All 5 entries tagged Uss;

No other Warwick Blogs use the tag Uss; on entries | View entries tagged Uss; at Technorati | There are no images tagged Uss; on this blog

October 15, 2014

Birmingham talk powerpoint

I have just given a talk to an open meeting organised by the Birmingham University UCU.

If anyone would like to read my power point presentation, it can be downloaded from here.

Dennis Leech

15 Oct 2014 15:42

|

Dennis Leech

15 Oct 2014 15:42

| ![]() Tags: Pensions Uss;

|

Tags: Pensions Uss;

|  Comments (1)

|

Comments (1)

|  Report a problem

Report a problem

Please wait - comments are loading

Please wait - comments are loading

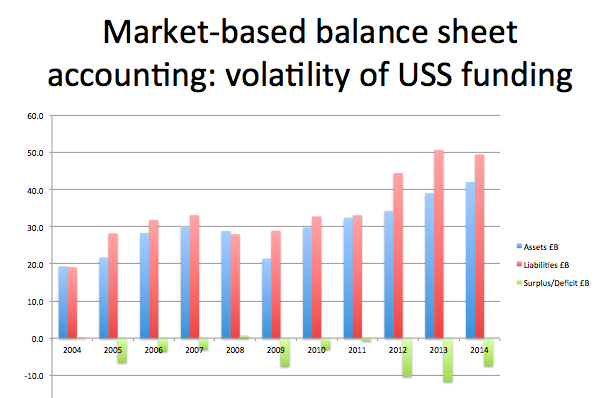

Poor and misleading reporting on the USS crisis by the Times Higher Education

I have just read an article by Jack Grove about the USS dispute (Universities unveil firm pension proposals) which is very very misleading.

He writes that there is a deficit of £8 billion PER YEAR. That is wildly incorrect. The deficit is not an annual payment. It is a notional capital sum and as such has no time dimension.

The USS deficit is the difference between the estimated value of the assets (an enormous approximate number) and a notional estimated value of the liabilities (another even vaguer approximation).Hence it is a wildly volatile figure with only limited practical meaning. (This diagram puts it in perspective. We should not get carried away by figures quoted in billions of pounds. We should get them in proportion.)

There is no "per year" deficit. In fact the latest Annual Report shows that the scheme makes a net surplus of £1 billion per year.

He also repeats the employers' claim that a reason for the deficit is poor investment returns after the financial crisis. In fact the USS's investments did well last year making a relatively good rate of return of 7.6 percent. It did not do as well as the Prudential but its performance was one of the best among pension funds. Whatever the reason for the deficit it is not poor investment returns.

Dennis Leech

15 Oct 2014 15:28

| ![]() Tags: Pensions Uss;

| Comments (0)

| Report a problem

Tags: Pensions Uss;

| Comments (0)

| Report a problem

September 23, 2014

USS Pensions: Reply to Private Eye

The current edition of Private Eye contains a highly misleading report about the universities' USS pension scheme (Gray-vy train, Eye no. 1375, 19 September-2 October 2014).

The report draws attention to the salary of the fund's chief investment officer, Roger Gray (up last year to £900k from the previous year's £600k) and suggests it is unjustified given the reported funding deficit leading to probable cuts in benefits to members.

It says:"While academic eyebrows will be raised over a pay packet more than 20 times as much as many of theirs, they might also question those running the scheme and responsible for the dubious investment policy."

This is actually a load of tripe (as the Eye might say). Last year the scheme's investment portfolio earned a respectable 7.6% return. (uss_warns_of_substantial_deficit_as_fund_returns_76_news_ipe.pdf.) It is the opposite of the truth to call that a dubious investment policy. Too often investors' bonuses are unrelated to performance but in this case Mr Gray's increase is actually based on good performance.

The article repeats criticisms of the USS investment policy that are familiar to anyone who has been following the debate. The deficit is actually a result of a controversial accounting methodology that treats the scheme as if it is one for employees of a small private company rather than the whole pre-92 Higher Education sector.

