residential and in the community. The removal of central government controls will increase local discretion over the amount of provision and the rules that say who gets it. And your local councillors, not your MP -- and not George Osborne -- will be to blame.

In Sum

The welfare state is not dead yet; managed prudently, it should last my lifetime and yours. But it will become smaller and less open handed.

Whether it will be more or less fair depends on your standpoint. If you care more about the equality of personal outcomes, then you'll see British welfarism moving away from fairness. If fairness is more about the balance between personal outcomes and personal efforts, however, you'll probably welcome the direction in which we are going.

There will always be unintended consequences. The process of change must create grave risks of harm to vulnerable and needy people. Against those risks is the impossibiity of continuing as we have done.

Mark Harrison

21 Oct 2010 15:33

| ![]() Tags: Economics Politics Recession

| Comments (0)

| Report a problem

Tags: Economics Politics Recession

| Comments (0)

| Report a problem

October 13, 2010

Higher Education: Who Else Should Pay?

Writing about web page http://hereview.independent.gov.uk/hereview/report/

A Browne study

The Browne report, Securing a sustainable future for higher education in England, says higher education should be paid for by those that benefit from it: our graduates. It also says they should pay later, in easy instalments, and only when they can clearly afford it, with all risk transferred to the government and universities.

It looks to me like a no-brainer ... Yet lots of people are showing signs of moral outrage.

A question the critics seldom address is: Who else should pay for my degree?

The taxpayer is usually implied. But here's the problem: tax-financed higher education involves a lot of poor-to-rich redistribution.

Robin Hood in reverse

Today's students are a large chunk of tomorrow's wealthy. Today's taxpayers, in contrast, extend well into the ranks of the poor. In the UK, you start paying income tax at an annual income of just £6,475. Under the Browne proposals, student loan repayments won't kick in until annual income reaches £21,000. If the graduate's income doesn't make it to that dizzy height, you pay nothing.

Somehow or other, there are people who figure it's fair for the guy on £6,475 to start paying for someone else, but not for the guy on £21k to start paying back. (If you take expenditure taxes into account, which everyone pays, it's even worse.)

I'm sad to see clever people, like Warwick's own student representatives, dressing up in the mantle of social justice to call for poor people to go on paying to make others richer than the payers will ever be.

They say that one thing clever people are good at is defending the indefensible. Is it them or is it me? Well, the reader can make that choice!

Better than a mortgage

The private net present value of a degree, according to an interesting but underexplained chart in the Browne report, is at least £100k (the actual figure shown is a bit over $200k, which is useful for international comparisons, but still confusing). If you include the "social contribution" from today's taxpayer, then it's a little more. For the sake of argument, let it be £120k.

Warwick University Students' Union puts the likely burden of student "debt" (I'm putting it in quotes, because it's not real debt like a mortgage, where they come after you if you can't make the payments*) under Browne arrangements, at "well over £40,000."

That sounds bad. But, the last time I checked, £120k minus £40k would still leave around £80k to enjoy. Nice.

* A roof over your head is a more fundamental right than higher education. Millions of working families, who have not had the benefit of higher education, take on much larger sums of mortgage debt in order to own their homes. If their incomes fall and they have to skip payments, they must sell up or risk repossession. Don't you think they'd jump at exchanging that for "debt" on the terms proposed by Browne?

And finally

My experience is that student finance is the one topic that attracts lots of comments. Feel free to say what you think. Right now, I don't promise to reply. That's not because I don't care or don't have an answer. It's because I've got to turn away from this to earn my salary! And do some teaching!

Mark Harrison

13 Oct 2010 11:17

| ![]() Tags: Economics Politics Universities

| Comments (17)

| Report a problem

Tags: Economics Politics Universities

| Comments (17)

| Report a problem

Loading…

Loading…