If the USS is regarded in the same way as other public sector schemes such as the Teachers Pension Scheme, on a pay-as-you-go basis, measuring its health in terms of its income and expenditure, it is actually in good shape: its income from its investment portfolio was over £1billion according to last year's accounts and with increasing membership.

Whether or not its investment strategy is wrong depends on which of these two views is taken. If it is a scheme for an important part of the UK education sector it wll have a very long (or indefinite) time horizon and will best be invested in equities to get the higher return over the long term. But if universities are seen as firms operating in the market place - and could go bust at any moment - then equities are too risky.

It is not clear that USS's investment strategy is wrong.

Dennis Leech

23 Sep 2014 01:53

| ![]() Tags: Eye Pensions; Private Uss;

| Comments (2)

| Report a problem

Tags: Eye Pensions; Private Uss;

| Comments (2)

| Report a problem

September 22, 2014

Letter to THE: Plea for more balanced reporting on USS

I have complained to the Times Higher Education magazine about their reporting about the USS. They tend to present deficit figures as if they are given facts rather than misleadng statistics derived from the misapplicaiton of financial theories. Fair reporting would at least acknowledge that the whole question of the deficit is political and highly controversial.

I would recommend that all should heed the advice of the Cambridge economist Ha-Joon Chang in his latest book "Economics: A Users Guide" and in his recent Guardian article "Economics is too important to leave to the experts" After all we are all participants in the economy and as such users of economics.

Letter to the Times Higher Education to be published on 25 September.

Dear Sir

I wish to complain about your reporting about USS pensions. Your reports tend to imply that statistics show a funding deficit as if the USS's assets and liabilities are objective scientific truths when in fact they are based on theories.

There are two principles on which DB (defined benefit) pension schemes are organised: pay-as-you-go - used throughout the public sector including the teachers' pension scheme - and funding - used for smaller pension schemes offered by private sector employers in the risky market place. How we think about the USS depends on which of these principles we apply. Viewed as a PAYG scheme USS appears to be financially strong with an annual surplus of over a billion pounds a year, a strongly performing investment portfolio and growing membership. The deficit figures you quote come from regarding USS as if it were the other type of scheme, one belonging to a small company that must be prudently managed against the likelihood of the firm failing. But to apply that approach to the whole pre-92 HE sector covered by USS is to misuse a theoretical model by applying it in circumstances it was not designed for and in which it will cease to work. We have heard a lot about economic models failing in the financial crash of 2008; we have the same issue today with pensions.

Can I suggest that you follow the advice of Ha-Joon Chang when he says "Economics is too important to leave to the experts"? Rather than taking on trust the opinion of someone styled as a pensions expert (as you frequently do) you actually get them to justify in detail what assumptions they are making, and recognise that the whole issue of the state of the USS is in fact highly controversial.

Dennis Leech

Professor of Economics

University of Warwick

Coventry CV4 8UW

d.leech@warwick.ac.uk

www2.warwick.ac.uk/fac/soc/economics/staff/faculty/leech

07712353201

Dennis Leech

22 Sep 2014 09:59

| ![]() Tags: Economics Neoliberalism; Pensions; Uss;

| Comments (0)

| Report a problem

Tags: Economics Neoliberalism; Pensions; Uss;

| Comments (0)

| Report a problem

September 17, 2012

Universities' Pensions Deficit is not Believable

Writing about web page http://www.timeshighereducation.co.uk/story.asp?sectioncode=26&storycode=421130&c=1

We have been told that there has been an increase in the deficit in the USS pension scheme in the past year that is so large as to threaten its very survival. (See the Times Higher Education report “Deficit puts pension scheme in jeopardy”, 13th September 2012.)

The funding level has suddenly plummeted from 92 percent to 77 percent between March 2011 and March 2012, but we have been given no explanation as to what is so wrong about it that would cause it to collapse on such a scale, which is far in excess of what would be caused by problems that critics (eg Tom Pike and Jim Naismith) have pointed to.

I think some analysis is needed before we believe some of the alarmist statements being made. There are grounds for believing there is a lot of artificiality in the figures and that they do not reflect fair value accounting.

The deficit is the difference between assets (USS investments) and liabilities (future and present pensions). Assets have INCREASED by 1.5 billion pounds. So the explanation cannot lie in poor investment performance. The problem is with the liabilities that have ballooned by £8.4 billion pounds - IN ONLY ONE YEAR. How is such a change – not only large but astronomical - credible? That is the question we all need to address.

It is all the more astonishing since the rule changes that were introduced last October ought to have reduced the liabilities, not increased them: introduction of the CARE section, increasing normal pension age to 65, flexible retirement, capping inflation adjustment. It cannot be due to increasing longevity since there has not been a major change in predictions of life expectancy.

(Increasing life expectancy is often blamed for deficits but its effect is exaggerated as the last valuation report showed: it increased the deficit between 2008 and 2011 by 0.6 billion pounds - much less than several other items such as the impact of basing inflation indexing on CPI instead of RPI which reduced the deficit by 2.9 billion pounds. The longevity argument is really a con. If members are expected to live one year longer, the liabilities figure increases by 0.6 billion pounds - significant but not an existential threat to the fund.)

WHY, then, has the reported liabilities figure gone up so much in one year? The answer is that the figure is artificial and highly misleading due to the way it is calculated under legislative rules, introduced in the Pensions Act 2004, that now apply to all private sector defined benefit pension schemes (of which USS counts as one). The reasons are technical (but no less controversial for that): it is calculated as a present value capital sum using a discount rate based on gilt rates which are currently very low, hence the large figure.

BUT the ACTUAL liabilities – the monthly payments to USS pensioners and future pensioners - are no different than they were before! So why the change in the liabilities figure? In fact the funding deficit is an artifact, a result of the overcautious regulatory regime brought in by the last government, that was meant to protect private pensions against the insolvency of the corporate sponsor but is having the unintended consequence of forcing perfectly good schemes to close.

It is worth reminding ourselves how a private pension scheme works: a group of employers and workers pay contributions into a collective fund, out of which pensions are paid to retired workers under defined rules, and surplus funds invested to earn dividends and interest for the future. It should be judged simply on whether its income exceeds expenditure on a sustainable basis, taking account of all future foreseeable changes.

From this point of view the USS is not in bad shape. The latest published accounts (2011) show that annual investment returns (including dividends from our investments in highly profitable companies like Shell, HSBC, Vodafone, BP, etc and government bonds) were about £2.4 billion, easily paying the current pensions bill of £1.4 billion per year. On top of that rising contribution income from members and employers brought in another £1.5 billion per year.

This is not the whole story, of course, because the scheme is still growing and it is necessary to make allowance for expected future changes: such as rising life expectancy, expected salary increases, retirement ages, inflation and so on. How this is done is an important issue surrounded by much uncertainty.

But the one thing that is certain is that interest rates on government bonds have nothing to do with it (except to the extent that part of the investment portfolio is in government bonds). What a member receives in pension payments when he or she retires will depend on their years of service, their pensionable salary, inflation and how long they live. The interest rate on gilts does not have any effect on this, so it is really bogus to convert these payments to a liability figure using it.

The same artificial calculation has led to yawning deficits in many company pension schemes. In August the ONS reported the combined UK deficit on this basis was £280 billion which has led to calls for emergency extra funding from employers. The artificiality of all this has led bodies such as the Confederation of British Industry and National Association of Pension Funds to call for government action to change the rules.

The whole emerging fiasco in funded pension schemes like USS is the result of the overeager application of neo-liberal economic thinking during the boom years. What is happening to USS, and the other final salary pension schemes in the private sector, is the logical culmination of a process based on the philosophy that “there is no such thing as society, only individuals and their families”.

What is needed is not to close down the scheme, but to defend it for the success it is, and for the government to look again at the distortionary regulatory rules that have been introduced without sufficient thought.

Dennis Leech

17 Sep 2012 01:20

| ![]() Tags: Neoliberal Economics; Pensions Uss;

| Comments (0)

| Report a problem

Tags: Neoliberal Economics; Pensions Uss;

| Comments (0)

| Report a problem

Loading…

Loading…

{kind=link}